Advertisement

February 2025's Stocks Trading Below Estimated Intrinsic Value

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a landscape marked by fluctuating corporate earnings and geopolitical tensions, investors are keenly observing the Federal Reserve's steady interest rate policy amid persistent inflationary pressures. In this context, identifying stocks trading below their estimated intrinsic value can present opportunities for those looking to potentially capitalize on market inefficiencies. Understanding what makes a stock undervalued often involves assessing its fundamentals against current market conditions, such as competitive pressures in sectors like technology or shifts in monetary policies worldwide.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Shihlin Electric & Engineering (TWSE:1503) | NT$176.00 | NT$352.00 | 50% |

| Brookline Bancorp (NasdaqGS:BRKL) | US$12.06 | US$24.01 | 49.8% |

| Nordic Waterproofing Holding (OM:NWG) | SEK170.60 | SEK340.70 | 49.9% |

| World Fitness Services (TWSE:2762) | NT$90.00 | NT$179.64 | 49.9% |

| All Ring Tech (TPEX:6187) | NT$375.50 | NT$748.61 | 49.8% |

| Atea (OB:ATEA) | NOK141.80 | NOK281.59 | 49.6% |

| Elekta (OM:EKTA B) | SEK64.60 | SEK128.36 | 49.7% |

| Kinaxis (TSX:KXS) | CA$171.05 | CA$340.41 | 49.8% |

| QuinStreet (NasdaqGS:QNST) | US$23.71 | US$47.35 | 49.9% |

| Equifax (NYSE:EFX) | US$267.52 | US$531.27 | 49.6% |

Here we highlight a subset of our preferred stocks from the screener.

Shenzhen Breo Technology (SHSE:688793)

Overview: Shenzhen Breo Technology Co., Ltd. specializes in the research and development of portable massage products for relieving headache swelling, eye fatigue, and shoulder and neck pain, with a market cap of CN¥2.18 billion.

Operations: Revenue Segments (in millions of CN¥):

Estimated Discount To Fair Value: 49%

Shenzhen Breo Technology is trading at CN¥26.15, significantly below its estimated fair value of CN¥51.29, reflecting a potential undervaluation based on discounted cash flow analysis. The stock is valued well compared to peers and the industry, with earnings projected to grow 69.7% annually and revenue expected to outpace the Chinese market at 19.9% per year. Additionally, profitability is anticipated within three years with a strong return on equity forecasted at 21.6%.

- The analysis detailed in our Shenzhen Breo Technology growth report hints at robust future financial performance.

- Dive into the specifics of Shenzhen Breo Technology here with our thorough financial health report.

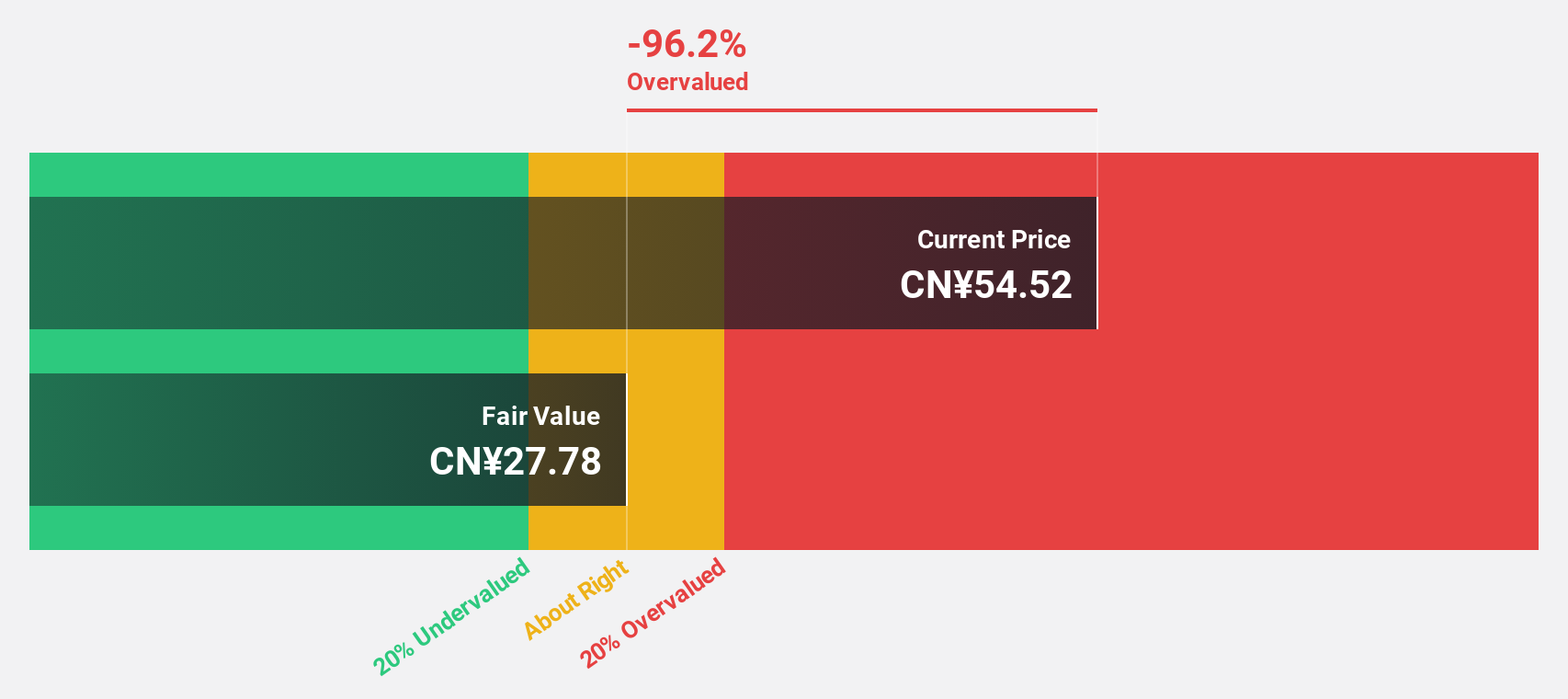

Kehua Data (SZSE:002335)

Overview: Kehua Data Co., Ltd. offers integrated solutions for power protection and energy conservation globally, with a market cap of CN¥13.22 billion.

Operations: Kehua Data's revenue segments include power protection solutions and energy conservation services, contributing to its global operations.

Estimated Discount To Fair Value: 37.9%

Kehua Data is trading at CN¥28.65, significantly below its estimated fair value of CN¥46.15, highlighting substantial undervaluation based on discounted cash flow analysis. Despite recent volatility and a decline in profit margins from 5.4% to 3.7%, the company's earnings are projected to grow considerably at 42% annually, outpacing the broader Chinese market's growth rate of 25.1%. Revenue is also expected to grow faster than the market average at 18.7% per year.

- Insights from our recent growth report point to a promising forecast for Kehua Data's business outlook.

- Get an in-depth perspective on Kehua Data's balance sheet by reading our health report here.

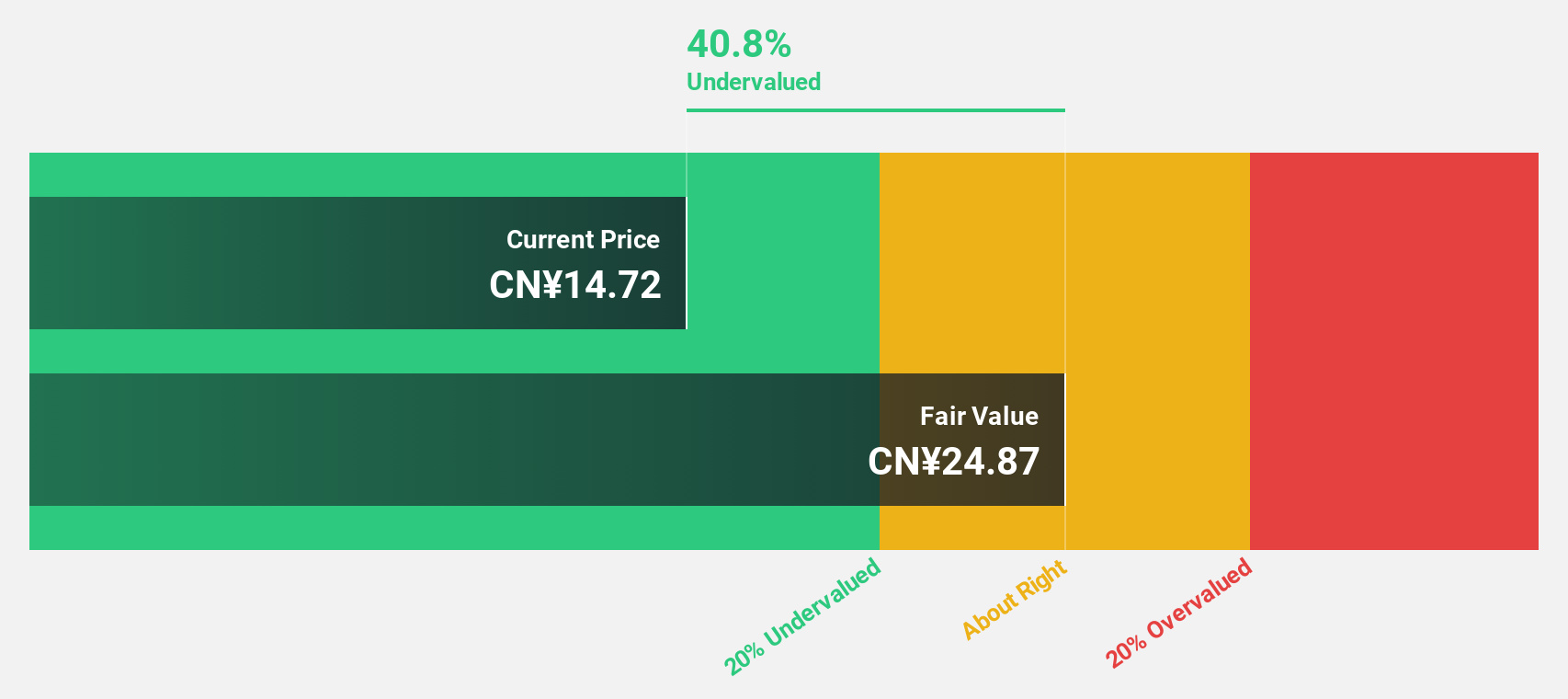

Shenzhen King Explorer Science and Technology (SZSE:002917)

Overview: Shenzhen King Explorer Science and Technology Corporation focuses on researching, designing, developing, manufacturing, and selling intelligent equipment systems for civil explosive production and blasting service companies in China and internationally, with a market cap of CN¥5.67 billion.

Operations: Shenzhen King Explorer Science and Technology Corporation generates revenue by providing intelligent equipment systems to companies involved in civil explosive production and blasting services both domestically and internationally.

Estimated Discount To Fair Value: 15.8%

Shenzhen King Explorer Science and Technology is trading at CN¥16.56, slightly below its estimated fair value of CN¥19.66, suggesting moderate undervaluation based on discounted cash flow analysis. The company's earnings are projected to grow significantly at 38.6% annually, surpassing the Chinese market's growth rate of 25.1%. Revenue growth is also expected to exceed market averages at 25.1% per year, although the share price has been highly volatile recently and dividend stability remains uncertain.

- In light of our recent growth report, it seems possible that Shenzhen King Explorer Science and Technology's financial performance will exceed current levels.

- Click here and access our complete balance sheet health report to understand the dynamics of Shenzhen King Explorer Science and Technology.

Seize The Opportunity

- Click here to access our complete index of 906 Undervalued Stocks Based On Cash Flows.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002917

Shenzhen King Explorer Science and Technology

Researches, designs, develops, manufactures, and sells intelligent equipment systems to civil explosive production and blasting service companies in China and internationally.

Undervalued with high growth potential.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor