Zhe Jiang Li Zi Yuan Food Co.,Ltd. (SHSE:605337) Shares Fly 27% But Investors Aren't Buying For Growth

Zhe Jiang Li Zi Yuan Food Co.,Ltd. (SHSE:605337) shares have continued their recent momentum with a 27% gain in the last month alone. The bad news is that even after the stocks recovery in the last 30 days, shareholders are still underwater by about 6.2% over the last year.

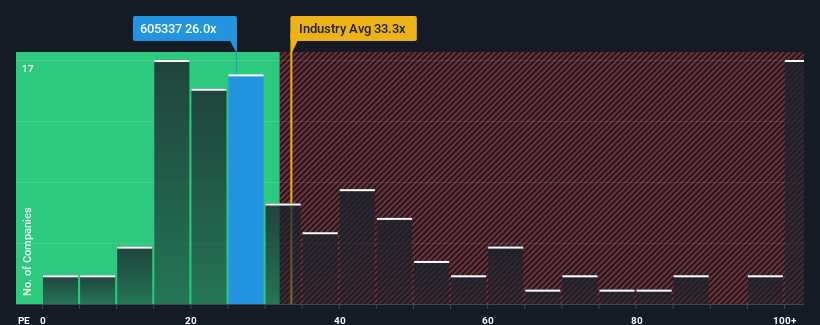

Even after such a large jump in price, Zhe Jiang Li Zi Yuan FoodLtd's price-to-earnings (or "P/E") ratio of 26x might still make it look like a buy right now compared to the market in China, where around half of the companies have P/E ratios above 38x and even P/E's above 74x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

With earnings that are retreating more than the market's of late, Zhe Jiang Li Zi Yuan FoodLtd has been very sluggish. The P/E is probably low because investors think this poor earnings performance isn't going to improve at all. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. If not, then existing shareholders will probably struggle to get excited about the future direction of the share price.

See our latest analysis for Zhe Jiang Li Zi Yuan FoodLtd

Is There Any Growth For Zhe Jiang Li Zi Yuan FoodLtd?

In order to justify its P/E ratio, Zhe Jiang Li Zi Yuan FoodLtd would need to produce sluggish growth that's trailing the market.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 20%. As a result, earnings from three years ago have also fallen 35% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Turning to the outlook, the next year should generate growth of 33% as estimated by the six analysts watching the company. That's shaping up to be materially lower than the 38% growth forecast for the broader market.

In light of this, it's understandable that Zhe Jiang Li Zi Yuan FoodLtd's P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Final Word

The latest share price surge wasn't enough to lift Zhe Jiang Li Zi Yuan FoodLtd's P/E close to the market median. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Zhe Jiang Li Zi Yuan FoodLtd's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

You always need to take note of risks, for example - Zhe Jiang Li Zi Yuan FoodLtd has 2 warning signs we think you should be aware of.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

Valuation is complex, but we're here to simplify it.

Discover if Zhe Jiang Li Zi Yuan FoodLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:605337

Zhe Jiang Li Zi Yuan FoodLtd

Engages in the research, production, and sale of milk-containing beverages and other beverages in China.

Excellent balance sheet and fair value.

Market Insights

Community Narratives