Advertisement

As global markets navigate a mixed start to 2025, with the S&P 500 and Nasdaq Composite reflecting strong annual gains despite recent volatility, investors are keenly observing economic indicators like the Chicago PMI and GDP forecasts that hint at underlying challenges for small-cap companies. Amidst this backdrop, identifying promising stocks requires a focus on those with robust fundamentals and potential resilience in fluctuating market conditions.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Morris State Bancshares | 10.20% | -0.28% | 6.97% | ★★★★★★ |

| Cita Mineral Investindo | NA | -3.08% | 16.56% | ★★★★★★ |

| Bahrain National Holding Company B.S.C | NA | 20.11% | 5.44% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Indofood Agri Resources | 34.58% | 4.29% | 50.61% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Mamata Machinery | 8.30% | 14.61% | 34.29% | ★★★★★☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Renaissance Global | 47.81% | -2.99% | 0.28% | ★★★★☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

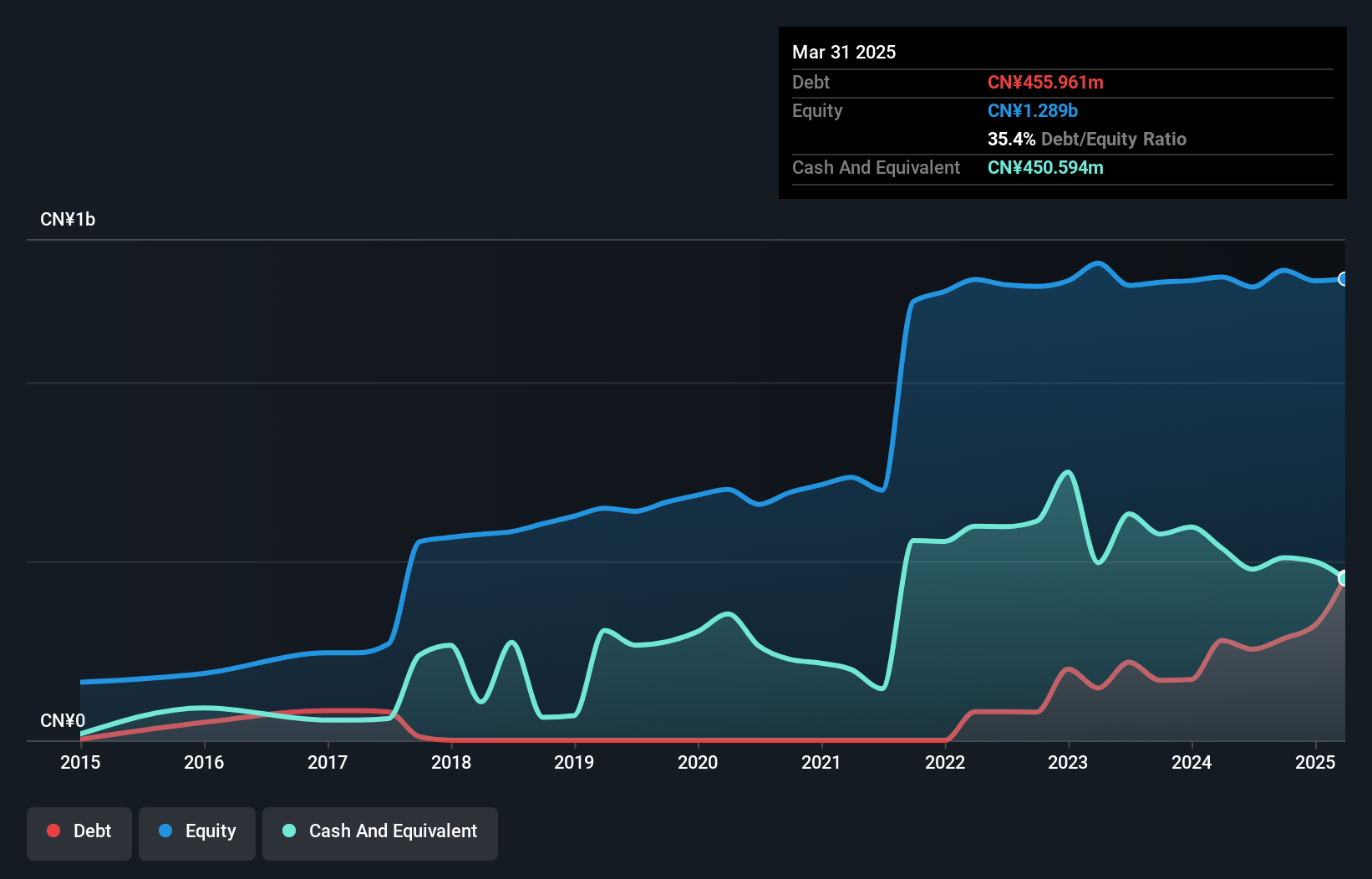

Keli Motor Group (SZSE:002892)

Simply Wall St Value Rating: ★★★★★☆

Overview: Keli Motor Group Co., Ltd. focuses on the research and development, manufacture, and sale of micro motors in China with a market capitalization of CN¥9.54 billion.

Operations: The primary revenue streams for Keli Motor Group are derived from the sale of micro motors. The company has experienced fluctuations in its gross profit margin, which was last reported at 28.5%.

Keli Motor Group, a smaller player in the automotive sector, reported impressive earnings growth of 28.5% over the past year, outpacing the electrical industry’s modest 1.1%. Despite this recent surge, its earnings have slipped by an average of 12.2% annually over five years. The company boasts more cash than total debt, yet its debt-to-equity ratio climbed to 21.7%. A significant one-off gain of CN¥18.9 million influenced recent results up to September 2024, while interest payments are comfortably covered with EBIT at 4.4 times coverage. Recent revenue reached CNY1.22 billion from CNY968 million previously, reflecting robust sales momentum.

- Click here and access our complete health analysis report to understand the dynamics of Keli Motor Group.

Understand Keli Motor Group's track record by examining our Past report.

