Market Still Lacking Some Conviction On Jiangsu Changqing Agrochemical Co., Ltd. (SZSE:002391)

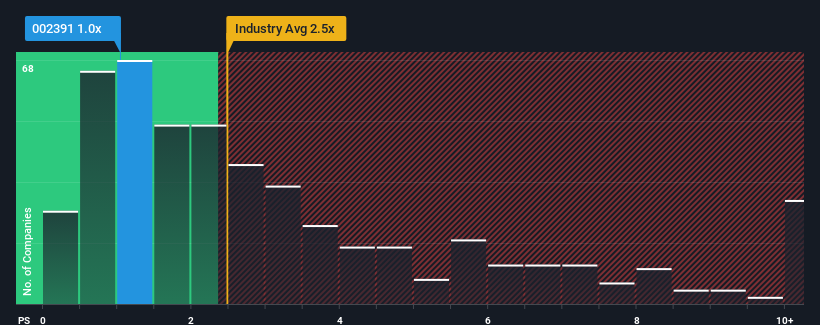

You may think that with a price-to-sales (or "P/S") ratio of 1x Jiangsu Changqing Agrochemical Co., Ltd. (SZSE:002391) is a stock worth checking out, seeing as almost half of all the Chemicals companies in China have P/S ratios greater than 2.5x and even P/S higher than 5x aren't out of the ordinary. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for Jiangsu Changqing Agrochemical

What Does Jiangsu Changqing Agrochemical's P/S Mean For Shareholders?

Jiangsu Changqing Agrochemical hasn't been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. The P/S ratio is probably low because investors think this poor revenue performance isn't going to get any better. So while you could say the stock is cheap, investors will be looking for improvement before they see it as good value.

Want the full picture on analyst estimates for the company? Then our free report on Jiangsu Changqing Agrochemical will help you uncover what's on the horizon.How Is Jiangsu Changqing Agrochemical's Revenue Growth Trending?

Jiangsu Changqing Agrochemical's P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

Retrospectively, the last year delivered a frustrating 6.7% decrease to the company's top line. This has soured the latest three-year period, which nevertheless managed to deliver a decent 5.7% overall rise in revenue. So we can start by confirming that the company has generally done a good job of growing revenue over that time, even though it had some hiccups along the way.

Shifting to the future, estimates from the dual analysts covering the company suggest revenue should grow by 27% over the next year. That's shaping up to be materially higher than the 25% growth forecast for the broader industry.

In light of this, it's peculiar that Jiangsu Changqing Agrochemical's P/S sits below the majority of other companies. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

The Bottom Line On Jiangsu Changqing Agrochemical's P/S

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

To us, it seems Jiangsu Changqing Agrochemical currently trades on a significantly depressed P/S given its forecasted revenue growth is higher than the rest of its industry. The reason for this depressed P/S could potentially be found in the risks the market is pricing in. It appears the market could be anticipating revenue instability, because these conditions should normally provide a boost to the share price.

It is also worth noting that we have found 2 warning signs for Jiangsu Changqing Agrochemical that you need to take into consideration.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002391

Jiangsu Changqing Agrochemical

Manufactures and sells pesticides in China, Europe, the United States, and Southeast Asia.

Reasonable growth potential and slightly overvalued.

Market Insights

Community Narratives