Advertisement

- China

- /

- Food and Staples Retail

- /

- SHSE:600827

Earnings growth of 6.7% over 3 years hasn't been enough to translate into positive returns for Shanghai Bailian (Group) (SHSE:600827) shareholders

In order to justify the effort of selecting individual stocks, it's worth striving to beat the returns from a market index fund. But its virtually certain that sometimes you will buy stocks that fall short of the market average returns. Unfortunately, that's been the case for longer term Shanghai Bailian (Group) Co., Ltd. (SHSE:600827) shareholders, since the share price is down 26% in the last three years, falling well short of the market decline of around 19%. Unfortunately the share price momentum is still quite negative, with prices down 19% in thirty days. But this could be related to poor market conditions -- stocks are down 11% in the same time.

Given the past week has been tough on shareholders, let's investigate the fundamentals and see what we can learn.

Check out our latest analysis for Shanghai Bailian (Group)

In his essay The Superinvestors of Graham-and-Doddsville Warren Buffett described how share prices do not always rationally reflect the value of a business. One way to examine how market sentiment has changed over time is to look at the interaction between a company's share price and its earnings per share (EPS).

Although the share price is down over three years, Shanghai Bailian (Group) actually managed to grow EPS by 22% per year in that time. This is quite a puzzle, and suggests there might be something temporarily buoying the share price. Alternatively, growth expectations may have been unreasonable in the past.

It's worth taking a look at other metrics, because the EPS growth doesn't seem to match with the falling share price.

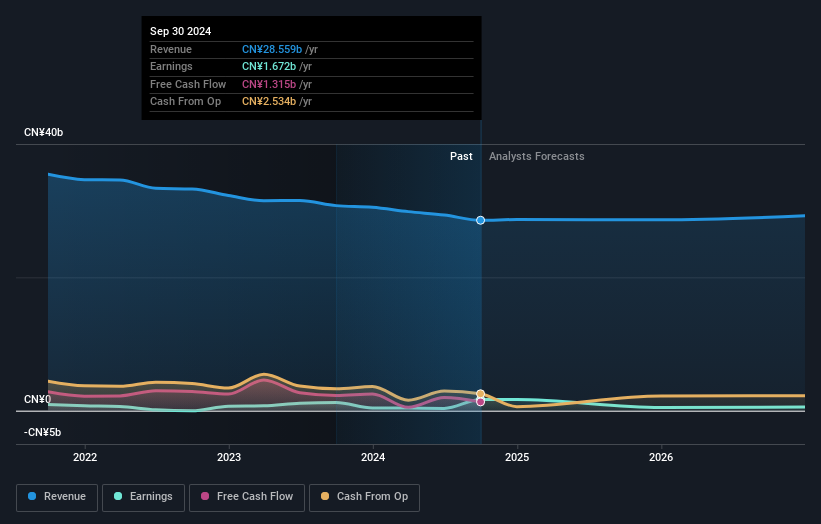

The modest 1.2% dividend yield is unlikely to be guiding the market view of the stock. Arguably the revenue decline of 6.9% per year has people thinking Shanghai Bailian (Group) is shrinking. After all, if revenue keeps shrinking, it may be difficult to find earnings growth in the future.

The graphic below depicts how earnings and revenue have changed over time (unveil the exact values by clicking on the image).

We know that Shanghai Bailian (Group) has improved its bottom line lately, but what does the future have in store? You can see what analysts are predicting for Shanghai Bailian (Group) in this interactive graph of future profit estimates.

What About Dividends?

It is important to consider the total shareholder return, as well as the share price return, for any given stock. Whereas the share price return only reflects the change in the share price, the TSR includes the value of dividends (assuming they were reinvested) and the benefit of any discounted capital raising or spin-off. So for companies that pay a generous dividend, the TSR is often a lot higher than the share price return. In the case of Shanghai Bailian (Group), it has a TSR of -23% for the last 3 years. That exceeds its share price return that we previously mentioned. This is largely a result of its dividend payments!

A Different Perspective

It's nice to see that Shanghai Bailian (Group) shareholders have received a total shareholder return of 8.0% over the last year. And that does include the dividend. Since the one-year TSR is better than the five-year TSR (the latter coming in at 3% per year), it would seem that the stock's performance has improved in recent times. Someone with an optimistic perspective could view the recent improvement in TSR as indicating that the business itself is getting better with time. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. For example, we've discovered 2 warning signs for Shanghai Bailian (Group) (1 is a bit unpleasant!) that you should be aware of before investing here.

Of course Shanghai Bailian (Group) may not be the best stock to buy. So you may wish to see this free collection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Chinese exchanges.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600827

Shanghai Bailian (Group)

Engages in retail business through department stores, and supermarket and specialty chains in China.

Adequate balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor