- China

- /

- Metals and Mining

- /

- SHSE:600392

There's Reason For Concern Over Shenghe Resources Holding Co., Ltd's (SHSE:600392) Massive 25% Price Jump

Shenghe Resources Holding Co., Ltd (SHSE:600392) shareholders are no doubt pleased to see that the share price has bounced 25% in the last month, although it is still struggling to make up recently lost ground. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 38% over that time.

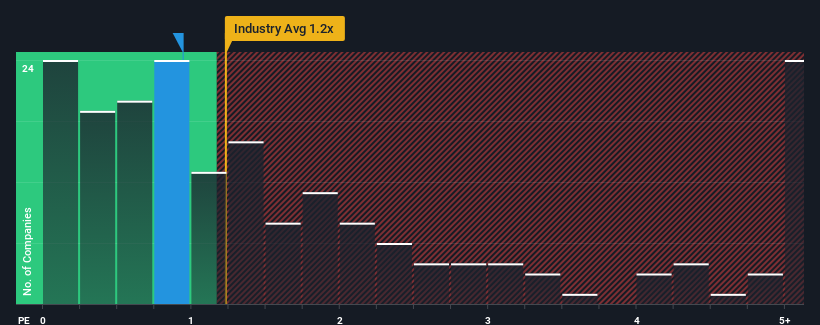

In spite of the firm bounce in price, it's still not a stretch to say that Shenghe Resources Holding's price-to-sales (or "P/S") ratio of 0.9x right now seems quite "middle-of-the-road" compared to the Metals and Mining industry in China, where the median P/S ratio is around 1.2x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

View our latest analysis for Shenghe Resources Holding

How Shenghe Resources Holding Has Been Performing

Recent times have been advantageous for Shenghe Resources Holding as its revenues have been rising faster than most other companies. It might be that many expect the strong revenue performance to wane, which has kept the P/S ratio from rising. If not, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Shenghe Resources Holding.How Is Shenghe Resources Holding's Revenue Growth Trending?

Shenghe Resources Holding's P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

If we review the last year of revenue growth, the company posted a worthy increase of 8.2%. The latest three year period has also seen an excellent 141% overall rise in revenue, aided somewhat by its short-term performance. So we can start by confirming that the company has done a great job of growing revenues over that time.

Shifting to the future, estimates from the four analysts covering the company suggest revenue should grow by 1.4% over the next year. With the industry predicted to deliver 15% growth, the company is positioned for a weaker revenue result.

With this in mind, we find it intriguing that Shenghe Resources Holding's P/S is closely matching its industry peers. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. Maintaining these prices will be difficult to achieve as this level of revenue growth is likely to weigh down the shares eventually.

What Does Shenghe Resources Holding's P/S Mean For Investors?

Its shares have lifted substantially and now Shenghe Resources Holding's P/S is back within range of the industry median. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Given that Shenghe Resources Holding's revenue growth projections are relatively subdued in comparison to the wider industry, it comes as a surprise to see it trading at its current P/S ratio. When we see companies with a relatively weaker revenue outlook compared to the industry, we suspect the share price is at risk of declining, sending the moderate P/S lower. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

And what about other risks? Every company has them, and we've spotted 3 warning signs for Shenghe Resources Holding you should know about.

If you're unsure about the strength of Shenghe Resources Holding's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600392

Shenghe Resources Holding

Engages in the research and development, production, and supply of rare earth and related products in China and internationally.

High growth potential with adequate balance sheet.

Market Insights

Community Narratives