Advertisement

- China

- /

- Specialty Stores

- /

- SZSE:300622

What Doctorglasses Chain Co.,Ltd.'s (SZSE:300622) 32% Share Price Gain Is Not Telling You

Despite an already strong run, Doctorglasses Chain Co.,Ltd. (SZSE:300622) shares have been powering on, with a gain of 32% in the last thirty days. The annual gain comes to 199% following the latest surge, making investors sit up and take notice.

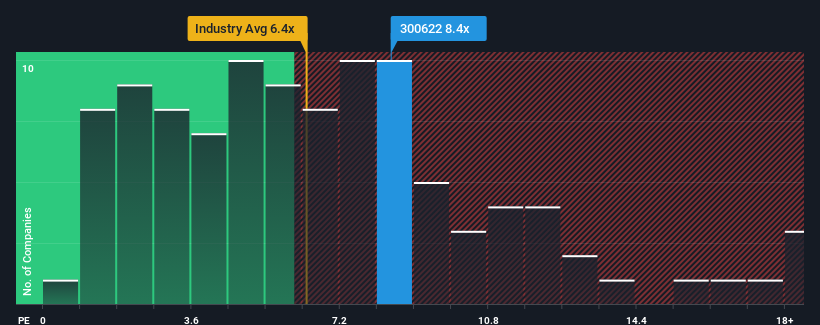

Since its price has surged higher, Doctorglasses ChainLtd may be sending sell signals at present with a price-to-sales (or "P/S") ratio of 8.4x, when you consider almost half of the companies in the Medical Equipment industry in China have P/S ratios under 6.4x and even P/S lower than 3x aren't out of the ordinary. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for Doctorglasses ChainLtd

What Does Doctorglasses ChainLtd's P/S Mean For Shareholders?

There hasn't been much to differentiate Doctorglasses ChainLtd's and the industry's revenue growth lately. Perhaps the market is expecting future revenue performance to improve, justifying the currently elevated P/S. If not, then existing shareholders may be a little nervous about the viability of the share price.

Keen to find out how analysts think Doctorglasses ChainLtd's future stacks up against the industry? In that case, our free report is a great place to start.How Is Doctorglasses ChainLtd's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as high as Doctorglasses ChainLtd's is when the company's growth is on track to outshine the industry.

Taking a look back first, we see that the company managed to grow revenues by a handy 4.3% last year. The latest three year period has also seen an excellent 36% overall rise in revenue, aided somewhat by its short-term performance. So we can start by confirming that the company has done a great job of growing revenues over that time.

Shifting to the future, estimates from the dual analysts covering the company suggest revenue should grow by 16% over the next year. With the industry predicted to deliver 25% growth, the company is positioned for a weaker revenue result.

In light of this, it's alarming that Doctorglasses ChainLtd's P/S sits above the majority of other companies. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

What Does Doctorglasses ChainLtd's P/S Mean For Investors?

Doctorglasses ChainLtd's P/S is on the rise since its shares have risen strongly. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

It comes as a surprise to see Doctorglasses ChainLtd trade at such a high P/S given the revenue forecasts look less than stellar. Right now we aren't comfortable with the high P/S as the predicted future revenues aren't likely to support such positive sentiment for long. At these price levels, investors should remain cautious, particularly if things don't improve.

Plus, you should also learn about these 3 warning signs we've spotted with Doctorglasses ChainLtd (including 1 which is a bit unpleasant).

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300622

Excellent balance sheet with limited growth.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor