3 Growth Companies With High Insider Ownership And Up To 38% Revenue Growth

Reviewed by Simply Wall St

As global markets navigate through geopolitical tensions and economic fluctuations, investors are keenly observing sectors that can withstand such volatility. In this environment, growth companies with high insider ownership stand out as potentially resilient options, offering a unique alignment of interests between management and shareholders.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 11.9% | 21.1% |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 34% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 27.4% |

| Atlas Energy Solutions (NYSE:AESI) | 29.1% | 42.1% |

| People & Technology (KOSDAQ:A137400) | 16.4% | 35.6% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.8% | 49.1% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 14.0% | 95% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 100.3% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.4% |

| UTI (KOSDAQ:A179900) | 33.1% | 134.6% |

Here's a peek at a few of the choices from the screener.

DBAPPSecurity (SHSE:688023)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: DBAPPSecurity Co., Ltd. operates in China, focusing on the research, development, manufacture, and sale of cybersecurity products with a market cap of CN¥5.65 billion.

Operations: DBAPPSecurity Co., Ltd. generates revenue through its research, development, manufacture, and sale of cybersecurity products in China.

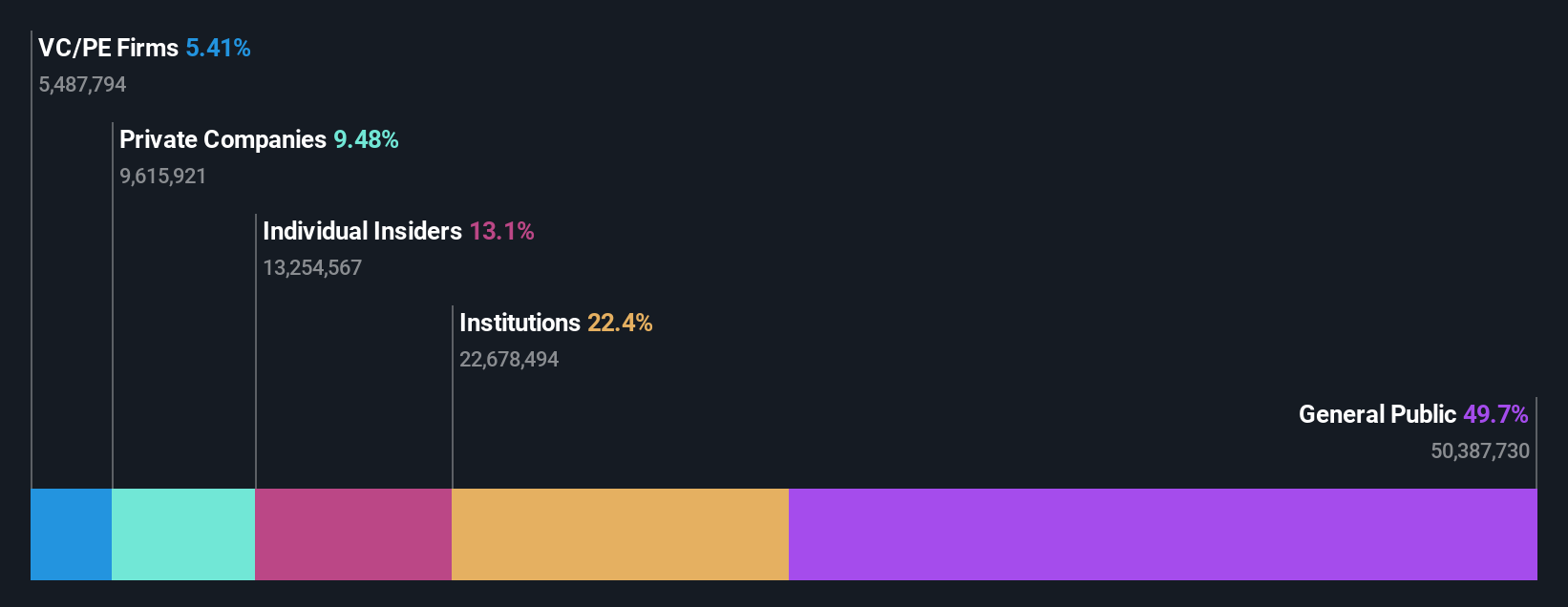

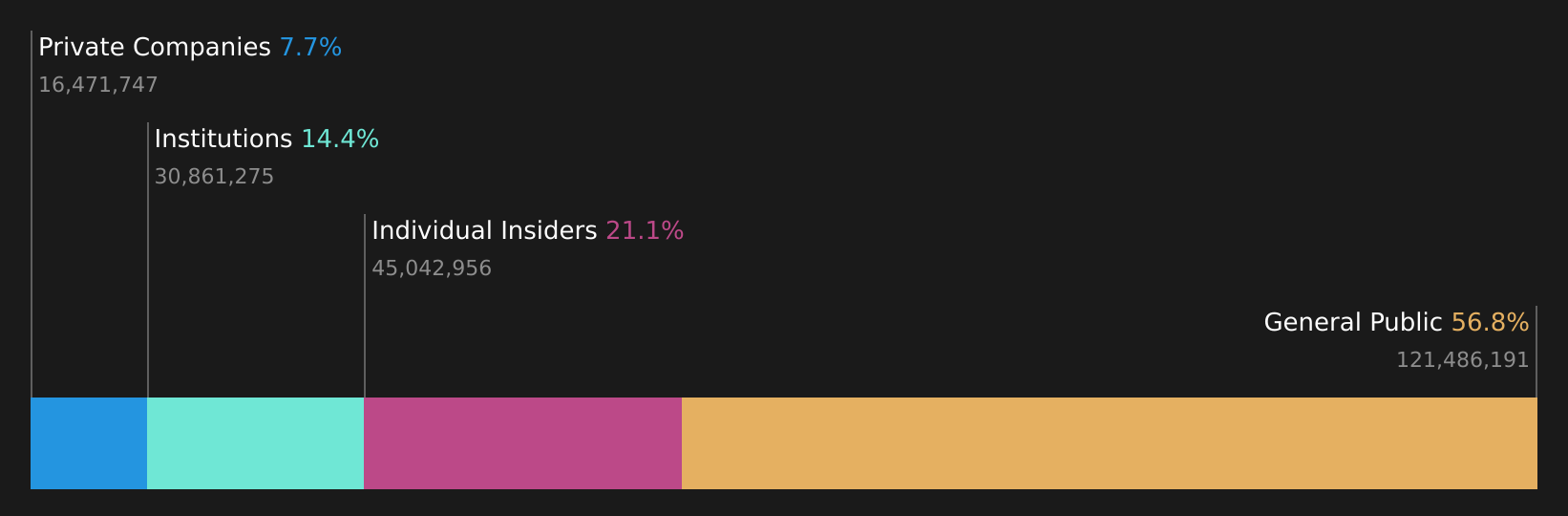

Insider Ownership: 16.9%

Revenue Growth Forecast: 17.3% p.a.

DBAPPSecurity is expected to achieve profitability within three years, with earnings forecasted to grow at 73.64% annually, surpassing market averages. Despite trading at 57.4% below estimated fair value and showing good relative value compared to peers, the share price has been highly volatile recently. Revenue growth is projected at 17.3% per year, outpacing the Chinese market average of 13.4%. Recent reports show a reduced net loss of CNY 275.61 million for H1 2024 compared to last year.

- Navigate through the intricacies of DBAPPSecurity with our comprehensive analyst estimates report here.

- The valuation report we've compiled suggests that DBAPPSecurity's current price could be quite moderate.

Great Microwave Technology (SHSE:688270)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Great Microwave Technology Co., Ltd. focuses on the research, development, production, and sale of integrated circuit chips and microsystems in China, with a market cap of CN¥6.95 billion.

Operations: Great Microwave Technology Co., Ltd. generates revenue through its activities in research, development, production, and sale of integrated circuit chips and microsystems within China.

Insider Ownership: 21%

Revenue Growth Forecast: 38.9% p.a.

Great Microwave Technology's earnings are projected to grow significantly at 61.1% annually, outpacing the Chinese market average. Revenue is expected to rise by 38.9% per year, well above the market rate. However, recent earnings showed a decline in net income from CNY 33.53 million to CNY 5.63 million for H1 2024, and profit margins have decreased from last year’s figures. Despite high growth forecasts, insider trading activity remains minimal over recent months.

- Unlock comprehensive insights into our analysis of Great Microwave Technology stock in this growth report.

- According our valuation report, there's an indication that Great Microwave Technology's share price might be on the expensive side.

Shenzhen Zhaowei Machinery & Electronics (SZSE:003021)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shenzhen Zhaowei Machinery & Electronics Co., Ltd. operates in the machinery and electronics sector, with a market cap of CN¥11.82 billion.

Operations: The company's revenue segments comprise Micro Transmission System at CN¥833.68 million, Precision Injection Molded Parts at CN¥428.05 million, and Precision Molds and Other Products at CN¥85.73 million.

Insider Ownership: 18.2%

Revenue Growth Forecast: 25.7% p.a.

Shenzhen Zhaowei Machinery & Electronics is experiencing robust growth, with revenue for the first half of 2024 rising to CNY 645.11 million from CNY 503.6 million a year ago, and net income increasing to CNY 93.83 million. Forecasts indicate revenue growth of 25.7% annually, surpassing the market average, while earnings are expected to grow by 28.5%. Despite these prospects, insider trading activity has been minimal recently and return on equity is forecasted low at 9.8%.

- Click to explore a detailed breakdown of our findings in Shenzhen Zhaowei Machinery & Electronics' earnings growth report.

- The analysis detailed in our Shenzhen Zhaowei Machinery & Electronics valuation report hints at an inflated share price compared to its estimated value.

Turning Ideas Into Actions

- Unlock our comprehensive list of 1477 Fast Growing Companies With High Insider Ownership by clicking here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688023

DBAPPSecurity

Engages in the research and development, manufacture, and sale of cybersecurity products in China.

Undervalued with reasonable growth potential.