Advertisement

- China

- /

- Construction

- /

- SZSE:300977

Why We're Not Concerned About Shenzhen Ridge Engineering Consulting Co., Ltd.'s (SZSE:300977) Share Price

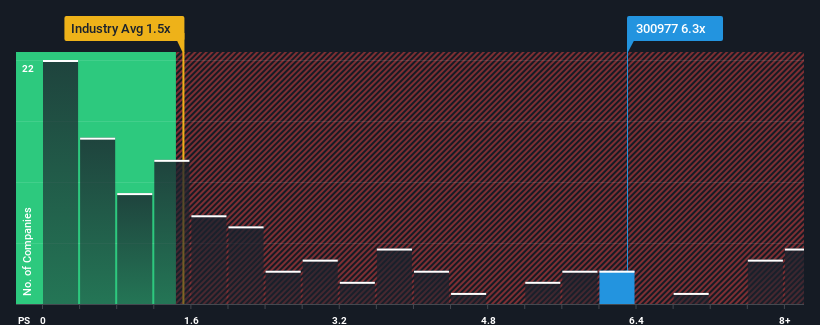

When you see that almost half of the companies in the Construction industry in China have price-to-sales ratios (or "P/S") below 1.5x, Shenzhen Ridge Engineering Consulting Co., Ltd. (SZSE:300977) looks to be giving off strong sell signals with its 6.3x P/S ratio. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for Shenzhen Ridge Engineering Consulting

How Has Shenzhen Ridge Engineering Consulting Performed Recently?

The recently shrinking revenue for Shenzhen Ridge Engineering Consulting has been in line with the industry. Perhaps the market is expecting the company to reverse its fortunes and beat out a struggling industry in the future, elevating the P/S. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Shenzhen Ridge Engineering Consulting.Is There Enough Revenue Growth Forecasted For Shenzhen Ridge Engineering Consulting?

Shenzhen Ridge Engineering Consulting's P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 4.1%. This means it has also seen a slide in revenue over the longer-term as revenue is down 35% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Shifting to the future, estimates from the dual analysts covering the company suggest revenue should grow by 21% over the next year. With the industry only predicted to deliver 12%, the company is positioned for a stronger revenue result.

In light of this, it's understandable that Shenzhen Ridge Engineering Consulting's P/S sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On Shenzhen Ridge Engineering Consulting's P/S

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Shenzhen Ridge Engineering Consulting maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Construction industry, as expected. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. Unless these conditions change, they will continue to provide strong support to the share price.

You need to take note of risks, for example - Shenzhen Ridge Engineering Consulting has 3 warning signs (and 1 which is a bit concerning) we think you should know about.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300977

Shenzhen Ridge Engineering Consulting

Shenzhen Ridge Engineering Consulting Co., Ltd.

High growth potential with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor