Investors are selling off Weifang Yaxing Chemical (SHSE:600319), lack of profits no doubt contribute to shareholders three-year loss

It is a pleasure to report that the Weifang Yaxing Chemical Co., Ltd. (SHSE:600319) is up 31% in the last quarter. It's not great that the stock is down over the last three years. But on the bright side, its return of -10%, is better than the market, which is down 13%.

After losing 12% this past week, it's worth investigating the company's fundamentals to see what we can infer from past performance.

View our latest analysis for Weifang Yaxing Chemical

Weifang Yaxing Chemical wasn't profitable in the last twelve months, it is unlikely we'll see a strong correlation between its share price and its earnings per share (EPS). Arguably revenue is our next best option. When a company doesn't make profits, we'd generally hope to see good revenue growth. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

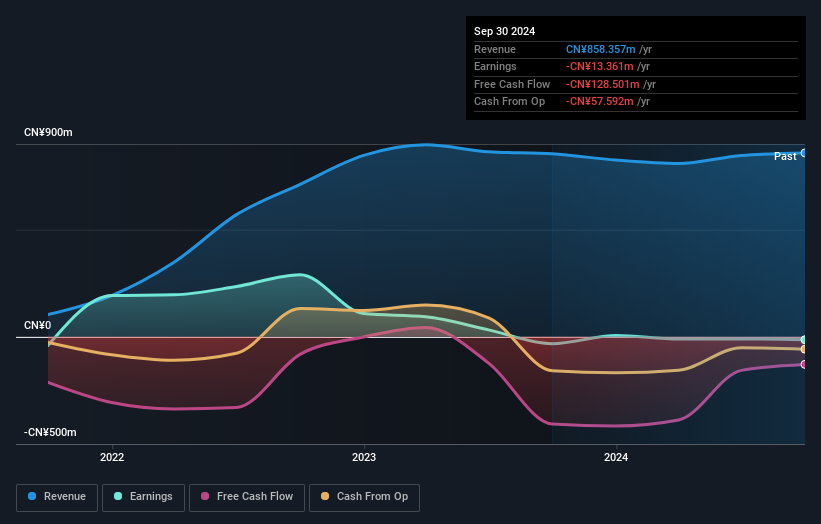

In the last three years, Weifang Yaxing Chemical saw its revenue grow by 35% per year, compound. That is faster than most pre-profit companies. It saw its share price decline by 3% per year over the last three. Given the revenue growth, it may simply be that the stock is suffering from market conditions. That means now could be exactly the right time to take a closer look at this business. Could the current price be an opportunity?

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

You can see how its balance sheet has strengthened (or weakened) over time in this free interactive graphic.

A Different Perspective

Investors in Weifang Yaxing Chemical had a tough year, with a total loss of 9.8%, against a market gain of about 14%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. On the bright side, long term shareholders have made money, with a gain of 1.1% per year over half a decade. If the fundamental data continues to indicate long term sustainable growth, the current sell-off could be an opportunity worth considering. Shareholders might want to examine this detailed historical graph of past earnings, revenue and cash flow.

Of course Weifang Yaxing Chemical may not be the best stock to buy. So you may wish to see this free collection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Chinese exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Weifang Yaxing Chemical might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600319

Weifang Yaxing Chemical

Engages in the research and development, production, operation, import, and sale of chemical materials in China and internationally.

Imperfect balance sheet and overvalued.