Advertisement

- China

- /

- Semiconductors

- /

- SHSE:603806

3 Global Growth Companies With High Insider Ownership Growing Revenues At 20%

Simply Wall St

Reviewed by Simply Wall St

In the current global market landscape, growth stocks have been outperforming value stocks, with indices like the Nasdaq Composite and Russell 2000 showing strong gains despite economic uncertainties such as the U.S. government shutdown and fluctuating commodity prices. In this environment, companies that not only exhibit robust revenue growth but also have high insider ownership can be particularly appealing to investors seeking alignment of interests between management and shareholders.

Top 10 Growth Companies With High Insider Ownership Globally

| Name | Insider Ownership | Earnings Growth |

| Seers Technology (KOSDAQ:A458870) | 33.9% | 84.6% |

| Pharma Mar (BME:PHM) | 11.9% | 44.2% |

| Laopu Gold (SEHK:6181) | 35.5% | 34% |

| KebNi (OM:KEBNI B) | 36.3% | 63.7% |

| J&V Energy Technology (TWSE:6869) | 17.5% | 24.9% |

| Gold Circuit Electronics (TWSE:2368) | 31.4% | 35.2% |

| Fulin Precision (SZSE:300432) | 11.7% | 50.7% |

| Elliptic Laboratories (OB:ELABS) | 24.4% | 97.5% |

| CD Projekt (WSE:CDR) | 29.7% | 43.1% |

| Ascentage Pharma Group International (SEHK:6855) | 12.8% | 91.9% |

We're going to check out a few of the best picks from our screener tool.

Hoshine Silicon Industry (SHSE:603260)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Hoshine Silicon Industry Co., Ltd. is involved in the production and sale of silicon-based materials both in China and internationally, with a market cap of CN¥57.98 billion.

Operations: Hoshine Silicon Industry Co., Ltd. generates revenue through the production and sale of silicon-based materials both domestically and internationally.

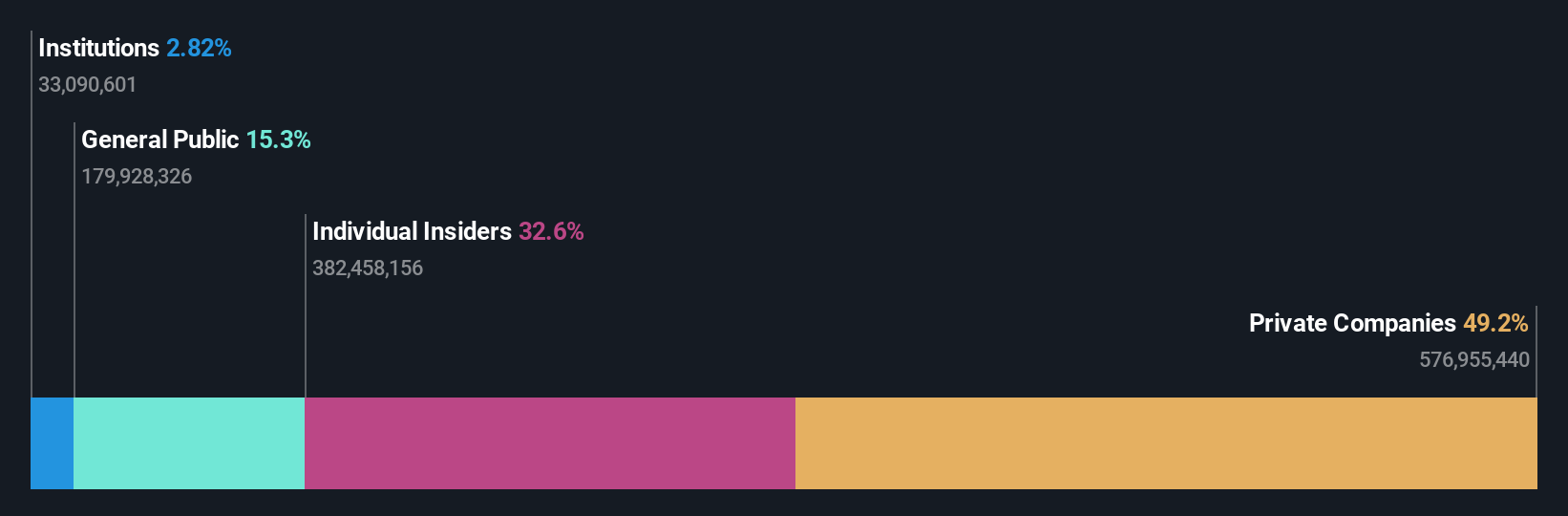

Insider Ownership: 32.6%

Revenue Growth Forecast: 15.4% p.a.

Hoshine Silicon Industry faces challenges with declining revenue and a net loss for the first half of 2025, contrasting its strong forecasted earnings growth of over 65% annually. Despite lower profit margins, its revenue growth outpaces the Chinese market average. A recent transaction saw Xiao Xiugen acquire a significant stake for CNY 2.63 billion, highlighting substantial insider ownership interest. However, financial stability concerns persist due to inadequate interest coverage and unsustainable dividends.

