Shareholders Shouldn’t Be Too Comfortable With Tech-Bank Food's (SZSE:002124) Strong Earnings

Tech-Bank Food Co., Ltd. (SZSE:002124) recently released a strong earnings report, and the market responded by raising the share price. However, we think that shareholders should be aware of some other factors beyond the profit numbers.

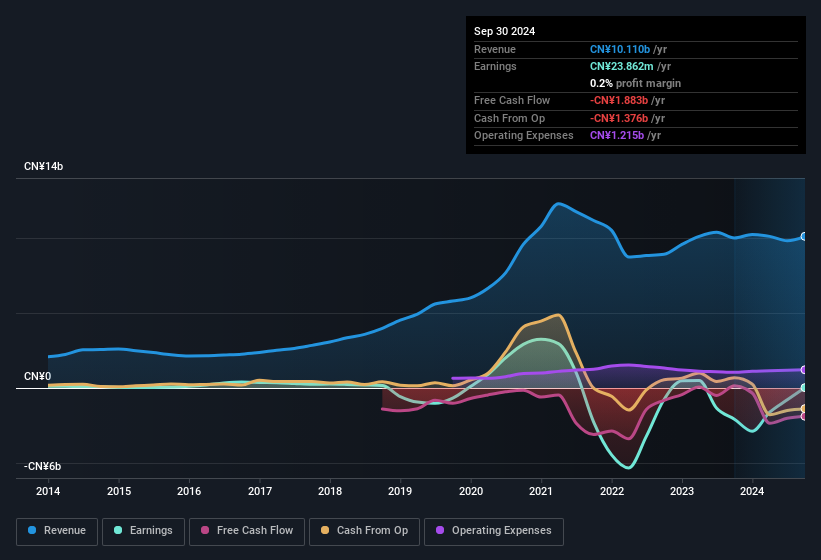

See our latest analysis for Tech-Bank Food

A Closer Look At Tech-Bank Food's Earnings

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. The ratio shows us how much a company's profit exceeds its FCF.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

Over the twelve months to September 2024, Tech-Bank Food recorded an accrual ratio of 0.28. Unfortunately, that means its free cash flow fell significantly short of its reported profits. Even though it reported a profit of CN¥23.9m, a look at free cash flow indicates it actually burnt through CN¥1.9b in the last year. It's worth noting that Tech-Bank Food generated positive FCF of CN¥145m a year ago, so at least they've done it in the past. Having said that, there is more to consider. We can look at how unusual items in the profit and loss statement impacted its accrual ratio, as well as explore how dilution is impacting shareholders negatively. One positive for Tech-Bank Food shareholders is that it's accrual ratio was significantly better last year, providing reason to believe that it may return to stronger cash conversion in the future. Shareholders should look for improved cashflow relative to profit in the current year, if that is indeed the case.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. Tech-Bank Food expanded the number of shares on issue by 21% over the last year. As a result, its net income is now split between a greater number of shares. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. Check out Tech-Bank Food's historical EPS growth by clicking on this link.

How Is Dilution Impacting Tech-Bank Food's Earnings Per Share (EPS)?

Three years ago, Tech-Bank Food lost money. Zooming in to the last year, we still can't talk about growth rates coherently, since it made a loss last year. But mathematics aside, it is always good to see when a formerly unprofitable business come good (though we accept profit would have been higher if dilution had not been required). And so, you can see quite clearly that dilution is influencing shareholder earnings.

If Tech-Bank Food's EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

How Do Unusual Items Influence Profit?

Given the accrual ratio, it's not overly surprising that Tech-Bank Food's profit was boosted by unusual items worth CN¥292m in the last twelve months. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. We ran the numbers on most publicly listed companies worldwide, and it's very common for unusual items to be once-off in nature. And, after all, that's exactly what the accounting terminology implies. We can see that Tech-Bank Food's positive unusual items were quite significant relative to its profit in the year to September 2024. All else being equal, this would likely have the effect of making the statutory profit a poor guide to underlying earnings power.

Our Take On Tech-Bank Food's Profit Performance

Tech-Bank Food didn't back up its earnings with free cashflow, but this isn't too surprising given profits were inflated by unusual items. Meanwhile, the new shares issued mean that shareholders now own less of the company, unless they tipped in more cash themselves. For all the reasons mentioned above, we think that, at a glance, Tech-Bank Food's statutory profits could be considered to be low quality, because they are likely to give investors an overly positive impression of the company. If you want to do dive deeper into Tech-Bank Food, you'd also look into what risks it is currently facing. To help with this, we've discovered 3 warning signs (2 make us uncomfortable!) that you ought to be aware of before buying any shares in Tech-Bank Food.

Our examination of Tech-Bank Food has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

Valuation is complex, but we're here to simplify it.

Discover if Tech-Bank Food might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002124

Tech-Bank Food

Tech-bank Food Co., Ltd., together with its subsidiaries, engages in the agriculture and animal husbandry businesses in China and internationally.

Good value with acceptable track record.

Similar Companies

Market Insights

Community Narratives