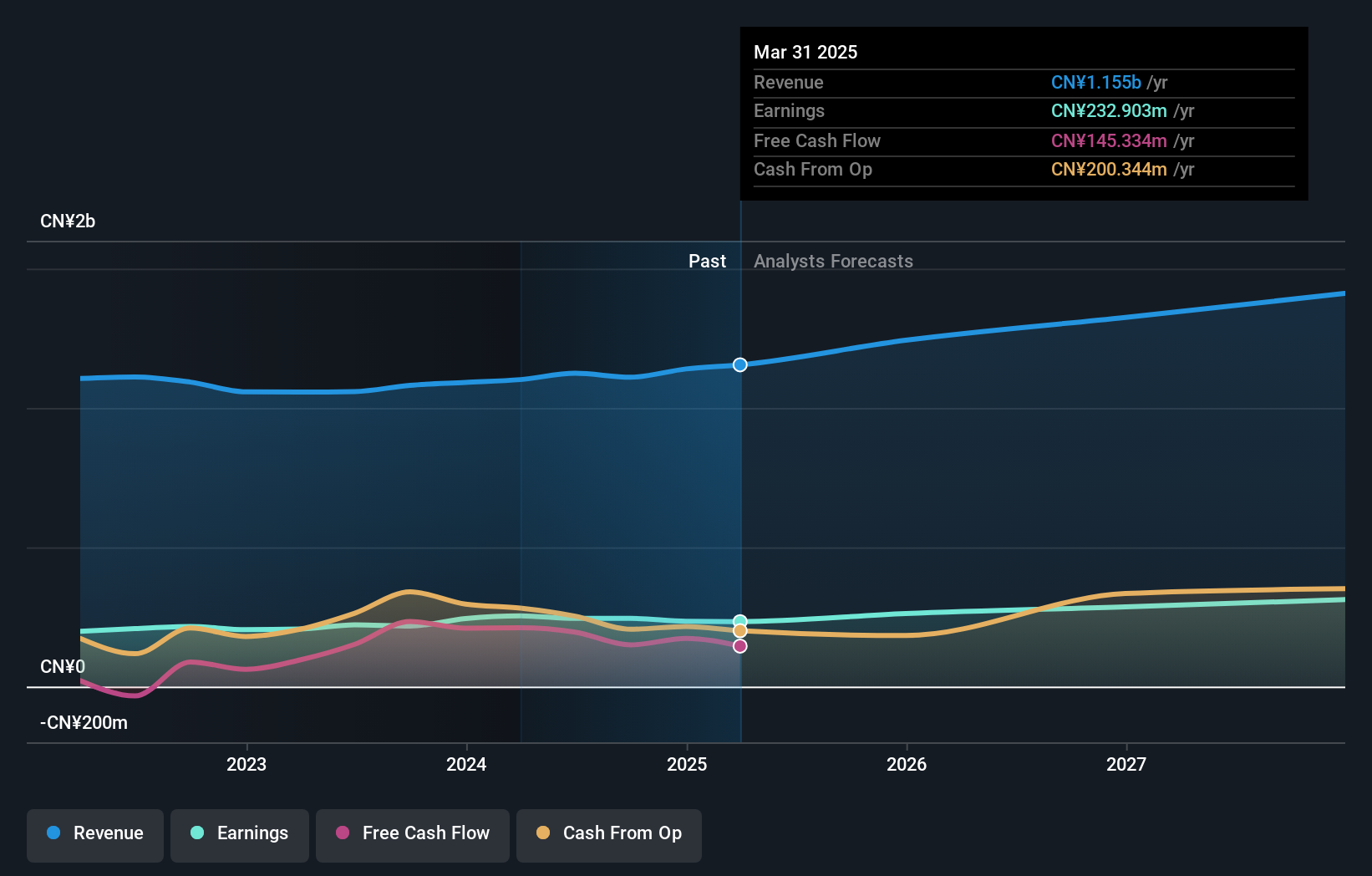

Hanyu Group (SZSE:300403)

Simply Wall St Value Rating: ★★★★★★

Overview: Hanyu Group Joint-Stock Co., Ltd. focuses on the research, development, production, and sale of drainage pumps for household appliances in China, with a market cap of CN¥5.99 billion.

Operations: Hanyu Group generates revenue primarily from the sale of drainage pumps for household appliances in China. The company has a market capitalization of CN¥5.99 billion.

Hanyu Group, a compact player in the machinery sector, has been showing promising signs with its earnings growth of 12.6% over the past year, outpacing the industry average of -0.06%. The company seems to be managing its finances well, evidenced by a reduction in debt-to-equity ratio from 5% to 3% over five years and having more cash than total debt. Despite recent share price volatility, Hanyu's P/E ratio at 25.4x is appealing compared to the CN market's 33.6x. Recent earnings reports indicate steady performance with net income rising slightly to CNY 178 million from CNY 177 million last year.

- Get an in-depth perspective on Hanyu Group's performance by reading our health report here.

Review our historical performance report to gain insights into Hanyu Group's's past performance.

