- China

- /

- Energy Services

- /

- SZSE:002278

Getting In Cheap On Shanghai SK Petroleum & Chemical Equipment Corporation Ltd. (SZSE:002278) Is Unlikely

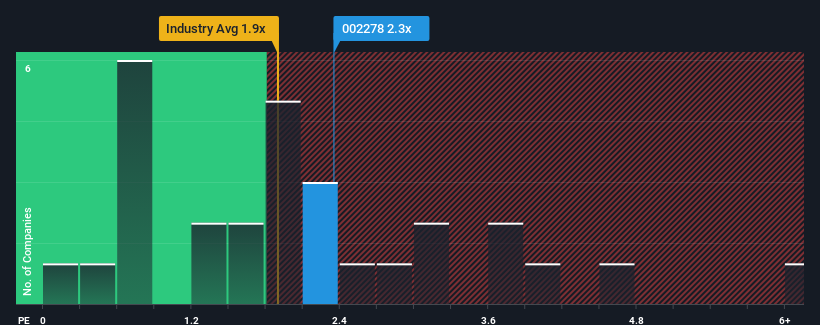

There wouldn't be many who think Shanghai SK Petroleum & Chemical Equipment Corporation Ltd.'s (SZSE:002278) price-to-sales (or "P/S") ratio of 2.3x is worth a mention when the median P/S for the Energy Services industry in China is similar at about 1.9x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

View our latest analysis for Shanghai SK Petroleum & Chemical Equipment

What Does Shanghai SK Petroleum & Chemical Equipment's P/S Mean For Shareholders?

Revenue has risen firmly for Shanghai SK Petroleum & Chemical Equipment recently, which is pleasing to see. One possibility is that the P/S is moderate because investors think this respectable revenue growth might not be enough to outperform the broader industry in the near future. If that doesn't eventuate, then existing shareholders probably aren't too pessimistic about the future direction of the share price.

Although there are no analyst estimates available for Shanghai SK Petroleum & Chemical Equipment, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.What Are Revenue Growth Metrics Telling Us About The P/S?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Shanghai SK Petroleum & Chemical Equipment's to be considered reasonable.

Taking a look back first, we see that the company managed to grow revenues by a handy 14% last year. However, due to its less than impressive performance prior to this period, revenue growth is practically non-existent over the last three years overall. Therefore, it's fair to say that revenue growth has been inconsistent recently for the company.

Comparing the recent medium-term revenue trends against the industry's one-year growth forecast of 18% shows it's noticeably less attractive.

With this in mind, we find it intriguing that Shanghai SK Petroleum & Chemical Equipment's P/S is comparable to that of its industry peers. Apparently many investors in the company are less bearish than recent times would indicate and aren't willing to let go of their stock right now. They may be setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

The Bottom Line On Shanghai SK Petroleum & Chemical Equipment's P/S

While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Our examination of Shanghai SK Petroleum & Chemical Equipment revealed its poor three-year revenue trends aren't resulting in a lower P/S as per our expectations, given they look worse than current industry outlook. Right now we are uncomfortable with the P/S as this revenue performance isn't likely to support a more positive sentiment for long. If recent medium-term revenue trends continue, the probability of a share price decline will become quite substantial, placing shareholders at risk.

There are also other vital risk factors to consider and we've discovered 4 warning signs for Shanghai SK Petroleum & Chemical Equipment (1 is potentially serious!) that you should be aware of before investing here.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002278

Shanghai SK Petroleum & Chemical Equipment

Engages in the research and development, and manufacture of petroleum and chemical equipment in China.

Adequate balance sheet low.