Advertisement

Nanjing Railway New Technology Co.,Ltd.'s (SZSE:301016) 27% Share Price Plunge Could Signal Some Risk

Nanjing Railway New Technology Co.,Ltd. (SZSE:301016) shares have retraced a considerable 27% in the last month, reversing a fair amount of their solid recent performance. To make matters worse, the recent drop has wiped out a year's worth of gains with the share price now back where it started a year ago.

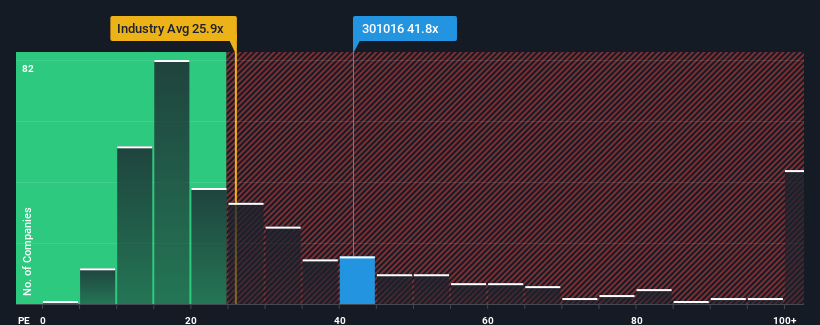

Although its price has dipped substantially, Nanjing Railway New TechnologyLtd may still be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 41.8x, since almost half of all companies in China have P/E ratios under 26x and even P/E's lower than 16x are not unusual. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

Nanjing Railway New TechnologyLtd has been doing a good job lately as it's been growing earnings at a solid pace. One possibility is that the P/E is high because investors think this respectable earnings growth will be enough to outperform the broader market in the near future. If not, then existing shareholders may be a little nervous about the viability of the share price.

See our latest analysis for Nanjing Railway New TechnologyLtd

How Is Nanjing Railway New TechnologyLtd's Growth Trending?

Nanjing Railway New TechnologyLtd's P/E ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the market.

If we review the last year of earnings growth, the company posted a worthy increase of 15%. Ultimately though, it couldn't turn around the poor performance of the prior period, with EPS shrinking 61% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Weighing that medium-term earnings trajectory against the broader market's one-year forecast for expansion of 36% shows it's an unpleasant look.

In light of this, it's alarming that Nanjing Railway New TechnologyLtd's P/E sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. Only the boldest would assume these prices are sustainable as a continuation of recent earnings trends is likely to weigh heavily on the share price eventually.

The Final Word

Nanjing Railway New TechnologyLtd's shares may have retreated, but its P/E is still flying high. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Our examination of Nanjing Railway New TechnologyLtd revealed its shrinking earnings over the medium-term aren't impacting its high P/E anywhere near as much as we would have predicted, given the market is set to grow. When we see earnings heading backwards and underperforming the market forecasts, we suspect the share price is at risk of declining, sending the high P/E lower. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these prices as being reasonable.

It is also worth noting that we have found 3 warning signs for Nanjing Railway New TechnologyLtd (2 can't be ignored!) that you need to take into consideration.

If these risks are making you reconsider your opinion on Nanjing Railway New TechnologyLtd, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Nanjing Railway New TechnologyLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:301016

Nanjing Railway New TechnologyLtd

Engages in the research, development, and manufacturing of rail vehicle body parts and bogie parts in China and internationally.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|48.2% undervalued

TO

Community Contributor