Earnings Not Telling The Story For Hubei Feilihua Quartz Glass Co., Ltd. (SZSE:300395) After Shares Rise 28%

Hubei Feilihua Quartz Glass Co., Ltd. (SZSE:300395) shares have had a really impressive month, gaining 28% after a shaky period beforehand. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 23% in the last twelve months.

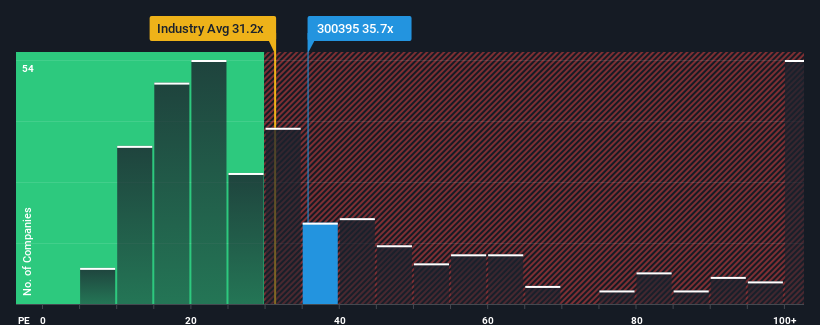

Since its price has surged higher, given around half the companies in China have price-to-earnings ratios (or "P/E's") below 30x, you may consider Hubei Feilihua Quartz Glass as a stock to potentially avoid with its 35.7x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

Hubei Feilihua Quartz Glass hasn't been tracking well recently as its declining earnings compare poorly to other companies, which have seen some growth on average. It might be that many expect the dour earnings performance to recover substantially, which has kept the P/E from collapsing. If not, then existing shareholders may be extremely nervous about the viability of the share price.

View our latest analysis for Hubei Feilihua Quartz Glass

Does Growth Match The High P/E?

In order to justify its P/E ratio, Hubei Feilihua Quartz Glass would need to produce impressive growth in excess of the market.

Retrospectively, the last year delivered a frustrating 2.3% decrease to the company's bottom line. However, a few very strong years before that means that it was still able to grow EPS by an impressive 65% in total over the last three years. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

Shifting to the future, estimates from the six analysts covering the company suggest earnings should grow by 23% per annum over the next three years. Meanwhile, the rest of the market is forecast to expand by 25% each year, which is not materially different.

In light of this, it's curious that Hubei Feilihua Quartz Glass' P/E sits above the majority of other companies. Apparently many investors in the company are more bullish than analysts indicate and aren't willing to let go of their stock right now. Although, additional gains will be difficult to achieve as this level of earnings growth is likely to weigh down the share price eventually.

What We Can Learn From Hubei Feilihua Quartz Glass' P/E?

Hubei Feilihua Quartz Glass shares have received a push in the right direction, but its P/E is elevated too. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

Our examination of Hubei Feilihua Quartz Glass' analyst forecasts revealed that its market-matching earnings outlook isn't impacting its high P/E as much as we would have predicted. When we see an average earnings outlook with market-like growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless these conditions improve, it's challenging to accept these prices as being reasonable.

Plus, you should also learn about this 1 warning sign we've spotted with Hubei Feilihua Quartz Glass.

If you're unsure about the strength of Hubei Feilihua Quartz Glass' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

If you're looking to trade Hubei Feilihua Quartz Glass, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Hubei Feilihua Quartz Glass might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300395

Hubei Feilihua Quartz Glass

Manufactures and sells quartz material and quartz fiber products worldwide.

High growth potential with excellent balance sheet.

Market Insights

Community Narratives