Advertisement

- China

- /

- Medical Equipment

- /

- SHSE:688677

Further Upside For Qingdao NovelBeam Technology Co.,Ltd. (SHSE:688677) Shares Could Introduce Price Risks After 41% Bounce

Qingdao NovelBeam Technology Co.,Ltd. (SHSE:688677) shareholders would be excited to see that the share price has had a great month, posting a 41% gain and recovering from prior weakness. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 30% over that time.

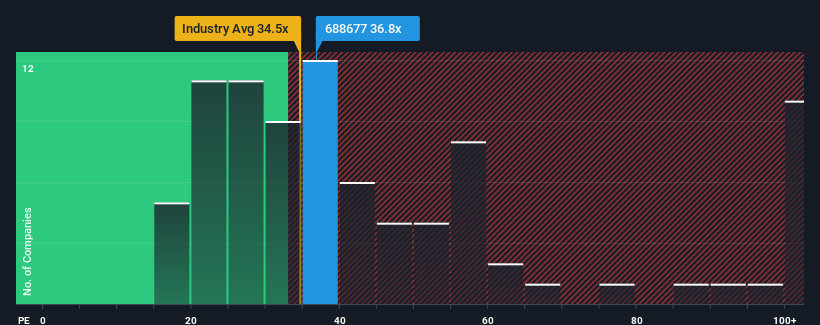

Even after such a large jump in price, you could still be forgiven for feeling indifferent about Qingdao NovelBeam TechnologyLtd's P/E ratio of 36.8x, since the median price-to-earnings (or "P/E") ratio in China is also close to 34x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

Qingdao NovelBeam TechnologyLtd has been struggling lately as its earnings have declined faster than most other companies. It might be that many expect the dismal earnings performance to revert back to market averages soon, which has kept the P/E from falling. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. If not, then existing shareholders may be a little nervous about the viability of the share price.

See our latest analysis for Qingdao NovelBeam TechnologyLtd

Is There Some Growth For Qingdao NovelBeam TechnologyLtd?

The only time you'd be comfortable seeing a P/E like Qingdao NovelBeam TechnologyLtd's is when the company's growth is tracking the market closely.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 34%. Unfortunately, that's brought it right back to where it started three years ago with EPS growth being virtually non-existent overall during that time. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Shifting to the future, estimates from the six analysts covering the company suggest earnings should grow by 37% per year over the next three years. With the market only predicted to deliver 19% per annum, the company is positioned for a stronger earnings result.

In light of this, it's curious that Qingdao NovelBeam TechnologyLtd's P/E sits in line with the majority of other companies. It may be that most investors aren't convinced the company can achieve future growth expectations.

The Bottom Line On Qingdao NovelBeam TechnologyLtd's P/E

Its shares have lifted substantially and now Qingdao NovelBeam TechnologyLtd's P/E is also back up to the market median. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of Qingdao NovelBeam TechnologyLtd's analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E as much as we would have predicted. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing pressure on the P/E ratio. It appears some are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Qingdao NovelBeam TechnologyLtd you should know about.

If you're unsure about the strength of Qingdao NovelBeam TechnologyLtd's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Qingdao NovelBeam TechnologyLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688677

Qingdao NovelBeam TechnologyLtd

Engages in the research, development, production, and sales of medical endoscopic instruments and optical products worldwide.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor