Advertisement

It's A Story Of Risk Vs Reward With Qingdao Gon Technology Co., Ltd. (SZSE:002768)

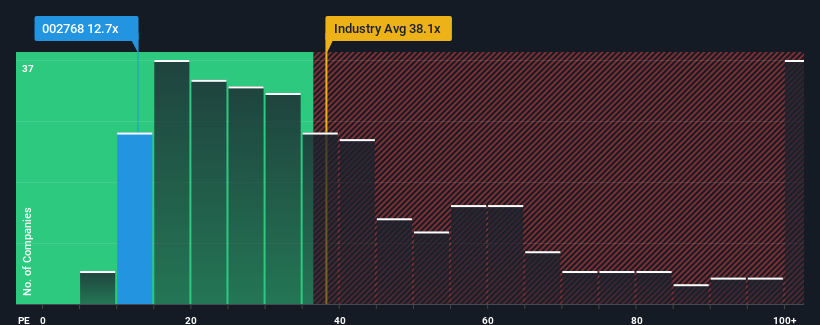

With a price-to-earnings (or "P/E") ratio of 12.7x Qingdao Gon Technology Co., Ltd. (SZSE:002768) may be sending very bullish signals at the moment, given that almost half of all companies in China have P/E ratios greater than 40x and even P/E's higher than 78x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

Qingdao Gon Technology certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. One possibility is that the P/E is low because investors think the company's earnings are going to fall away like everyone else's soon. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

See our latest analysis for Qingdao Gon Technology

How Is Qingdao Gon Technology's Growth Trending?

In order to justify its P/E ratio, Qingdao Gon Technology would need to produce anemic growth that's substantially trailing the market.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 8.1% last year. Still, EPS has barely risen at all in aggregate from three years ago, which is not ideal. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Looking ahead now, EPS is anticipated to climb by 40% during the coming year according to the sole analyst following the company. That's shaping up to be similar to the 37% growth forecast for the broader market.

With this information, we find it odd that Qingdao Gon Technology is trading at a P/E lower than the market. Apparently some shareholders are doubtful of the forecasts and have been accepting lower selling prices.

The Bottom Line On Qingdao Gon Technology's P/E

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Qingdao Gon Technology's analyst forecasts revealed that its market-matching earnings outlook isn't contributing to its P/E as much as we would have predicted. There could be some unobserved threats to earnings preventing the P/E ratio from matching the outlook. At least the risk of a price drop looks to be subdued, but investors seem to think future earnings could see some volatility.

There are also other vital risk factors to consider before investing and we've discovered 1 warning sign for Qingdao Gon Technology that you should be aware of.

If these risks are making you reconsider your opinion on Qingdao Gon Technology, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Qingdao Gon Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002768

Qingdao Gon Technology

Engages in the research and development, production, and sale of modified plastic particles and products, and functional plastic plates in China and internationally.

Proven track record with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor