- China

- /

- Electrical

- /

- SZSE:301152

Subdued Growth No Barrier To Tianli Lithium Energy Group Co., Ltd. (SZSE:301152) With Shares Advancing 32%

Despite an already strong run, Tianli Lithium Energy Group Co., Ltd. (SZSE:301152) shares have been powering on, with a gain of 32% in the last thirty days. Notwithstanding the latest gain, the annual share price return of 9.7% isn't as impressive.

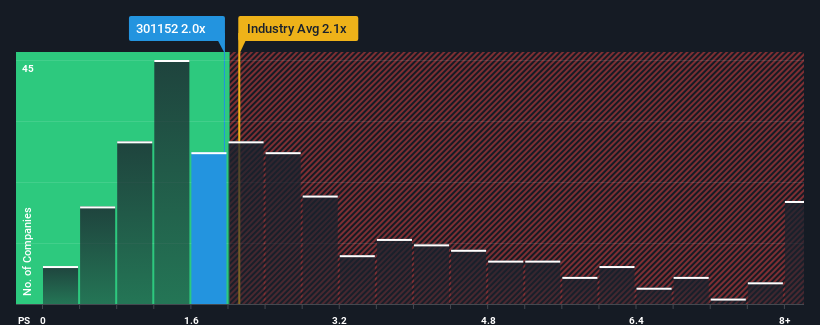

In spite of the firm bounce in price, you could still be forgiven for feeling indifferent about Tianli Lithium Energy Group's P/S ratio of 2x, since the median price-to-sales (or "P/S") ratio for the Electrical industry in China is also close to 2.1x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

View our latest analysis for Tianli Lithium Energy Group

How Tianli Lithium Energy Group Has Been Performing

For instance, Tianli Lithium Energy Group's receding revenue in recent times would have to be some food for thought. Perhaps investors believe the recent revenue performance is enough to keep in line with the industry, which is keeping the P/S from dropping off. If not, then existing shareholders may be a little nervous about the viability of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Tianli Lithium Energy Group will help you shine a light on its historical performance.How Is Tianli Lithium Energy Group's Revenue Growth Trending?

Tianli Lithium Energy Group's P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 17%. However, a few very strong years before that means that it was still able to grow revenue by an impressive 41% in total over the last three years. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been more than adequate for the company.

This is in contrast to the rest of the industry, which is expected to grow by 23% over the next year, materially higher than the company's recent medium-term annualised growth rates.

In light of this, it's curious that Tianli Lithium Energy Group's P/S sits in line with the majority of other companies. Apparently many investors in the company are less bearish than recent times would indicate and aren't willing to let go of their stock right now. Maintaining these prices will be difficult to achieve as a continuation of recent revenue trends is likely to weigh down the shares eventually.

The Final Word

Its shares have lifted substantially and now Tianli Lithium Energy Group's P/S is back within range of the industry median. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Tianli Lithium Energy Group's average P/S is a bit surprising since its recent three-year growth is lower than the wider industry forecast. When we see weak revenue with slower than industry growth, we suspect the share price is at risk of declining, bringing the P/S back in line with expectations. If recent medium-term revenue trends continue, the probability of a share price decline will become quite substantial, placing shareholders at risk.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Tianli Lithium Energy Group you should know about.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Tianli Lithium Energy Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:301152

Tianli Lithium Energy Group

Engages in the research and development, production, and sale of ternary cathode materials for lithium batteries in China.

Mediocre balance sheet low.

Market Insights

Community Narratives