Advertisement

Investors Don't See Light At End Of BIEM.L.FDLKK Garment Co.,Ltd.'s (SZSE:002832) Tunnel And Push Stock Down 26%

The BIEM.L.FDLKK Garment Co.,Ltd. (SZSE:002832) share price has fared very poorly over the last month, falling by a substantial 26%. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 31% share price drop.

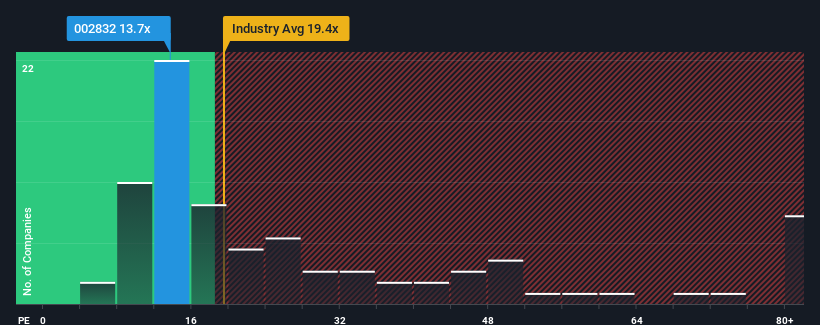

Although its price has dipped substantially, BIEM.L.FDLKK GarmentLtd may still be sending very bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 13.7x, since almost half of all companies in China have P/E ratios greater than 29x and even P/E's higher than 54x are not unusual. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

Recent times have been advantageous for BIEM.L.FDLKK GarmentLtd as its earnings have been rising faster than most other companies. One possibility is that the P/E is low because investors think this strong earnings performance might be less impressive moving forward. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

See our latest analysis for BIEM.L.FDLKK GarmentLtd

Is There Any Growth For BIEM.L.FDLKK GarmentLtd?

There's an inherent assumption that a company should far underperform the market for P/E ratios like BIEM.L.FDLKK GarmentLtd's to be considered reasonable.

Taking a look back first, we see that the company grew earnings per share by an impressive 19% last year. The latest three year period has also seen an excellent 63% overall rise in EPS, aided by its short-term performance. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Shifting to the future, estimates from the six analysts covering the company suggest earnings should grow by 18% per annum over the next three years. That's shaping up to be materially lower than the 25% per annum growth forecast for the broader market.

In light of this, it's understandable that BIEM.L.FDLKK GarmentLtd's P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Final Word

Shares in BIEM.L.FDLKK GarmentLtd have plummeted and its P/E is now low enough to touch the ground. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of BIEM.L.FDLKK GarmentLtd's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

Before you take the next step, you should know about the 2 warning signs for BIEM.L.FDLKK GarmentLtd (1 makes us a bit uncomfortable!) that we have uncovered.

If you're unsure about the strength of BIEM.L.FDLKK GarmentLtd's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if BIEM.L.FDLKK GarmentLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002832

BIEM.L.FDLKK GarmentLtd

Engages in the research and development, and design of branded apparel; and brand promotion, marketing network construction, and supply chain management activities in China.

Very undervalued with flawless balance sheet.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.0% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor