Advertisement

- China

- /

- Semiconductors

- /

- SHSE:688599

Asian Growth Companies With High Insider Ownership October 2025

Simply Wall St

Reviewed by Simply Wall St

In the current economic climate, Asian markets are navigating a landscape marked by cautious optimism, with growth prospects tempered by global inflationary pressures and evolving monetary policies. Amidst these conditions, companies in Asia that exhibit high insider ownership often signal strong confidence from those who know the business best, making them intriguing considerations for investors seeking growth opportunities.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Zhejiang Leapmotor Technology (SEHK:9863) | 14.6% | 57.6% |

| Vuno (KOSDAQ:A338220) | 15.6% | 113.4% |

| Seers Technology (KOSDAQ:A458870) | 33.9% | 84.6% |

| Novoray (SHSE:688300) | 23.6% | 30.3% |

| Laopu Gold (SEHK:6181) | 35.5% | 34% |

| J&V Energy Technology (TWSE:6869) | 17.5% | 24.9% |

| Gold Circuit Electronics (TWSE:2368) | 31.4% | 35.2% |

| Fulin Precision (SZSE:300432) | 11.7% | 50.7% |

| Ascentage Pharma Group International (SEHK:6855) | 12.8% | 91.9% |

| AprilBioLtd (KOSDAQ:A397030) | 31% | 87.1% |

Let's review some notable picks from our screened stocks.

Trina Solar (SHSE:688599)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Trina Solar Co., Ltd. is involved in the research, development, production, and sales of photovoltaic modules across various global regions including China, Europe, North America, and others with a market cap of CN¥37.59 billion.

Operations: Trina Solar generates revenue through the development, manufacturing, and distribution of photovoltaic modules across regions such as China, Europe, North America, Japan, the Asia Pacific, the Middle East, and Africa.

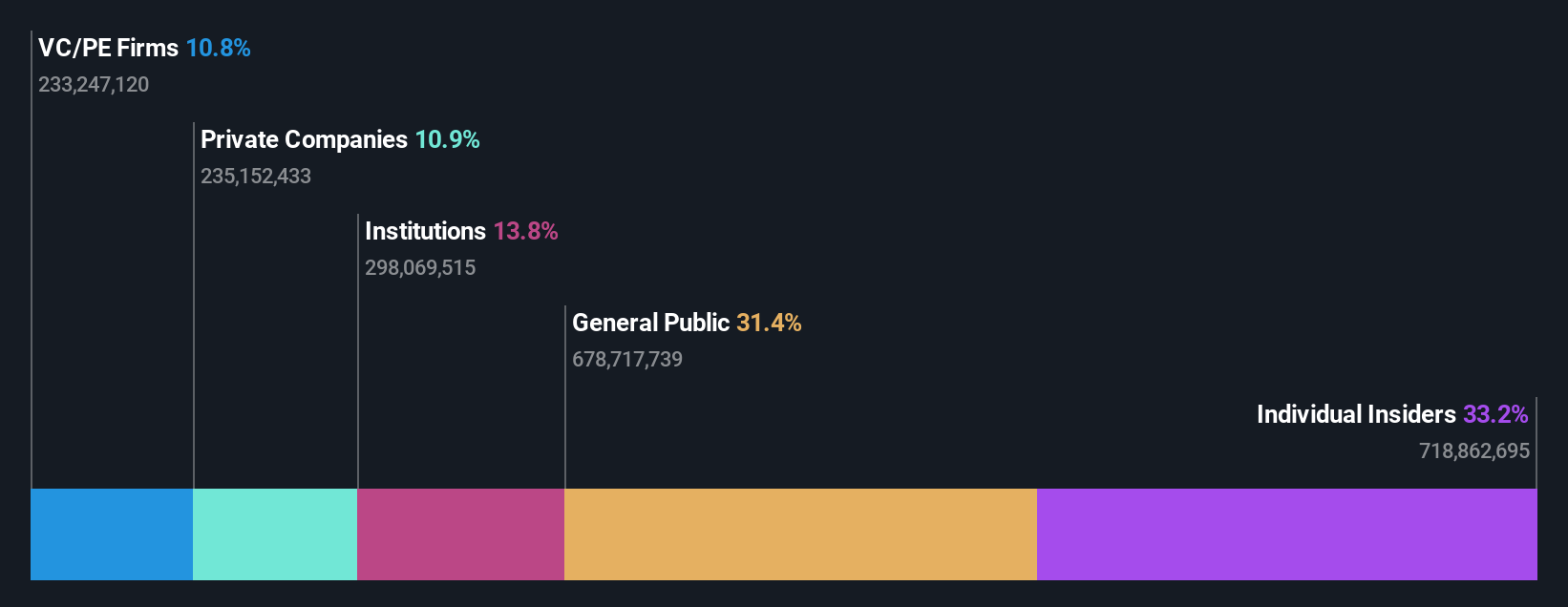

Insider Ownership: 33.2%

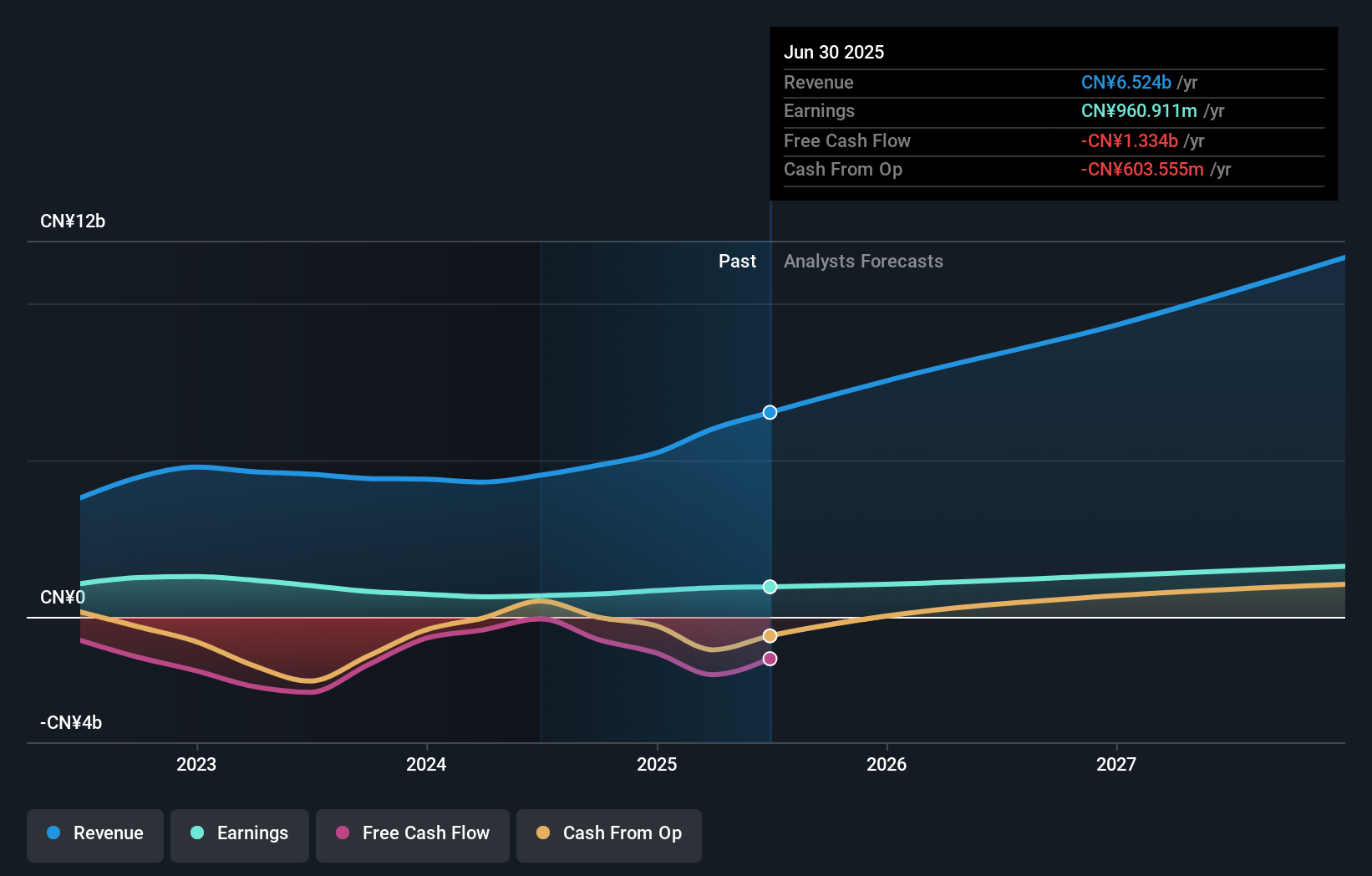

Trina Solar is positioned as a growth company with high insider ownership, though it faces challenges. The company's forecasted earnings growth of 71.51% per year indicates strong future potential despite a recent net loss of CNY 2.92 billion for H1 2025. Trina's innovative energy storage solutions, such as the Elementa 2 Pro Platform, and its high-efficiency Vertex modules underscore its commitment to advancing solar technology and maintaining competitive market positioning in Asia's renewable energy sector.

- Click here to discover the nuances of Trina Solar with our detailed analytical future growth report.

- According our valuation report, there's an indication that Trina Solar's share price might be on the cheaper side.

Shijiazhuang Shangtai Technology (SZSE:001301)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Shijiazhuang Shangtai Technology Co., Ltd. operates in the technology sector and has a market cap of approximately CN¥21.83 billion.

Operations: The company's revenue is primarily derived from Negative Electrode Material at CN¥5.97 billion, followed by Graphitized Coke at CN¥304.23 million and Diamond Carbon Source at CN¥27.34 million.

Insider Ownership: 39.4%

Shijiazhuang Shangtai Technology demonstrates potential as a growth company, with earnings forecasted to grow 21.37% annually despite a highly volatile share price. The company's recent half-year results showed significant revenue growth to CNY 3.39 billion from CNY 2.09 billion year-on-year. However, its return on equity is expected to be low at 16.7%, and its dividend yield of 0.96% is not well covered by free cash flows, indicating some financial constraints amid positive revenue trends.

- Click here and access our complete growth analysis report to understand the dynamics of Shijiazhuang Shangtai Technology.

- Upon reviewing our latest valuation report, Shijiazhuang Shangtai Technology's share price might be too pessimistic.

Guangzhou Great Power Energy and Technology (SZSE:300438)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Guangzhou Great Power Energy and Technology Co., Ltd focuses on the research, development, production, and sale of energy batteries in China with a market cap of CN¥20.54 billion.

Operations: The company generates revenue primarily from its electronic component manufacturing segment, totaling CN¥8.49 billion.

Insider Ownership: 34.4%

Guangzhou Great Power Energy and Technology shows promise with forecasted revenue growth of 18.5% annually, outpacing the CN market average. Despite a recent net loss of CNY 88.23 million for the half year ending June 2025, it is expected to become profitable within three years, indicating strong future potential. However, its return on equity is projected to remain low at 8.3%, and current debt levels are not well covered by operating cash flow, posing financial challenges.

- Take a closer look at Guangzhou Great Power Energy and Technology's potential here in our earnings growth report.

- Our valuation report unveils the possibility Guangzhou Great Power Energy and Technology's shares may be trading at a premium.

Summing It All Up

- Investigate our full lineup of 615 Fast Growing Asian Companies With High Insider Ownership right here.

- Ready To Venture Into Other Investment Styles? AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Trina Solar might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688599

Trina Solar

Engages in the research and development, production, and sales of photovoltaic (PV) modules in China, Europe, North America, the United States, Japan, the Asia Pacific, the Middle East, and Africa.

Reasonable growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.2% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|90.0% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.6% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|97.1% undervalued

AG

Community Contributor