- Get an in-depth perspective on Hoshine Silicon Industry's performance by reading our analyst estimates report here.

- Our expertly prepared valuation report Hoshine Silicon Industry implies its share price may be too high.

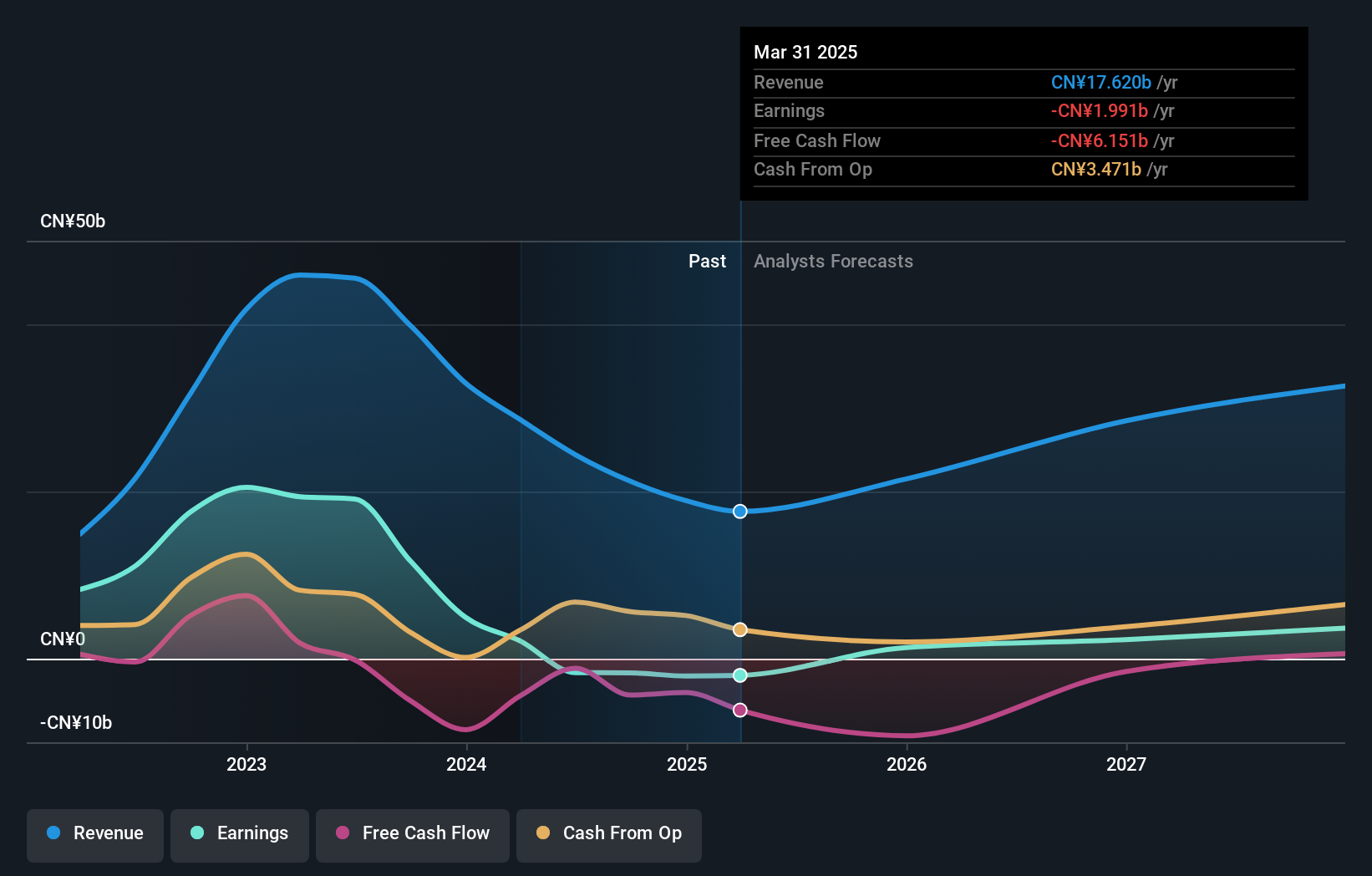

Hangzhou First Applied Material (SHSE:603806)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Hangzhou First Applied Material Co., Ltd. and its subsidiaries specialize in the design, development, manufacture, and sale of solar battery encapsulation materials both in China and internationally, with a market cap of CN¥40.91 billion.

Operations: Hangzhou First Applied Material Co., Ltd. generates revenue primarily through the design, development, manufacturing, and sales of solar battery encapsulation materials in both domestic and international markets.

