Advertisement

With A 29% Price Drop For Zhejiang Zhongxin Fluoride Materials Co.,Ltd (SZSE:002915) You'll Still Get What You Pay For

The Zhejiang Zhongxin Fluoride Materials Co.,Ltd (SZSE:002915) share price has fared very poorly over the last month, falling by a substantial 29%. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 48% in that time.

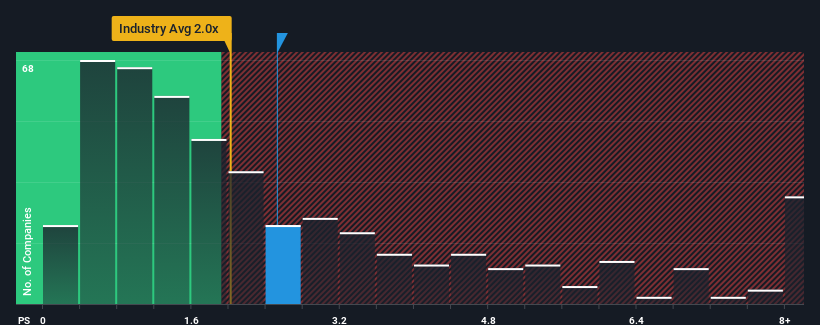

In spite of the heavy fall in price, given close to half the companies operating in China's Chemicals industry have price-to-sales ratios (or "P/S") below 2x, you may still consider Zhejiang Zhongxin Fluoride MaterialsLtd as a stock to potentially avoid with its 2.5x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

Check out our latest analysis for Zhejiang Zhongxin Fluoride MaterialsLtd

How Has Zhejiang Zhongxin Fluoride MaterialsLtd Performed Recently?

Zhejiang Zhongxin Fluoride MaterialsLtd hasn't been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. One possibility is that the P/S ratio is high because investors think this poor revenue performance will turn the corner. However, if this isn't the case, investors might get caught out paying too much for the stock.

Keen to find out how analysts think Zhejiang Zhongxin Fluoride MaterialsLtd's future stacks up against the industry? In that case, our free report is a great place to start.How Is Zhejiang Zhongxin Fluoride MaterialsLtd's Revenue Growth Trending?

Zhejiang Zhongxin Fluoride MaterialsLtd's P/S ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 16%. That put a dampener on the good run it was having over the longer-term as its three-year revenue growth is still a noteworthy 30% in total. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of revenue growth.

Shifting to the future, estimates from the dual analysts covering the company suggest revenue should grow by 93% over the next year. Meanwhile, the rest of the industry is forecast to only expand by 20%, which is noticeably less attractive.

In light of this, it's understandable that Zhejiang Zhongxin Fluoride MaterialsLtd's P/S sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Final Word

There's still some elevation in Zhejiang Zhongxin Fluoride MaterialsLtd's P/S, even if the same can't be said for its share price recently. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Zhejiang Zhongxin Fluoride MaterialsLtd maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Chemicals industry, as expected. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

You should always think about risks. Case in point, we've spotted 2 warning signs for Zhejiang Zhongxin Fluoride MaterialsLtd you should be aware of.

If these risks are making you reconsider your opinion on Zhejiang Zhongxin Fluoride MaterialsLtd, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Zhongxin Fluoride MaterialsLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002915

Zhejiang Zhongxin Fluoride MaterialsLtd

Engages in the research and development, production, and sale of fluorine-based fine chemicals in China.

Reasonable growth potential with very low risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor