Nanfang Zhongjin Environment Co., Ltd. (SZSE:300145) Held Back By Insufficient Growth Even After Shares Climb 31%

Nanfang Zhongjin Environment Co., Ltd. (SZSE:300145) shareholders are no doubt pleased to see that the share price has bounced 31% in the last month, although it is still struggling to make up recently lost ground. Notwithstanding the latest gain, the annual share price return of 2.9% isn't as impressive.

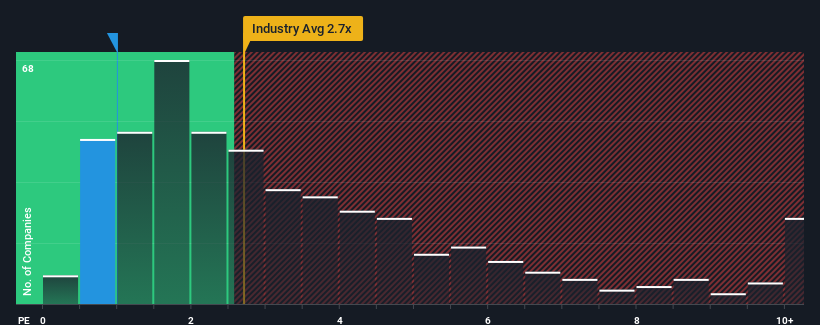

In spite of the firm bounce in price, Nanfang Zhongjin Environment may still be sending buy signals at present with its price-to-sales (or "P/S") ratio of 1x, considering almost half of all companies in the Machinery industry in China have P/S ratios greater than 2.7x and even P/S higher than 5x aren't out of the ordinary. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

See our latest analysis for Nanfang Zhongjin Environment

What Does Nanfang Zhongjin Environment's P/S Mean For Shareholders?

Recent times haven't been great for Nanfang Zhongjin Environment as its revenue has been rising slower than most other companies. It seems that many are expecting the uninspiring revenue performance to persist, which has repressed the growth of the P/S ratio. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Nanfang Zhongjin Environment.Is There Any Revenue Growth Forecasted For Nanfang Zhongjin Environment?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Nanfang Zhongjin Environment's to be considered reasonable.

Taking a look back first, we see that the company managed to grow revenues by a handy 6.5% last year. This was backed up an excellent period prior to see revenue up by 39% in total over the last three years. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 14% during the coming year according to the two analysts following the company. Meanwhile, the rest of the industry is forecast to expand by 27%, which is noticeably more attractive.

With this information, we can see why Nanfang Zhongjin Environment is trading at a P/S lower than the industry. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Bottom Line On Nanfang Zhongjin Environment's P/S

The latest share price surge wasn't enough to lift Nanfang Zhongjin Environment's P/S close to the industry median. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Nanfang Zhongjin Environment maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. Shareholders' pessimism on the revenue prospects for the company seems to be the main contributor to the depressed P/S. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Nanfang Zhongjin Environment (1 is potentially serious!) that you need to be mindful of.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

If you're looking to trade Nanfang Zhongjin Environment, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Nanfang Zhongjin Environment might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300145

Nanfang Zhongjin Environment

Through its subsidiaries, engages in the general equipment manufacturing business.

Flawless balance sheet and fair value.

Market Insights

Community Narratives