There's Reason For Concern Over Wuxi Smart Auto-Control Engineering Co., Ltd.'s (SZSE:002877) Massive 26% Price Jump

Despite an already strong run, Wuxi Smart Auto-Control Engineering Co., Ltd. (SZSE:002877) shares have been powering on, with a gain of 26% in the last thirty days. The bad news is that even after the stocks recovery in the last 30 days, shareholders are still underwater by about 4.2% over the last year.

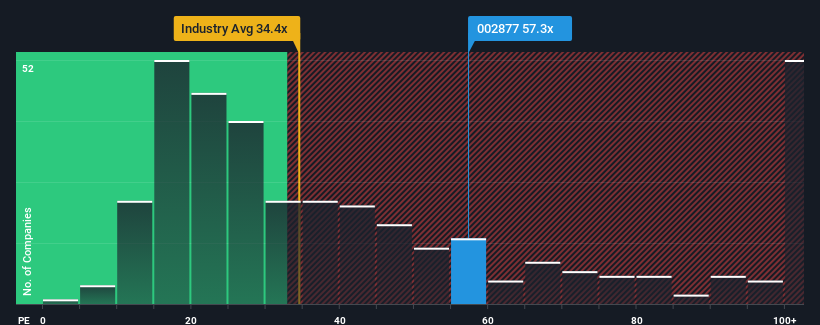

Following the firm bounce in price, Wuxi Smart Auto-Control Engineering's price-to-earnings (or "P/E") ratio of 57.3x might make it look like a strong sell right now compared to the market in China, where around half of the companies have P/E ratios below 34x and even P/E's below 20x are quite common. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

For instance, Wuxi Smart Auto-Control Engineering's receding earnings in recent times would have to be some food for thought. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for Wuxi Smart Auto-Control Engineering

What Are Growth Metrics Telling Us About The High P/E?

The only time you'd be truly comfortable seeing a P/E as steep as Wuxi Smart Auto-Control Engineering's is when the company's growth is on track to outshine the market decidedly.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 49%. This means it has also seen a slide in earnings over the longer-term as EPS is down 7.5% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Weighing that medium-term earnings trajectory against the broader market's one-year forecast for expansion of 39% shows it's an unpleasant look.

In light of this, it's alarming that Wuxi Smart Auto-Control Engineering's P/E sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. Only the boldest would assume these prices are sustainable as a continuation of recent earnings trends is likely to weigh heavily on the share price eventually.

The Key Takeaway

The strong share price surge has got Wuxi Smart Auto-Control Engineering's P/E rushing to great heights as well. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Our examination of Wuxi Smart Auto-Control Engineering revealed its shrinking earnings over the medium-term aren't impacting its high P/E anywhere near as much as we would have predicted, given the market is set to grow. Right now we are increasingly uncomfortable with the high P/E as this earnings performance is highly unlikely to support such positive sentiment for long. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these prices as being reasonable.

Having said that, be aware Wuxi Smart Auto-Control Engineering is showing 2 warning signs in our investment analysis, and 1 of those shouldn't be ignored.

If you're unsure about the strength of Wuxi Smart Auto-Control Engineering's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Wuxi Smart Auto-Control Engineering might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002877

Wuxi Smart Auto-Control Engineering

Wuxi Smart Auto-Control Engineering Co., Ltd.

Mediocre balance sheet with questionable track record.

Market Insights

Community Narratives