Advertisement

- India

- /

- Specialty Stores

- /

- NSEI:V2RETAIL

Discovering November 2024's Undiscovered Gems on None

Simply Wall St

Reviewed by Simply Wall St

In a week marked by volatility, global markets saw major indices like the Nasdaq Composite and S&P MidCap 400 reach record highs only to retreat sharply, while small-cap stocks demonstrated resilience amid cautious earnings reports and mixed economic signals. As investors navigate these turbulent waters, identifying potential "undiscovered gems" requires a keen eye for companies that can withstand macroeconomic pressures and deliver sustainable growth in challenging environments.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Ruentex Interior Design | NA | 44.92% | 51.98% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Steamships Trading | 33.60% | 4.17% | 3.90% | ★★★★★☆ |

| Procimmo Group | 157.49% | 0.65% | 4.94% | ★★★★☆☆ |

| Arab Banking Corporation (B.S.C.) | 190.18% | 16.52% | 21.58% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Practic | NA | 3.63% | 6.85% | ★★★★☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

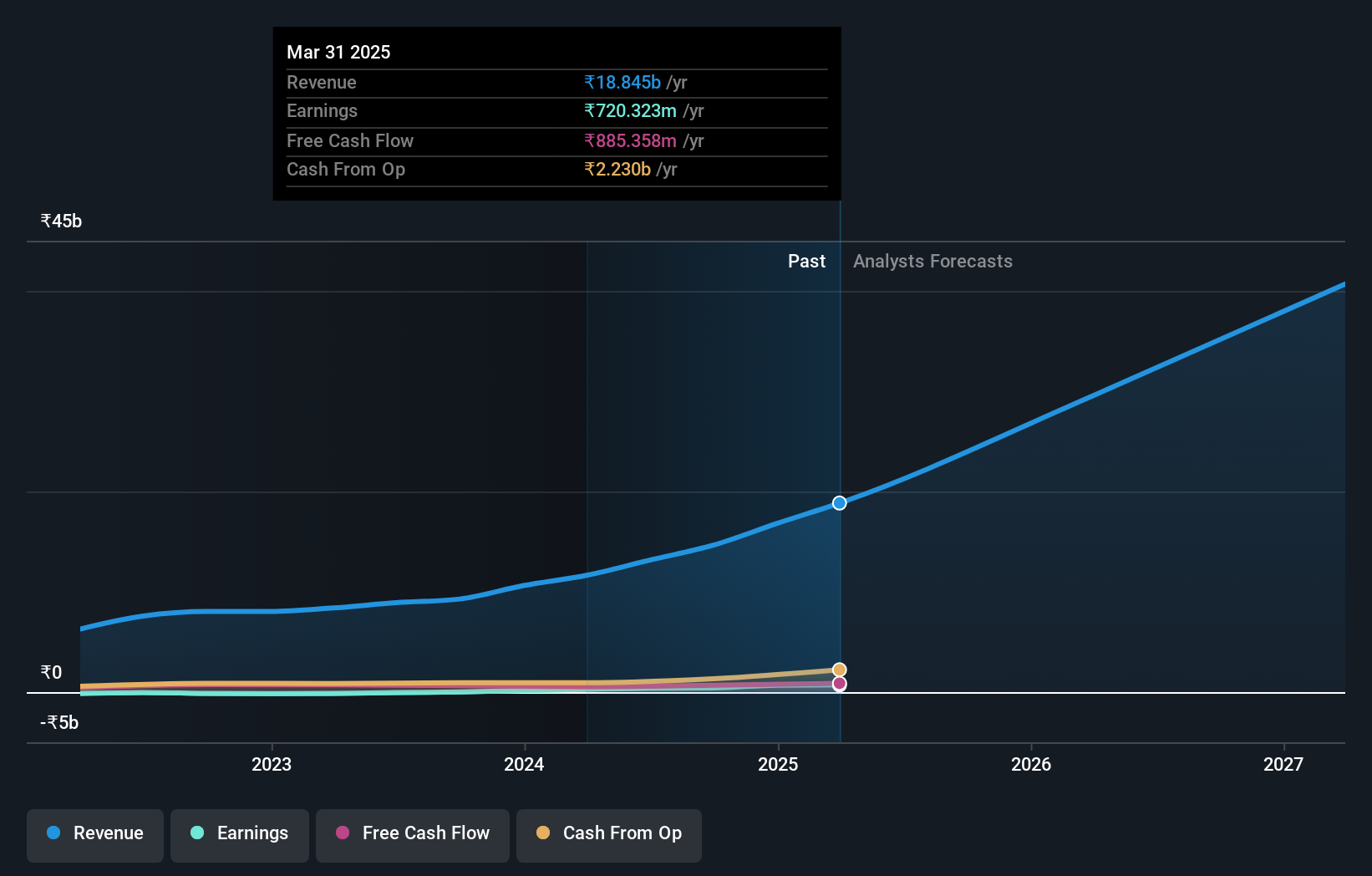

V2 Retail (NSEI:V2RETAIL)

Simply Wall St Value Rating: ★★★★☆☆

Overview: V2 Retail Limited, along with its subsidiary V2 Smart Manufacturing Private Limited, operates in the retail trade sector focusing on apparel, garments, textiles, and accessories across India with a market capitalization of ₹41.87 billion.

Operations: The company generates revenue primarily from the retail trade of garments, textiles, and accessories, amounting to ₹14.65 billion. The net profit margin shows a specific trend that may be of interest to investors analyzing financial performance.

V2 Retail, a notable player in the specialty retail sector, has demonstrated impressive earnings growth of 1834.8% over the past year, significantly outpacing the industry average of 32.8%. The company's net debt to equity ratio stands at 30.3%, which is considered satisfactory, though interest payments are not well covered by EBIT with a coverage of only 1.9x. Recent financial performance highlights include a standalone revenue increase of 64% YoY for Q2 FY25 to INR 3,799.9 million and Same Store Sales Growth (SSG) of approximately 34%, suggesting strong consumer demand and operational efficiency in this market segment.

- Unlock comprehensive insights into our analysis of V2 Retail stock in this health report.

Review our historical performance report to gain insights into V2 Retail's's past performance.

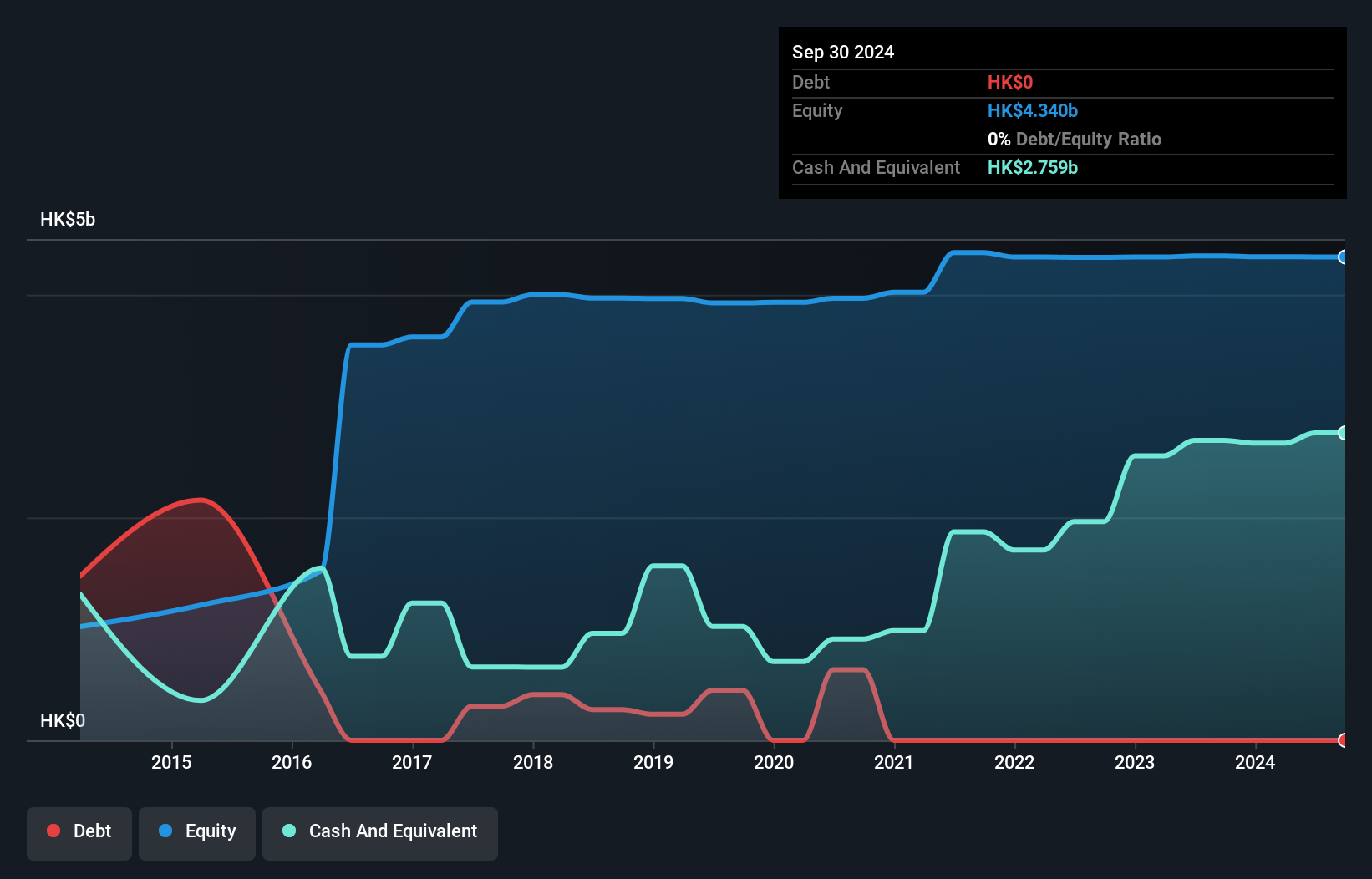

Get Nice Financial Group (SEHK:1469)

Simply Wall St Value Rating: ★★★★★★

Overview: Get Nice Financial Group Limited is an investment holding company offering financial services in Hong Kong, with a market capitalization of HK$2.33 billion.

Operations: The primary revenue streams for Get Nice Financial Group are securities margin financing and broking, generating HK$204.97 million and HK$127.13 million, respectively. The company also earns from corporate finance and asset management, though these contribute significantly less to the overall revenue. Notably, financial instruments investments resulted in a negative impact on revenue with a loss of HK$0.56 million.

Get Nice Financial Group, a smaller player in the financial sector, offers some intriguing aspects for investors. The company is debt-free, which contrasts with its previous debt to equity ratio of 5.9% five years ago. This clean slate likely contributes to its high-quality earnings and has allowed it to grow earnings by 1.9% over the past year, outpacing the capital markets industry average of -50%. Its Price-To-Earnings ratio stands at 15.2x, below the industry average of 19.4x, suggesting potential value for investors seeking underappreciated opportunities in this space.

- Get an in-depth perspective on Get Nice Financial Group's performance by reading our health report here.

Assess Get Nice Financial Group's past performance with our detailed historical performance reports.

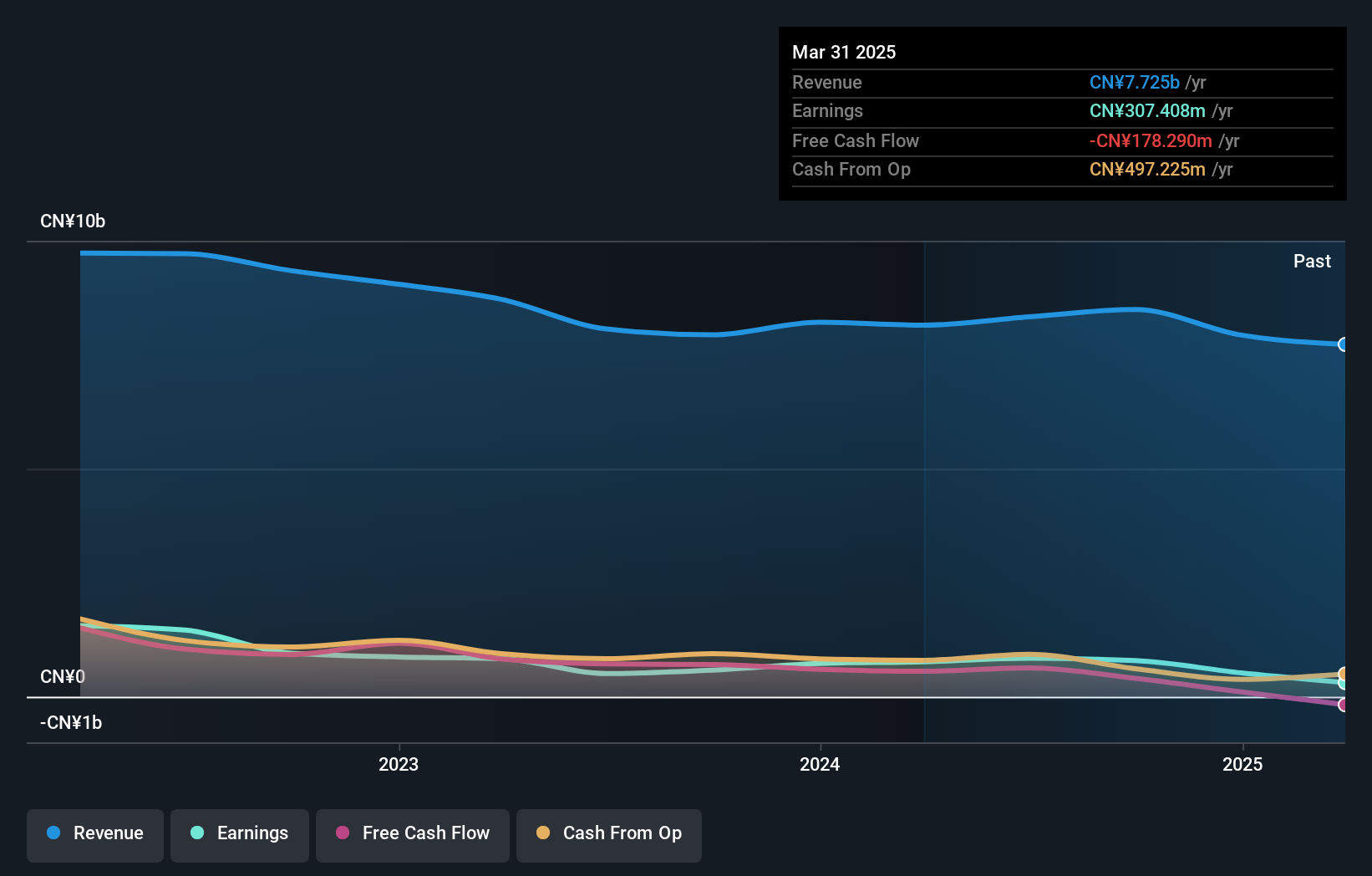

Jiangsu Huachang Chemical (SZSE:002274)

Simply Wall St Value Rating: ★★★★★★

Overview: Jiangsu Huachang Chemical Co., Ltd is a Chinese company that manufactures and sells agrochemicals, basic chemicals, fine chemicals, and biochemical products with a market capitalization of CN¥7.59 billion.

Operations: Jiangsu Huachang Chemical generates revenue through the sale of agrochemicals, basic chemicals, fine chemicals, and biochemical products. The company's financial performance is influenced by its ability to manage production costs and market demand for its diverse chemical offerings.

Jiangsu Huachang Chemical, a nimble player in the chemical sector, has shown robust financial health with a significant reduction in its debt to equity ratio from 87% to 1.7% over five years. The company boasts earnings growth of 35.6%, outpacing the industry average of -4.1%. Its price-to-earnings ratio stands at an attractive 9.6x compared to the broader Chinese market's 35.4x, suggesting potential undervaluation. Recent performance highlights include net income rising to CNY 529.99 million from CNY 469.43 million year-over-year for nine months ending September, reflecting solid operational execution and strategic positioning within its industry niche.

Where To Now?

- Discover the full array of 4705 Undiscovered Gems With Strong Fundamentals right here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:V2RETAIL

V2 Retail

Together with its subsidiary, V2 Smart Manufacturing Private Limited, engages in the retail trade of apparel and garments, textiles, and accessories in India.

Outstanding track record with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|38.6% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|8.8% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.0% undervalued

BL

Community Contributor