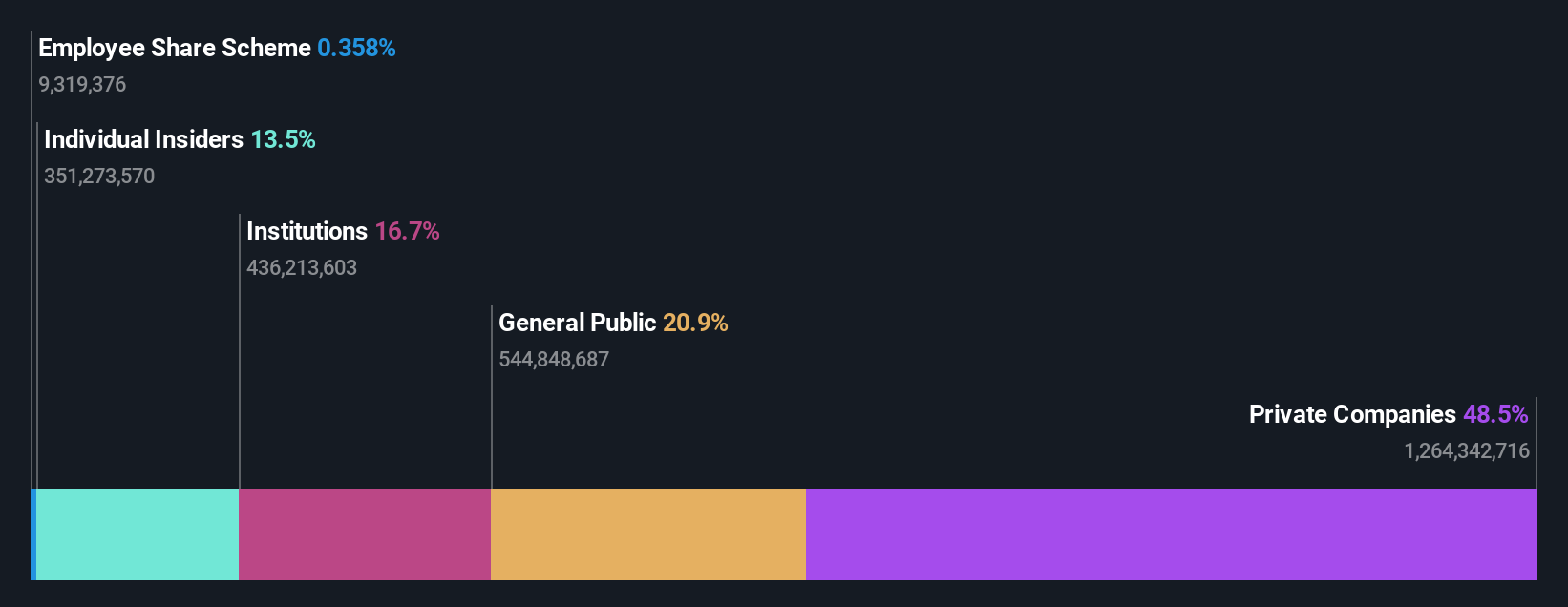

Insider Ownership: 13.5%

Revenue Growth Forecast: 16.7% p.a.

Hangzhou First Applied Material is poised for significant earnings growth of 35.85% annually, surpassing the Chinese market average, despite a decline in revenue and net income for H1 2025. The company's price-to-earnings ratio of 48.5x suggests good value relative to industry peers. However, its profit margins have decreased from last year, and its return on equity is forecasted to remain low at 10.5%. Recent financial results indicate challenges but highlight potential growth opportunities.

- Click here and access our complete growth analysis report to understand the dynamics of Hangzhou First Applied Material.

- Insights from our recent valuation report point to the potential undervaluation of Hangzhou First Applied Material shares in the market.

Ganfeng Lithium Group (SZSE:002460)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Ganfeng Lithium Group Co., Ltd. is involved in the manufacturing and sale of lithium products, with a market capitalization of approximately CN¥117.44 billion.

Operations: Ganfeng Lithium Group Co., Ltd. generates revenue primarily through the production and sale of lithium products.

Insider Ownership: 27.3%

Revenue Growth Forecast: 20.1% p.a.

Ganfeng Lithium Group is navigating a challenging landscape with recent amendments to its Articles of Association and a HK$1.17 billion follow-on equity offering. Despite reporting a net loss of CNY 531.24 million for H1 2025, the company shows potential with forecasted revenue growth exceeding the market average at 20.1% annually and expected profitability within three years. The strategic joint venture with Lithium Argentina AG underscores its commitment to expanding lithium projects, although financial stability remains an area of concern due to high debt levels.

- Take a closer look at Ganfeng Lithium Group's potential here in our earnings growth report.

- Our valuation report here indicates Ganfeng Lithium Group may be overvalued.

Make It Happen

- Dive into all 810 of the Fast Growing Global Companies With High Insider Ownership we have identified here.

- Seeking Other Investments? Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Hangzhou First Applied Material might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:603806

Hangzhou First Applied Material

Designs, develops, manufactures, and sells solar battery encapsulation materials in China and internationally.

Excellent balance sheet with reasonable growth potential and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|41.9% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|14.1% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$613.59|1.3% undervalued

AN

Based on Analyst Price Targets