- China

- /

- Electrical

- /

- SZSE:300709

Take Care Before Jumping Onto Jiangsu Gian Technology Co., Ltd. (SZSE:300709) Even Though It's 30% Cheaper

Jiangsu Gian Technology Co., Ltd. (SZSE:300709) shares have had a horrible month, losing 30% after a relatively good period beforehand. The recent drop has obliterated the annual return, with the share price now down 6.3% over that longer period.

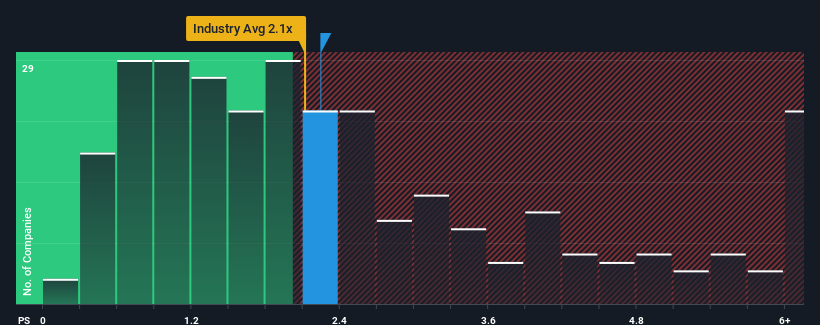

Although its price has dipped substantially, there still wouldn't be many who think Jiangsu Gian Technology's price-to-sales (or "P/S") ratio of 2.2x is worth a mention when the median P/S in China's Electrical industry is similar at about 2.1x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

See our latest analysis for Jiangsu Gian Technology

How Jiangsu Gian Technology Has Been Performing

Jiangsu Gian Technology could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. One possibility is that the P/S ratio is moderate because investors think this poor revenue performance will turn around. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

Keen to find out how analysts think Jiangsu Gian Technology's future stacks up against the industry? In that case, our free report is a great place to start.Do Revenue Forecasts Match The P/S Ratio?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Jiangsu Gian Technology's to be considered reasonable.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 19%. Even so, admirably revenue has lifted 39% in aggregate from three years ago, notwithstanding the last 12 months. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been more than adequate for the company.

Turning to the outlook, the next year should generate growth of 40% as estimated by the sole analyst watching the company. That's shaping up to be materially higher than the 23% growth forecast for the broader industry.

With this information, we find it interesting that Jiangsu Gian Technology is trading at a fairly similar P/S compared to the industry. It may be that most investors aren't convinced the company can achieve future growth expectations.

What We Can Learn From Jiangsu Gian Technology's P/S?

Following Jiangsu Gian Technology's share price tumble, its P/S is just clinging on to the industry median P/S. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Looking at Jiangsu Gian Technology's analyst forecasts revealed that its superior revenue outlook isn't giving the boost to its P/S that we would've expected. When we see a strong revenue outlook, with growth outpacing the industry, we can only assume potential uncertainty around these figures are what might be placing slight pressure on the P/S ratio. However, if you agree with the analysts' forecasts, you may be able to pick up the stock at an attractive price.

You always need to take note of risks, for example - Jiangsu Gian Technology has 1 warning sign we think you should be aware of.

If these risks are making you reconsider your opinion on Jiangsu Gian Technology, explore our interactive list of high quality stocks to get an idea of what else is out there.

If you're looking to trade Jiangsu Gian Technology, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300709

Jiangsu Gian Technology

Manufactures and sells metal injection molding products in China and internationally.

High growth potential with excellent balance sheet.

Market Insights

Community Narratives