Advertisement

- China

- /

- Consumer Durables

- /

- SZSE:301187

3 Stocks Estimated To Be Trading Below Fair Value In November 2024

Simply Wall St

Reviewed by Simply Wall St

As global markets react to the recent U.S. election results, with major indices reaching record highs driven by expectations of economic growth and regulatory changes, investors are keenly assessing opportunities amidst these shifting dynamics. In this context, identifying stocks that may be trading below their fair value becomes particularly intriguing, as they offer potential for growth in a market buoyed by optimism and policy shifts.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Micro-Star International (TWSE:2377) | NT$184.00 | NT$368.99 | 50.1% |

| Anhui Huaheng Biotechnology (SHSE:688639) | CN¥37.84 | CN¥71.65 | 47.2% |

| Jetpak Top Holding (OM:JETPAK) | SEK106.00 | SEK211.81 | 50% |

| Dynavox Group (OM:DYVOX) | SEK66.50 | SEK132.84 | 49.9% |

| Redcentric (AIM:RCN) | £1.1625 | £2.32 | 50% |

| Proficient Auto Logistics (NasdaqGS:PAL) | US$10.00 | US$19.92 | 49.8% |

| Royal Plus (SET:PLUS) | THB5.45 | THB10.88 | 49.9% |

| Dometic Group (OM:DOM) | SEK61.15 | SEK121.72 | 49.8% |

| Fine Foods & Pharmaceuticals N.T.M (BIT:FF) | €8.14 | €16.25 | 49.9% |

| St. James's Place (LSE:STJ) | £8.275 | £16.46 | 49.7% |

Let's take a closer look at a couple of our picks from the screened companies.

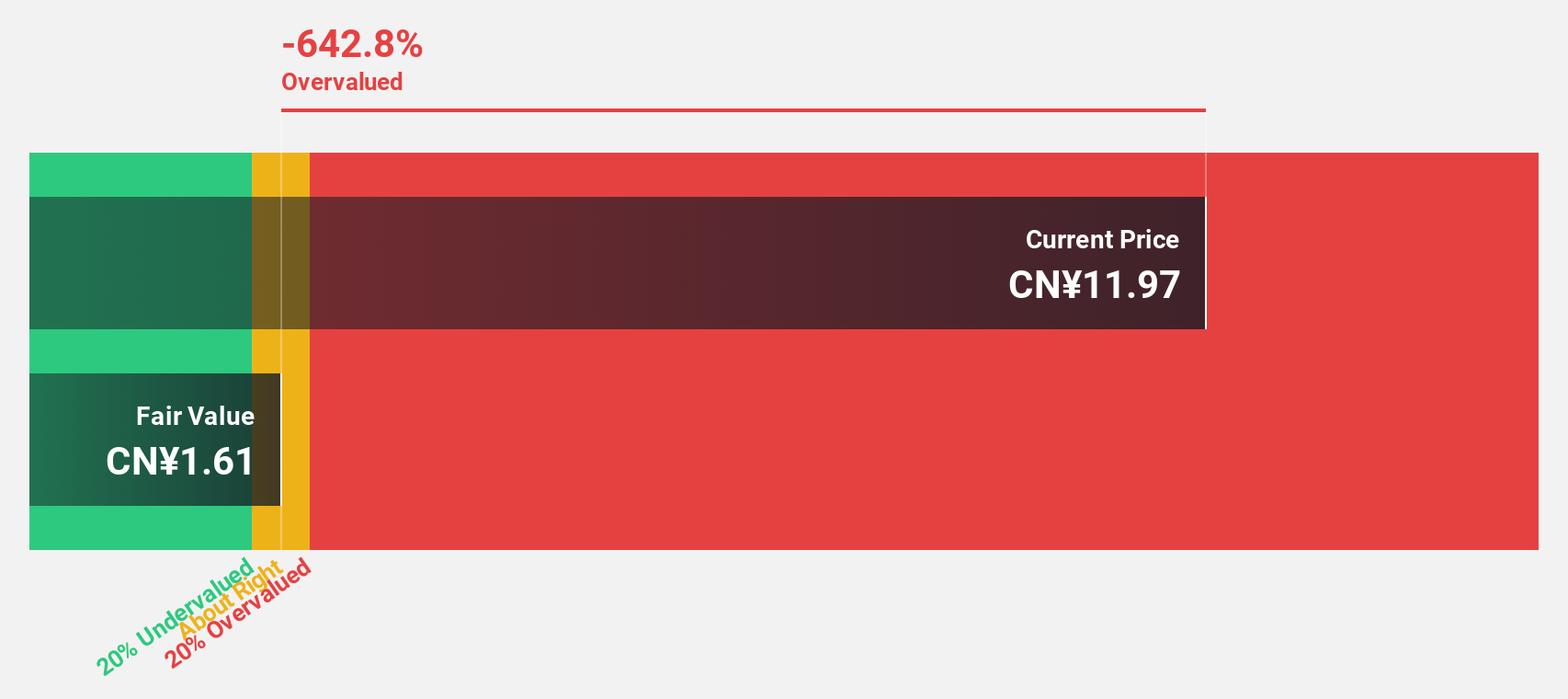

Hui Lyu Ecological Technology GroupsLtd (SZSE:001267)

Overview: Hui Lyu Ecological Technology Groups Co., Ltd. operates in the ecological technology sector and has a market cap of CN¥6.03 billion.

Operations: Unfortunately, the provided text for revenue segments is incomplete and does not contain specific information about the company's revenue breakdown. If you have additional details or a complete list of revenue segments, please provide it so I can assist you further.

Estimated Discount To Fair Value: 22%

Hui Lyu Ecological Technology Groups Ltd. is trading at CN¥7.92, which is 22% below its estimated fair value of CN¥10.15, suggesting potential undervaluation based on cash flows. Despite a low forecasted return on equity (10.1%), the company's earnings are projected to grow significantly at 41.5% annually over the next three years, outpacing the Chinese market's growth rate of 26.2%. Recent earnings showed slight improvement in net income despite declining sales.

- In light of our recent growth report, it seems possible that Hui Lyu Ecological Technology GroupsLtd's financial performance will exceed current levels.

- Click here and access our complete balance sheet health report to understand the dynamics of Hui Lyu Ecological Technology GroupsLtd.

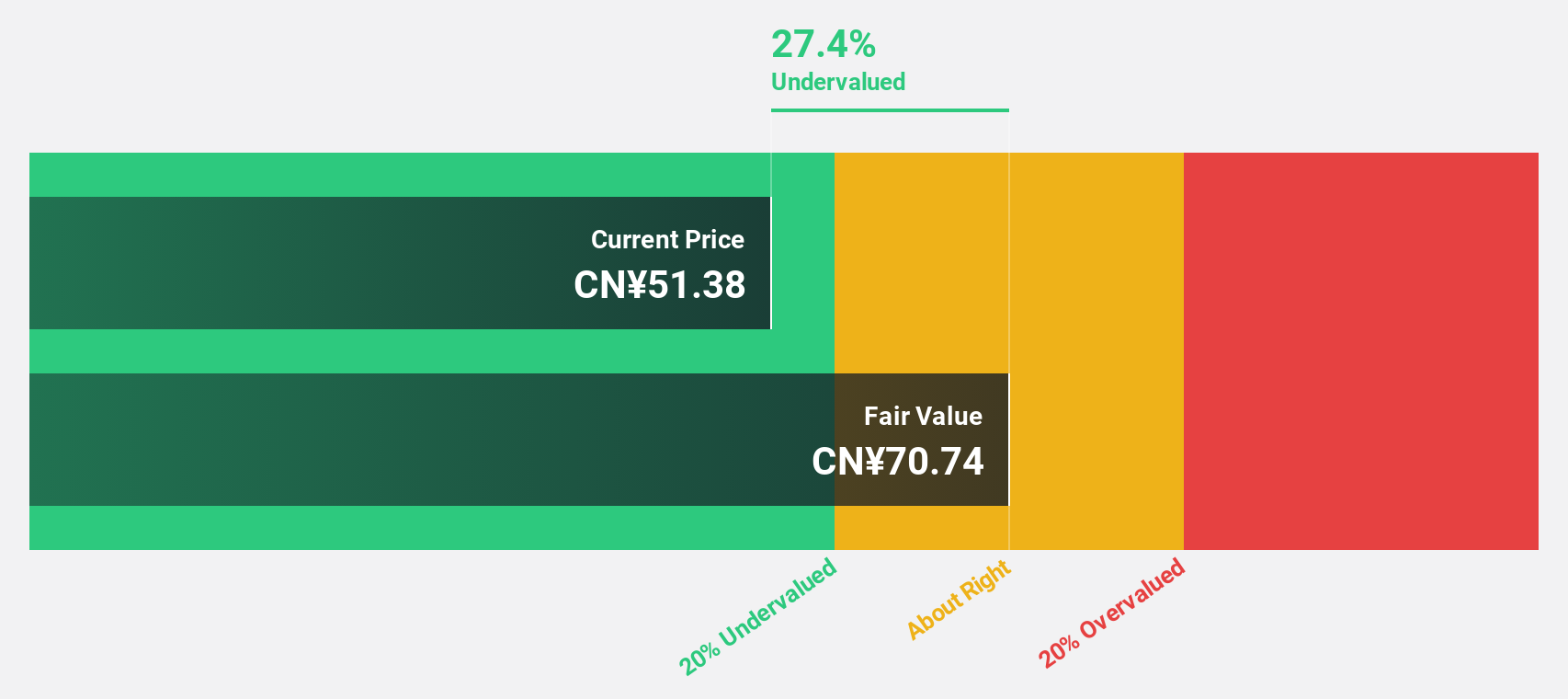

AcrobiosystemsLtd (SZSE:301080)

Overview: Acrobiosystems Co., Ltd. develops and manufactures recombinant proteins, antibodies, and other biological reagents for pharmaceutical and biotechnology companies as well as scientific research institutions, with a market cap of CN¥5.24 billion.

Operations: The company generates revenue primarily from Research and Experimental Development, amounting to CN¥583.70 million.

Estimated Discount To Fair Value: 21.9%

Acrobiosystems Ltd. is trading at CN¥46.46, approximately 21.9% below its estimated fair value of CN¥59.51, indicating potential undervaluation based on cash flows. Despite a decline in net income to CNY 83.49 million for the recent nine months, earnings are expected to grow significantly at 30.47% annually over the next three years, surpassing market growth rates. However, profit margins have decreased from last year’s levels and the dividend remains poorly covered by current earnings or free cash flows.

- Our earnings growth report unveils the potential for significant increases in AcrobiosystemsLtd's future results.

- Click to explore a detailed breakdown of our findings in AcrobiosystemsLtd's balance sheet health report.

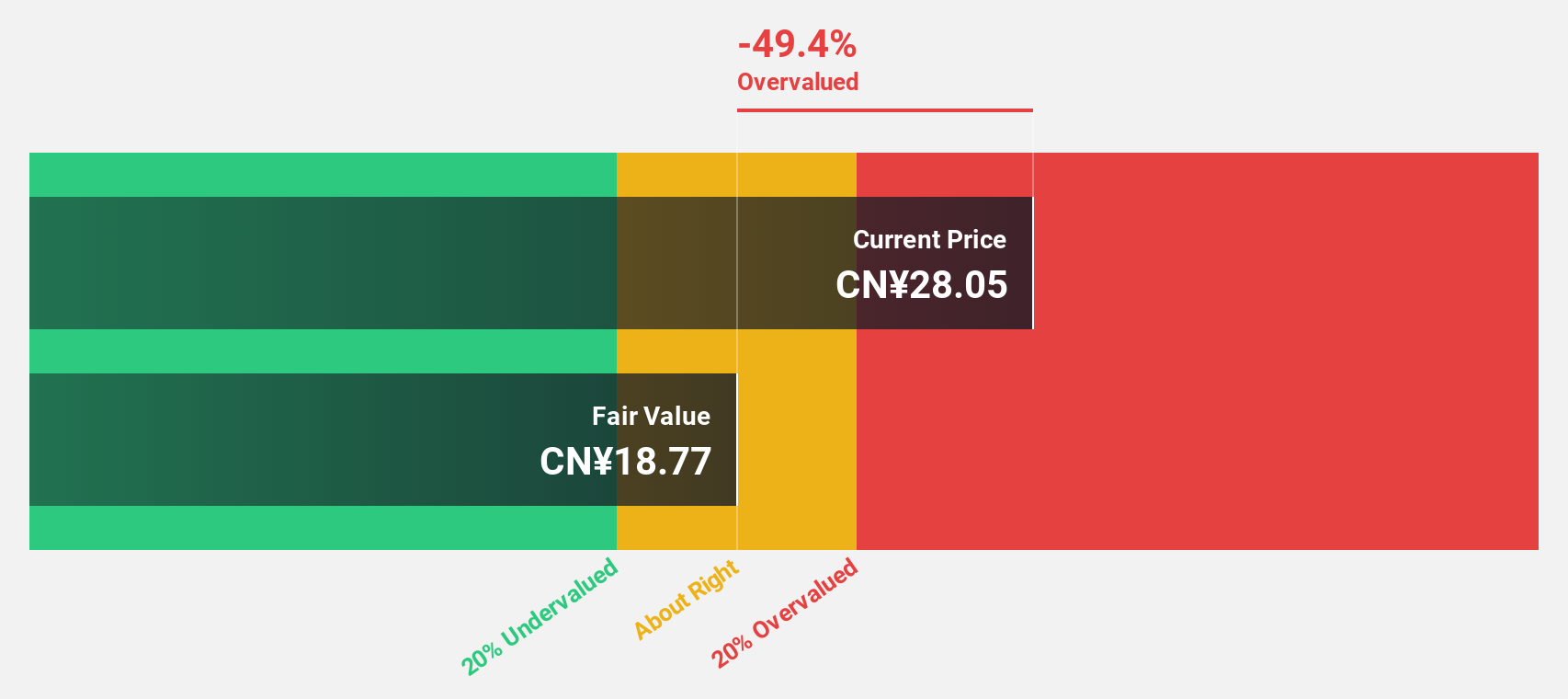

Suzhou Alton Electrical & Mechanical Industry (SZSE:301187)

Overview: Suzhou Alton Electrical & Mechanical Industry Co., Ltd. operates in the electrical and mechanical sector, with a market capitalization of CN¥4.99 billion.

Operations: Suzhou Alton Electrical & Mechanical Industry Co., Ltd. generates its revenue from various segments within the electrical and mechanical sector.

Estimated Discount To Fair Value: 24.2%

Suzhou Alton Electrical & Mechanical Industry is trading at CN¥32.78, over 20% below its estimated fair value of CN¥43.26, highlighting potential undervaluation based on cash flows. Recent earnings for the nine months show revenue growth to CN¥1.31 billion from CN¥836.6 million a year ago, with net income rising to CN¥184.58 million from CN¥124.75 million last year. However, dividends are not well covered by earnings or free cash flows, posing a potential risk.

- Our growth report here indicates Suzhou Alton Electrical & Mechanical Industry may be poised for an improving outlook.

- Unlock comprehensive insights into our analysis of Suzhou Alton Electrical & Mechanical Industry stock in this financial health report.

Summing It All Up

- Investigate our full lineup of 899 Undervalued Stocks Based On Cash Flows right here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:301187

Suzhou Alton Electrical & Mechanical Industry

Suzhou Alton Electrical & Mechanical Industry Co., Ltd.

Exceptional growth potential and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

48 followersusers have followed this narrative

6 commentsusers have commented on this narrative

15 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4729.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.8% undervalued

956 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Alphabet ·

GOOGL: AI Platform Expansion And Cloud Demand Will Support Durable Performance Amid Competitive Pressures

Fair Value:US$323.71.9% undervalued

1342 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative