Advertisement

- France

- /

- Oil and Gas

- /

- ENXTPA:ES

Undiscovered Gems To Explore On None In November 2024

Simply Wall St

Reviewed by Simply Wall St

As global markets react to the recent U.S. election results, small-cap stocks are gaining attention, with the Russell 2000 Index leading the charge despite not yet reaching record highs. This environment of anticipated economic growth and regulatory changes presents an opportune moment for investors to explore lesser-known stocks that could benefit from these shifts. In this context, identifying promising companies often involves looking for solid fundamentals and potential for growth amidst evolving market conditions.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Eagle Financial Services | 169.49% | 12.30% | 1.92% | ★★★★★★ |

| Parker Drilling | 46.25% | -0.33% | 53.04% | ★★★★★★ |

| Morris State Bancshares | 17.84% | 4.83% | 6.58% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Bakrie & Brothers | 22.66% | 7.78% | 13.50% | ★★★★★☆ |

| Compañía Electro Metalúrgica | 71.27% | 12.50% | 19.90% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

Here's a peek at a few of the choices from the screener.

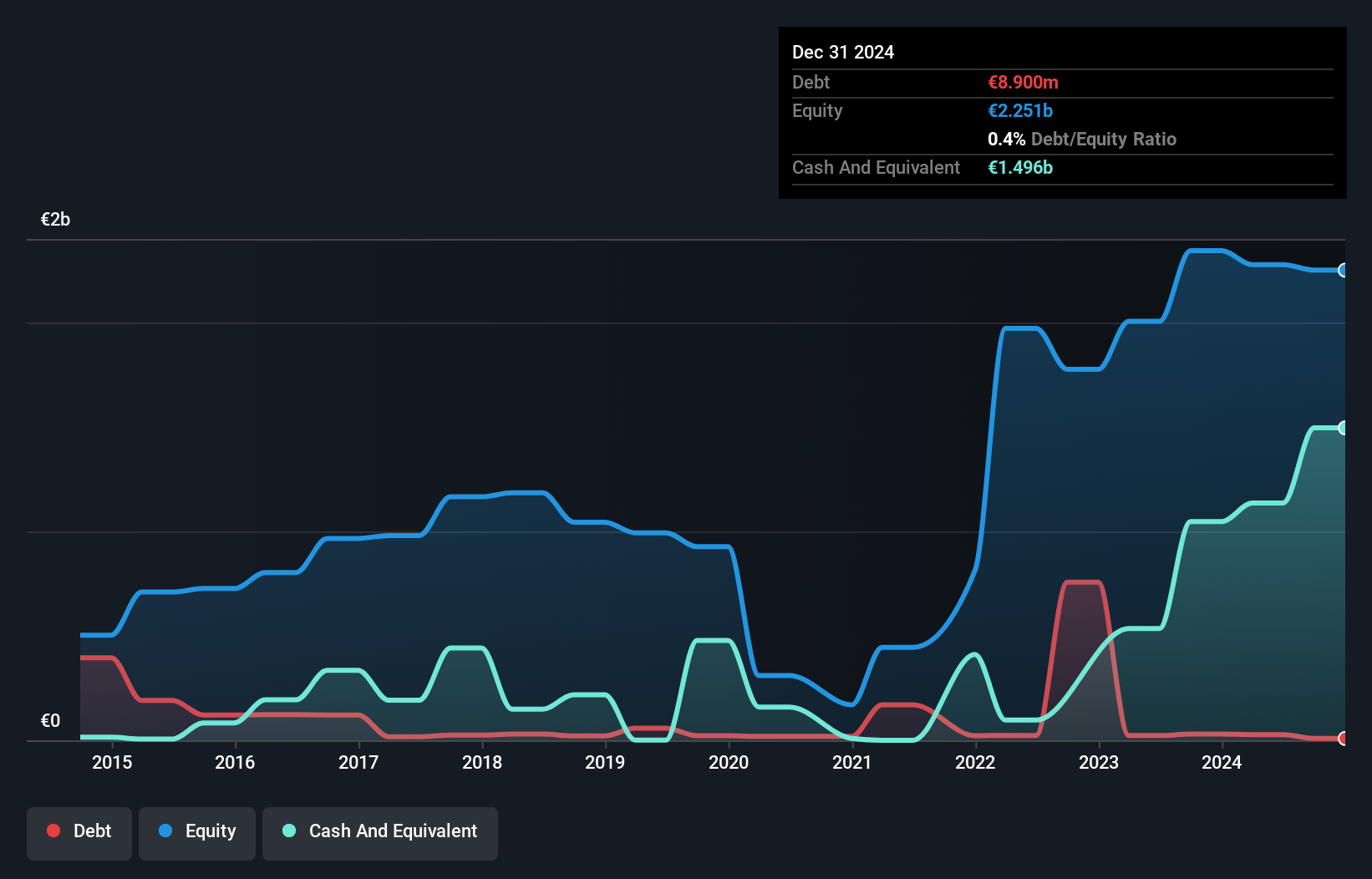

EssoF (ENXTPA:ES)

Simply Wall St Value Rating: ★★★★★★

Overview: Esso S.A.F. is involved in refining, distributing, and marketing refined petroleum products both in France and internationally with a market capitalization of approximately €1.30 billion.

Operations: Esso S.A.F. generates revenue primarily from its refining and distribution segment, which reported €18.93 billion. The company's financial performance is influenced by its operational costs within this segment, impacting overall profitability metrics such as net profit margin.

EssoF, a smaller player in the energy sector, has recently turned profitable, contrasting with the broader Oil and Gas industry's 11.8% earnings contraction. This shift is supported by high-quality past earnings and a significant reduction in its debt-to-equity ratio from 5.8 to 1.2 over five years, suggesting prudent financial management. The company trades at a substantial discount of 97% below its estimated fair value, indicating potential upside if market conditions align favorably. With more cash than total debt and positive free cash flow of US$790 million as of June 2024, EssoF seems well-positioned for future growth opportunities within the industry context.

- Delve into the full analysis health report here for a deeper understanding of EssoF.

Evaluate EssoF's historical performance by accessing our past performance report.

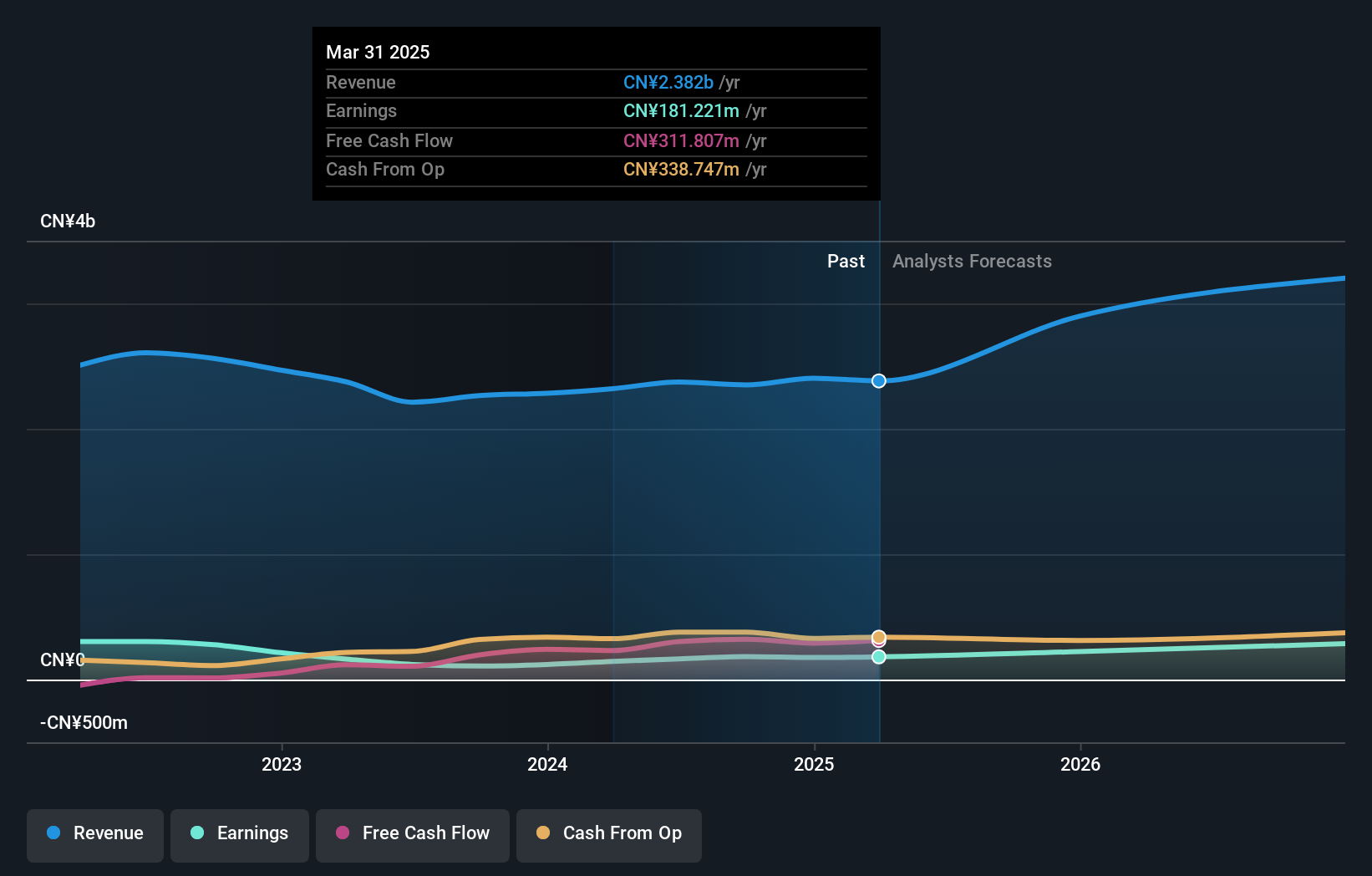

Lily Group (SHSE:603823)

Simply Wall St Value Rating: ★★★★★★

Overview: Lily Group Co., Ltd. is a company that manufactures and sells organic pigments in the People’s Republic of China, with a market capitalization of approximately CN¥4.26 billion.

Operations: Lily Group generates revenue primarily from its chemicals segment, amounting to CN¥2.34 billion. The company's financials include a segment adjustment of CN¥15.54 million.

Lily Group has been making waves with its impressive earnings growth, outpacing the chemicals industry by a significant margin of 69.5% over the past year. The company's net income for the nine months ending September 2024 was CNY 143.83 million, up from CNY 81.31 million in the previous year, showcasing robust financial health. With interest payments well covered by EBIT at a remarkable 71 times coverage and trading at nearly half of its estimated fair value, Lily Group seems undervalued with strong potential for future appreciation. Additionally, their debt to equity ratio has improved from 8.3 to 6.9 over five years, indicating prudent financial management and stability in operations.

- Take a closer look at Lily Group's potential here in our health report.

Examine Lily Group's past performance report to understand how it has performed in the past.

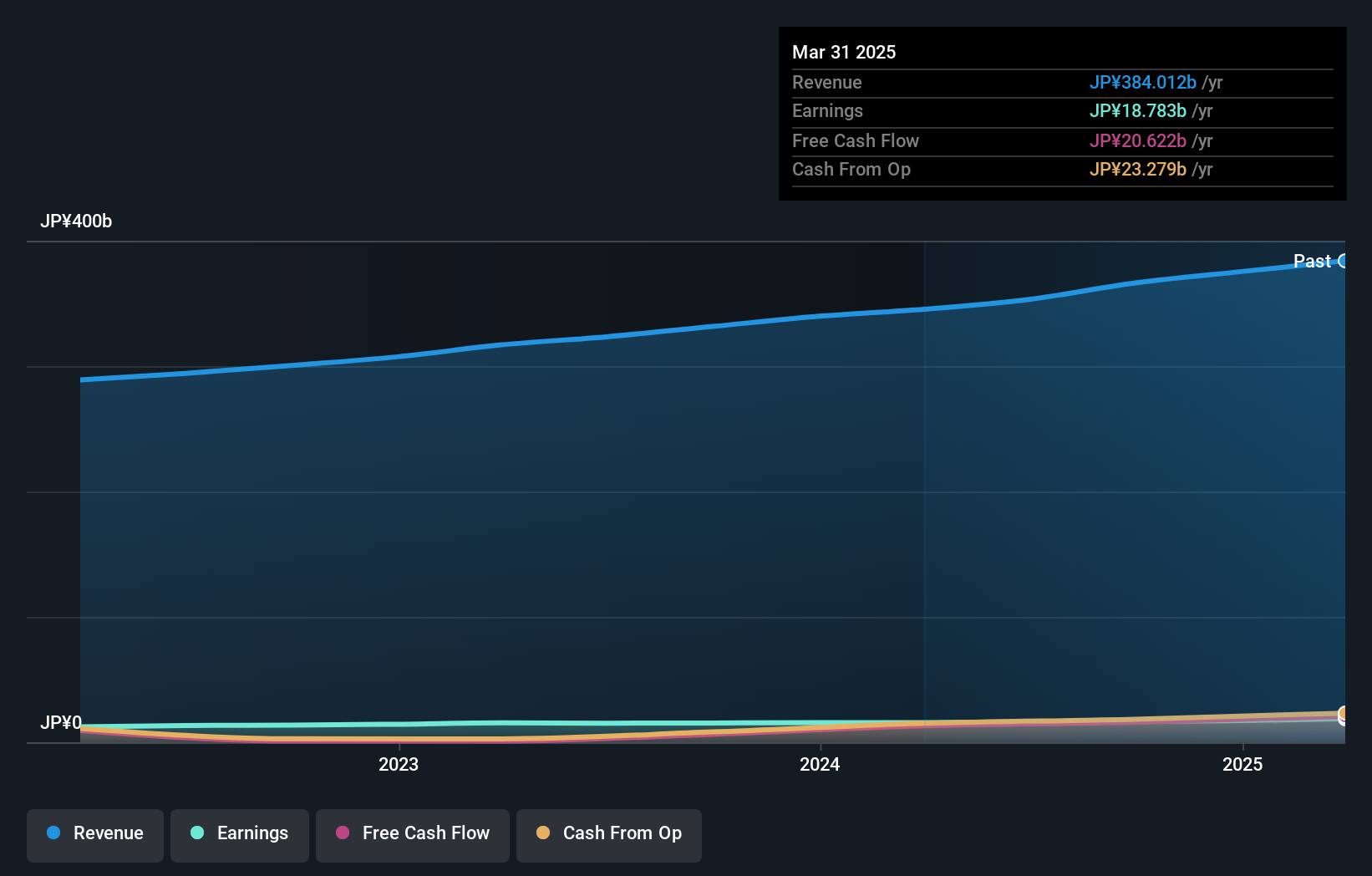

Inaba Denki SangyoLtd (TSE:9934)

Simply Wall St Value Rating: ★★★★★★

Overview: Inaba Denki Sangyo Co., Ltd. operates in Japan, offering electrical equipment and materials, industrial automation solutions, and proprietary products with a market capitalization of ¥217.85 billion.

Operations: Inaba Denki Sangyo generates revenue primarily from its Electrical Equipment Materials segment, which contributes ¥258.02 billion, followed by the In-House Product Business at ¥78.12 billion and the Industrial Equipment Business at ¥37.46 billion. The company exhibits a net profit margin trend that is noteworthy for analysis in understanding its financial health and efficiency over time.

Inaba Denki Sangyo, a small yet promising player in the trade distribution industry, has shown commendable financial health with earnings growth of 7.6% over the past year, outpacing the industry's 4.9%. The company is trading at a notable 16.4% below its estimated fair value, suggesting potential undervaluation. With more cash than total debt and positive free cash flow of ¥13.14 million as of March 2024, financial stability appears strong. Its high-quality earnings further bolster confidence in its performance amidst plans to announce Q2 results soon, potentially offering insights into future growth trajectories within its sector.

- Click to explore a detailed breakdown of our findings in Inaba Denki SangyoLtd's health report.

Assess Inaba Denki SangyoLtd's past performance with our detailed historical performance reports.

Turning Ideas Into Actions

- Unlock more gems! Our Undiscovered Gems With Strong Fundamentals screener has unearthed 4641 more companies for you to explore.Click here to unveil our expertly curated list of 4644 Undiscovered Gems With Strong Fundamentals.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if EssoF might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:ES

EssoF

Esso S.A.F. refines, distributes, and markets oil products in France and internationally.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|41.9% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|14.1% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$613.59|1.3% undervalued

AN

Based on Analyst Price Targets