Advertisement

Hubei Feilihua Quartz Glass Co., Ltd. (SZSE:300395) Stocks Shoot Up 36% But Its P/E Still Looks Reasonable

Hubei Feilihua Quartz Glass Co., Ltd. (SZSE:300395) shareholders have had their patience rewarded with a 36% share price jump in the last month. The bad news is that even after the stocks recovery in the last 30 days, shareholders are still underwater by about 5.1% over the last year.

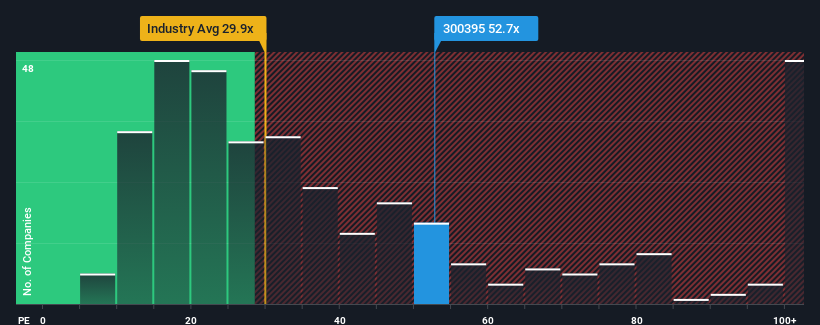

Since its price has surged higher, Hubei Feilihua Quartz Glass may be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 52.7x, since almost half of all companies in China have P/E ratios under 29x and even P/E's lower than 18x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

With earnings that are retreating more than the market's of late, Hubei Feilihua Quartz Glass has been very sluggish. One possibility is that the P/E is high because investors think the company will turn things around completely and accelerate past most others in the market. If not, then existing shareholders may be very nervous about the viability of the share price.

Check out our latest analysis for Hubei Feilihua Quartz Glass

How Is Hubei Feilihua Quartz Glass' Growth Trending?

The only time you'd be truly comfortable seeing a P/E as steep as Hubei Feilihua Quartz Glass' is when the company's growth is on track to outshine the market decidedly.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 20%. That put a dampener on the good run it was having over the longer-term as its three-year EPS growth is still a noteworthy 23% in total. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been mostly respectable for the company.

Looking ahead now, EPS is anticipated to climb by 27% each year during the coming three years according to the five analysts following the company. With the market only predicted to deliver 19% per year, the company is positioned for a stronger earnings result.

In light of this, it's understandable that Hubei Feilihua Quartz Glass' P/E sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Final Word

The strong share price surge has got Hubei Feilihua Quartz Glass' P/E rushing to great heights as well. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Hubei Feilihua Quartz Glass' analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

Before you take the next step, you should know about the 2 warning signs for Hubei Feilihua Quartz Glass (1 is concerning!) that we have uncovered.

You might be able to find a better investment than Hubei Feilihua Quartz Glass. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Hubei Feilihua Quartz Glass might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300395

Hubei Feilihua Quartz Glass

Manufactures and sells quartz material and quartz fiber products worldwide.

High growth potential with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.5% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.1% undervalued

TO

Community Contributor