- China

- /

- Electronic Equipment and Components

- /

- SHSE:688100

3 Growth Companies With Insider Ownership Up To 35%

Reviewed by Simply Wall St

In the current global market landscape, uncertainty surrounding tariffs and mixed economic signals have led to cautious investor sentiment, with major U.S. indices experiencing slight declines. Despite these challenges, many investors are turning their attention to growth companies where high insider ownership can signal confidence in a company's long-term potential.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 50.1% |

| Seojin SystemLtd (KOSDAQ:A178320) | 32.1% | 39.9% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 26.2% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Laopu Gold (SEHK:6181) | 36.4% | 38.2% |

| Pricol (NSEI:PRICOLLTD) | 25.4% | 25.2% |

| Medley (TSE:4480) | 34.1% | 27.3% |

| Plenti Group (ASX:PLT) | 12.7% | 120.1% |

| Fulin Precision (SZSE:300432) | 13.6% | 71% |

| Findi (ASX:FND) | 35.8% | 111.4% |

Let's dive into some prime choices out of the screener.

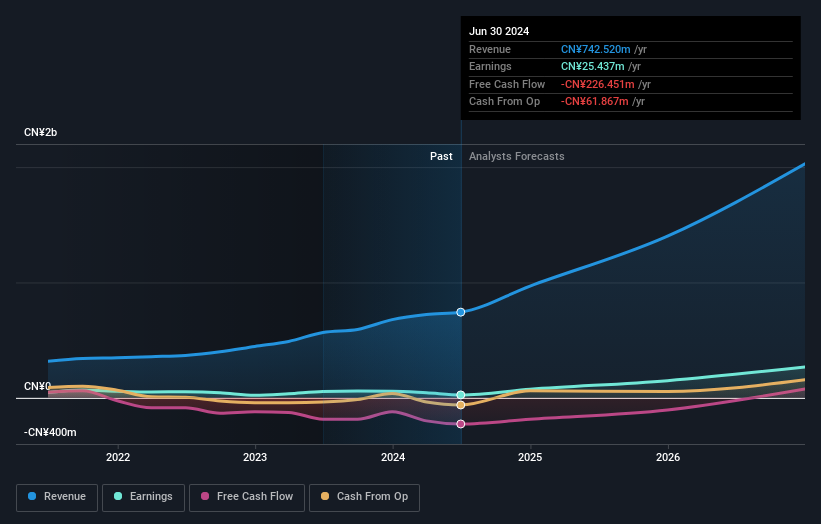

Willfar Information Technology (SHSE:688100)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Willfar Information Technology Co., Ltd. offers smart utility services and IoT solutions both in China and internationally, with a market cap of CN¥18.10 billion.

Operations: Willfar Information Technology Co., Ltd. generates revenue through its smart utility services and IoT solutions across domestic and international markets.

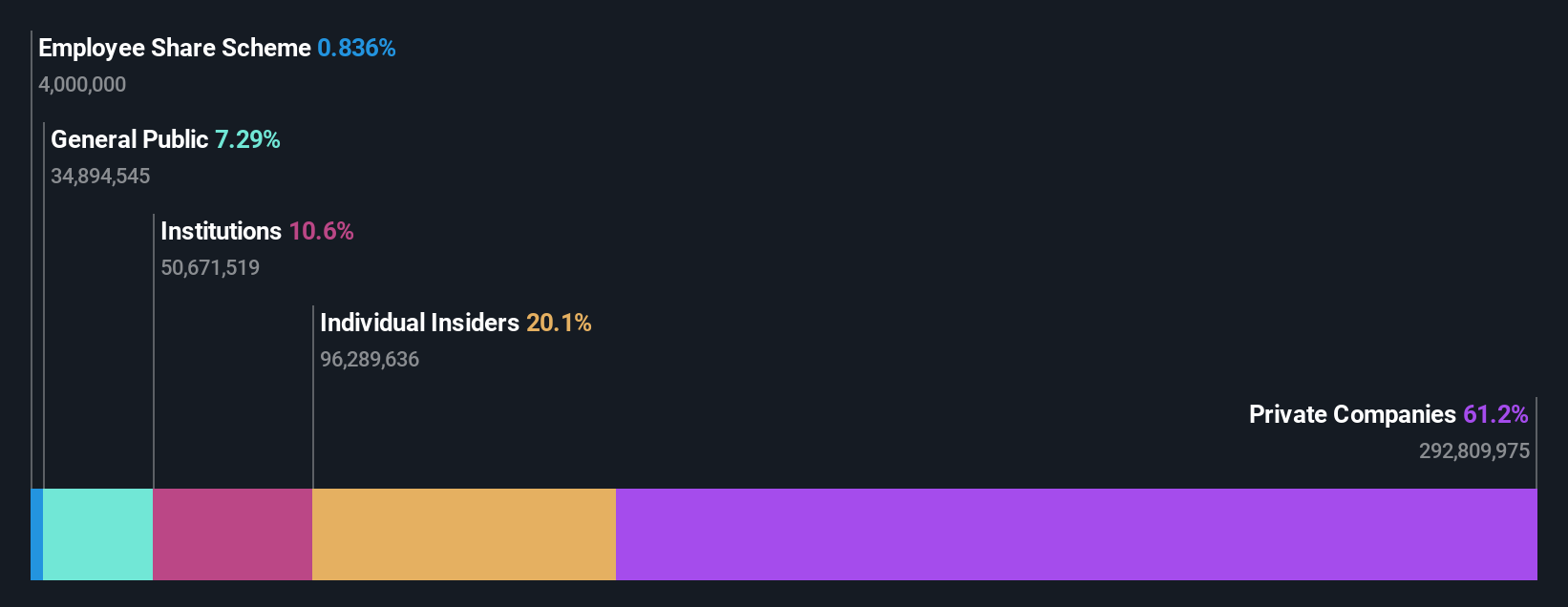

Insider Ownership: 21.2%

Willfar Information Technology is positioned for robust growth, with revenue projected to increase by 21.3% annually, outpacing the broader Chinese market. Despite a price-to-earnings ratio of 30.6x, it remains attractively valued compared to peers and the market average of 36.4x. A recent CNY 150 million share buyback plan underscores management's confidence in future prospects and commitment to shareholder value through equity incentives or employee stock ownership plans.

- Get an in-depth perspective on Willfar Information Technology's performance by reading our analyst estimates report here.

- Upon reviewing our latest valuation report, Willfar Information Technology's share price might be too pessimistic.

Shanghai Aohua Photoelectricity Endoscope (SHSE:688212)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shanghai Aohua Photoelectricity Endoscope Co., Ltd. operates in the medical equipment industry, focusing on the development and production of endoscopic devices, with a market cap of CN¥5.66 billion.

Operations: The company generates revenue primarily from its diagnostic kits and equipment segment, totaling CN¥750.04 million.

Insider Ownership: 32.3%

Shanghai Aohua Photoelectricity Endoscope is poised for significant growth, with earnings expected to rise by 59.9% annually, surpassing the broader market's pace. Despite a decline in profit margins from 9.8% to 6.7%, the company trades at a discount of 20.8% below its estimated fair value. A CNY 200 million share buyback plan reflects management's confidence, funded partly by a special loan and aimed at equity incentives or employee stock ownership plans.

- Click to explore a detailed breakdown of our findings in Shanghai Aohua Photoelectricity Endoscope's earnings growth report.

- In light of our recent valuation report, it seems possible that Shanghai Aohua Photoelectricity Endoscope is trading behind its estimated value.

Suzhou Sunmun Technology (SZSE:300522)

Simply Wall St Growth Rating: ★★★★★★

Overview: Suzhou Sunmun Technology Co., Ltd. specializes in the research, production, and sale of nano-coloring materials, functional nano-dispersions, special additives, intelligent color matching systems, and electronic chemicals in China with a market cap of approximately CN¥4.61 billion.

Operations: Revenue Segments (in millions of CN¥): Nano-coloring materials: 1,200; Functional nano-dispersions: 950; Special additives: 780; Intelligent color matching systems: 640; Electronic chemicals: 1,150. Suzhou Sunmun Technology generates its revenue from nano-coloring materials (CN¥1.20 billion), functional nano-dispersions (CN¥950 million), special additives (CN¥780 million), intelligent color matching systems (CN¥640 million), and electronic chemicals (CN¥1.15 billion).

Insider Ownership: 35.4%

Suzhou Sunmun Technology is positioned for robust growth, with earnings projected to increase significantly at 92.8% annually, outpacing the CN market's 25.3%. Revenue is also expected to grow rapidly at 48.8% per year, well above the market average of 13.4%. Despite no substantial insider trading activity in recent months, its future return on equity is forecasted to reach a high level of 22.8%, indicating strong potential for value creation.

- Take a closer look at Suzhou Sunmun Technology's potential here in our earnings growth report.

- Upon reviewing our latest valuation report, Suzhou Sunmun Technology's share price might be too optimistic.

Summing It All Up

- Access the full spectrum of 1447 Fast Growing Companies With High Insider Ownership by clicking on this link.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Willfar Information Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688100

Willfar Information Technology

Provides smart utility services and IoT solutions in China and internationally.

High growth potential with solid track record.

Market Insights

Community Narratives