Advertisement

Risks To Shareholder Returns Are Elevated At These Prices For Beijing Gehua Catv Network Co.,Ltd. (SHSE:600037)

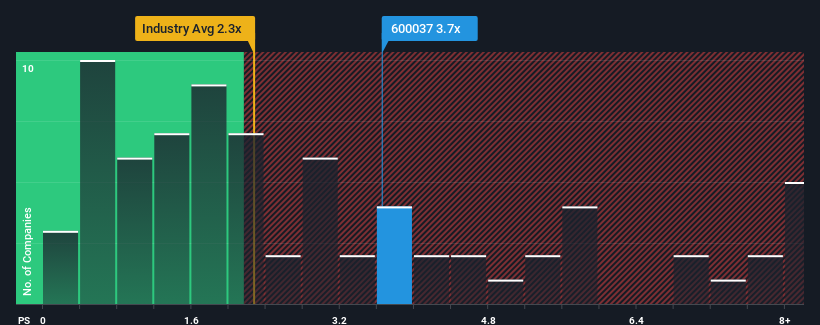

Beijing Gehua Catv Network Co.,Ltd.'s (SHSE:600037) price-to-sales (or "P/S") ratio of 3.7x may not look like an appealing investment opportunity when you consider close to half the companies in the Media industry in China have P/S ratios below 2.3x. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Beijing Gehua Catv NetworkLtd

How Beijing Gehua Catv NetworkLtd Has Been Performing

Beijing Gehua Catv NetworkLtd hasn't been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. One possibility is that the P/S ratio is high because investors think this poor revenue performance will turn the corner. However, if this isn't the case, investors might get caught out paying too much for the stock.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Beijing Gehua Catv NetworkLtd.Is There Enough Revenue Growth Forecasted For Beijing Gehua Catv NetworkLtd?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Beijing Gehua Catv NetworkLtd's to be considered reasonable.

Retrospectively, the last year delivered virtually the same number to the company's top line as the year before. This isn't what shareholders were looking for as it means they've been left with a 7.2% decline in revenue over the last three years in total. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Turning to the outlook, the next year should generate growth of 5.3% as estimated by the sole analyst watching the company. With the industry predicted to deliver 12% growth, the company is positioned for a weaker revenue result.

In light of this, it's alarming that Beijing Gehua Catv NetworkLtd's P/S sits above the majority of other companies. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of revenue growth is likely to weigh heavily on the share price eventually.

What We Can Learn From Beijing Gehua Catv NetworkLtd's P/S?

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've concluded that Beijing Gehua Catv NetworkLtd currently trades on a much higher than expected P/S since its forecast growth is lower than the wider industry. When we see a weak revenue outlook, we suspect the share price faces a much greater risk of declining, bringing back down the P/S figures. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

Many other vital risk factors can be found on the company's balance sheet. Our free balance sheet analysis for Beijing Gehua Catv NetworkLtd with six simple checks will allow you to discover any risks that could be an issue.

If these risks are making you reconsider your opinion on Beijing Gehua Catv NetworkLtd, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Beijing Gehua Catv NetworkLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600037

Beijing Gehua Catv NetworkLtd

Engages in the construction, management, operation, and maintenance of cable radio and television networks in China.

Flawless balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.6% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.6% undervalued

GM

Community Contributor