- China

- /

- Consumer Durables

- /

- SHSE:603389

More Unpleasant Surprises Could Be In Store For A-Zenith Home Furnishings Co., Ltd.'s (SHSE:603389) Shares After Tumbling 38%

A-Zenith Home Furnishings Co., Ltd. (SHSE:603389) shareholders that were waiting for something to happen have been dealt a blow with a 38% share price drop in the last month. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 13% in that time.

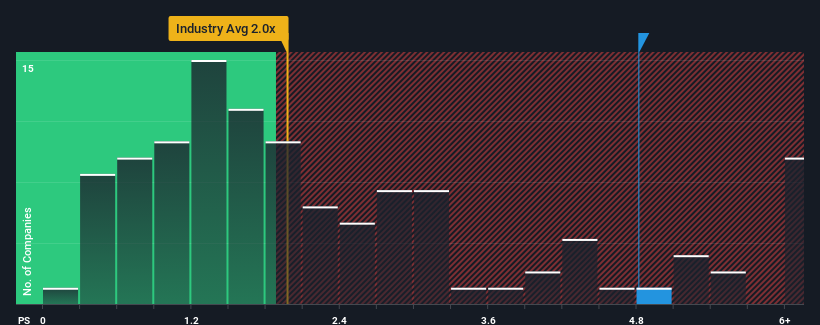

Although its price has dipped substantially, when almost half of the companies in China's Consumer Durables industry have price-to-sales ratios (or "P/S") below 2x, you may still consider A-Zenith Home Furnishings as a stock not worth researching with its 4.8x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

See our latest analysis for A-Zenith Home Furnishings

What Does A-Zenith Home Furnishings' Recent Performance Look Like?

As an illustration, revenue has deteriorated at A-Zenith Home Furnishings over the last year, which is not ideal at all. Perhaps the market believes the company can do enough to outperform the rest of the industry in the near future, which is keeping the P/S ratio high. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on A-Zenith Home Furnishings' earnings, revenue and cash flow.Is There Enough Revenue Growth Forecasted For A-Zenith Home Furnishings?

A-Zenith Home Furnishings' P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 2.0%. This means it has also seen a slide in revenue over the longer-term as revenue is down 17% in total over the last three years. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

In contrast to the company, the rest of the industry is expected to grow by 11% over the next year, which really puts the company's recent medium-term revenue decline into perspective.

With this in mind, we find it worrying that A-Zenith Home Furnishings' P/S exceeds that of its industry peers. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as a continuation of recent revenue trends is likely to weigh heavily on the share price eventually.

The Final Word

A significant share price dive has done very little to deflate A-Zenith Home Furnishings' very lofty P/S. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We've established that A-Zenith Home Furnishings currently trades on a much higher than expected P/S since its recent revenues have been in decline over the medium-term. With a revenue decline on investors' minds, the likelihood of a souring sentiment is quite high which could send the P/S back in line with what we'd expect. Unless the recent medium-term conditions improve markedly, investors will have a hard time accepting the share price as fair value.

And what about other risks? Every company has them, and we've spotted 3 warning signs for A-Zenith Home Furnishings you should know about.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603389

Low with imperfect balance sheet.

Market Insights

Community Narratives