Advertisement

It's Down 26% But Zhengzhou Qianweiyangchu Food Co., Ltd. (SZSE:001215) Could Be Riskier Than It Looks

Zhengzhou Qianweiyangchu Food Co., Ltd. (SZSE:001215) shares have had a horrible month, losing 26% after a relatively good period beforehand. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 50% loss during that time.

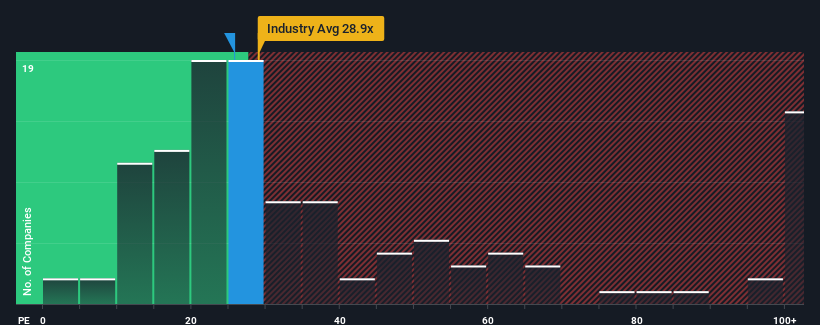

In spite of the heavy fall in price, Zhengzhou Qianweiyangchu Food's price-to-earnings (or "P/E") ratio of 25.8x might still make it look like a buy right now compared to the market in China, where around half of the companies have P/E ratios above 33x and even P/E's above 61x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

Recent times have been advantageous for Zhengzhou Qianweiyangchu Food as its earnings have been rising faster than most other companies. One possibility is that the P/E is low because investors think this strong earnings performance might be less impressive moving forward. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Zhengzhou Qianweiyangchu Food

Is There Any Growth For Zhengzhou Qianweiyangchu Food?

The only time you'd be truly comfortable seeing a P/E as low as Zhengzhou Qianweiyangchu Food's is when the company's growth is on track to lag the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 27% last year. Still, EPS has barely risen at all from three years ago in total, which is not ideal. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Turning to the outlook, the next year should generate growth of 50% as estimated by the analysts watching the company. That's shaping up to be materially higher than the 39% growth forecast for the broader market.

With this information, we find it odd that Zhengzhou Qianweiyangchu Food is trading at a P/E lower than the market. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

What We Can Learn From Zhengzhou Qianweiyangchu Food's P/E?

The softening of Zhengzhou Qianweiyangchu Food's shares means its P/E is now sitting at a pretty low level. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our examination of Zhengzhou Qianweiyangchu Food's analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E anywhere near as much as we would have predicted. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. It appears many are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

Plus, you should also learn about this 1 warning sign we've spotted with Zhengzhou Qianweiyangchu Food.

If these risks are making you reconsider your opinion on Zhengzhou Qianweiyangchu Food, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Zhengzhou Qianweiyangchu Food might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:001215

Zhengzhou Qianweiyangchu Food

Primarily engages in the provision of customized and standardized prefabricated semi-finished products for catering companies, group meals, hotels, and banquets in China.

Flawless balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor