Advertisement

- China

- /

- Basic Materials

- /

- SHSE:600449

Market Might Still Lack Some Conviction On Ningxia Building Materials Group Co.,Ltd (SHSE:600449) Even After 29% Share Price Boost

Ningxia Building Materials Group Co.,Ltd (SHSE:600449) shareholders would be excited to see that the share price has had a great month, posting a 29% gain and recovering from prior weakness. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 28% in the last twelve months.

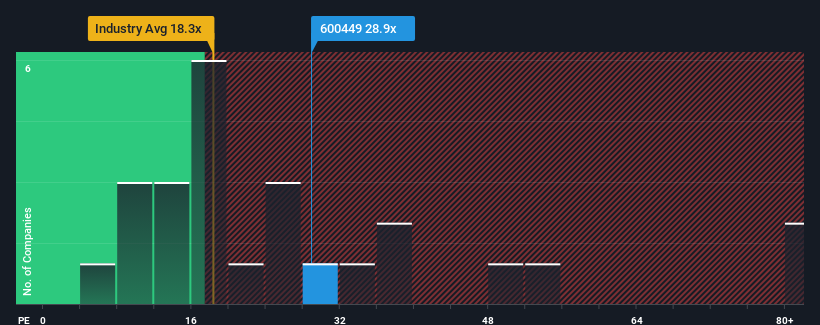

Even after such a large jump in price, there still wouldn't be many who think Ningxia Building Materials GroupLtd's price-to-earnings (or "P/E") ratio of 28.9x is worth a mention when the median P/E in China is similar at about 29x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

Recent times haven't been advantageous for Ningxia Building Materials GroupLtd as its earnings have been falling quicker than most other companies. It might be that many expect the dismal earnings performance to revert back to market averages soon, which has kept the P/E from falling. You'd much rather the company wasn't bleeding earnings if you still believe in the business. If not, then existing shareholders may be a little nervous about the viability of the share price.

Check out our latest analysis for Ningxia Building Materials GroupLtd

How Is Ningxia Building Materials GroupLtd's Growth Trending?

The only time you'd be comfortable seeing a P/E like Ningxia Building Materials GroupLtd's is when the company's growth is tracking the market closely.

Retrospectively, the last year delivered a frustrating 34% decrease to the company's bottom line. The last three years don't look nice either as the company has shrunk EPS by 79% in aggregate. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Turning to the outlook, the next three years should generate growth of 25% per year as estimated by the sole analyst watching the company. That's shaping up to be materially higher than the 19% per annum growth forecast for the broader market.

In light of this, it's curious that Ningxia Building Materials GroupLtd's P/E sits in line with the majority of other companies. It may be that most investors aren't convinced the company can achieve future growth expectations.

The Bottom Line On Ningxia Building Materials GroupLtd's P/E

Ningxia Building Materials GroupLtd's stock has a lot of momentum behind it lately, which has brought its P/E level with the market. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

Our examination of Ningxia Building Materials GroupLtd's analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E as much as we would have predicted. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing pressure on the P/E ratio. It appears some are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

Before you settle on your opinion, we've discovered 3 warning signs for Ningxia Building Materials GroupLtd that you should be aware of.

Of course, you might also be able to find a better stock than Ningxia Building Materials GroupLtd. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Ningxia Building Materials GroupLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600449

Ningxia Building Materials GroupLtd

Manufactures and sells cement, cement clinkers, concrete, and aggregates in China.

Undervalued with excellent balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.5% undervalued

GM

Community Contributor