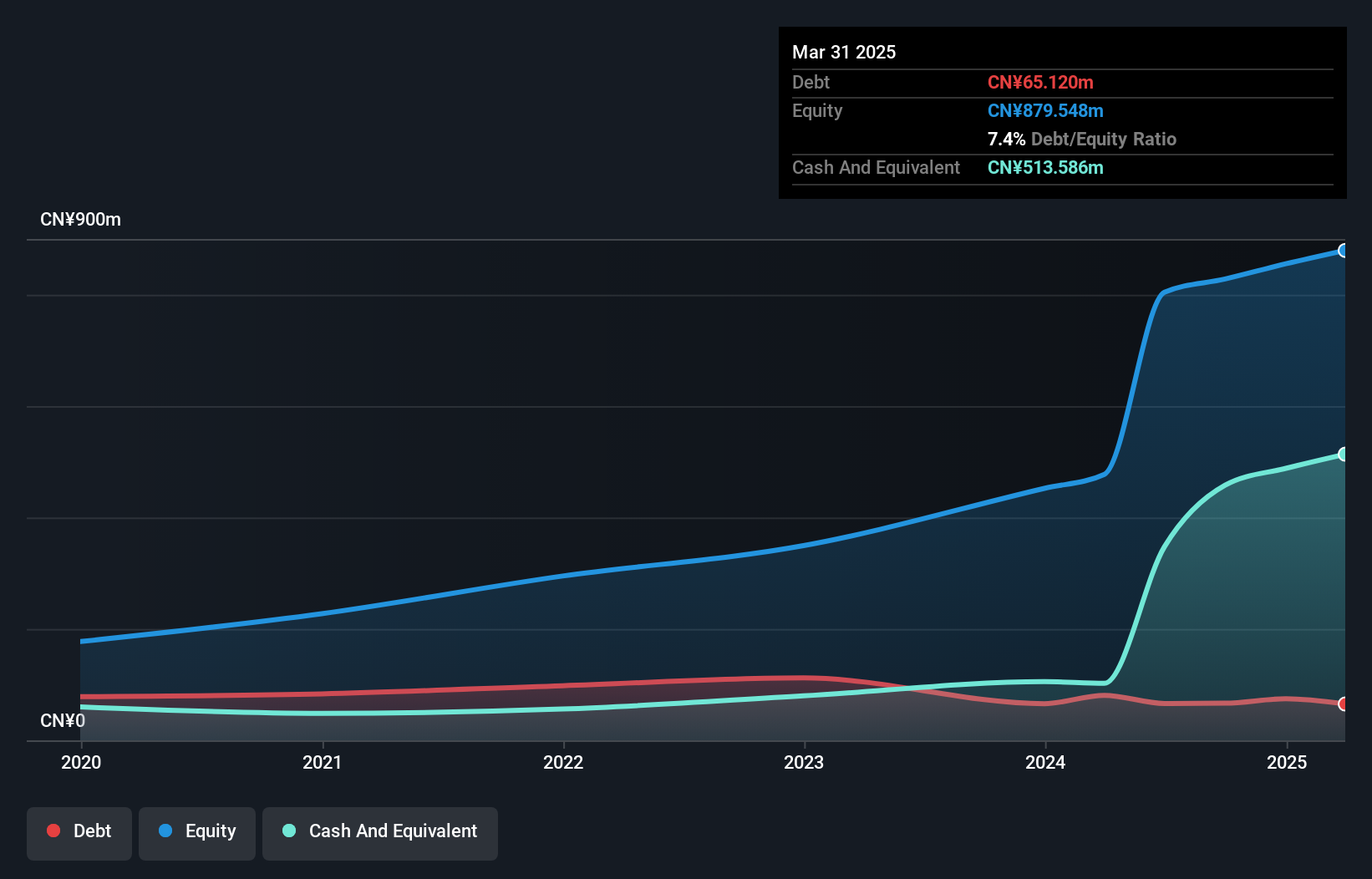

Reach Machinery (SZSE:301596)

Simply Wall St Value Rating: ★★★★★☆

Overview: Reach Machinery Co., Ltd. is involved in the research, development, production, and sale of components for automation equipment, power transmission, and braking systems both domestically in China and internationally, with a market cap of CN¥5.31 billion.

Operations: Reach Machinery generates revenue primarily from its Machinery & Industrial Equipment segment, amounting to CN¥599.22 million.

Reach Machinery, a compact player in the machinery sector, has shown commendable earnings growth of 9.3% over the past year, outpacing its industry peers who saw a slight contraction. The company's financial health seems robust with interest payments comfortably covered by EBIT at 533 times, indicating strong operational efficiency. Despite volatility in share prices recently, Reach's net income for the first nine months of 2024 rose to CNY 73 million from CNY 70 million last year. However, basic earnings per share dipped slightly to CNY 1.55 from CNY 1.70 previously, suggesting some pressure on profitability margins amidst sales growth reaching CNY 443 million this period compared to last year's CNY 429 million.

Summing It All Up

- Reveal the 4651 hidden gems among our Undiscovered Gems With Strong Fundamentals screener with a single click here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hanyu Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300403

Hanyu Group

Researches, develops, produces, and sells drainage pumps for household appliances in China.

Flawless balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% undervalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|45.0% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|20.4% undervalued

TI

Community Contributor