Advertisement

- China

- /

- Electrical

- /

- SZSE:002851

Asian Growth Companies With High Insider Ownership For December 2025

Simply Wall St

Reviewed by Simply Wall St

As December 2025 unfolds, Asian markets are capturing global attention with their robust performance, particularly as investors anticipate potential interest rate adjustments from major economies like the U.S. and Japan. Amidst this backdrop, growth companies with high insider ownership in Asia stand out as potentially attractive opportunities, offering a unique blend of strategic alignment and long-term commitment that can be appealing to investors navigating today's complex market environment.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| UTI (KOSDAQ:A179900) | 25.2% | 120.7% |

| Streamax Technology (SZSE:002970) | 32.5% | 33.1% |

| Seers Technology (KOSDAQ:A458870) | 33.9% | 78.8% |

| Novoray (SHSE:688300) | 23.6% | 31.4% |

| Loadstar Capital K.K (TSE:3482) | 31% | 23.6% |

| Laopu Gold (SEHK:6181) | 34.8% | 34.3% |

| Knowmerce (KOSDAQ:A473980) | 30% | 33.2% |

| J&V Energy Technology (TWSE:6869) | 17.5% | 31.6% |

| Gold Circuit Electronics (TWSE:2368) | 31.4% | 37.2% |

| Fulin Precision (SZSE:300432) | 11.6% | 55.2% |

Let's uncover some gems from our specialized screener.

Xi'an Bright Laser TechnologiesLtd (SHSE:688333)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Xi'an Bright Laser Technologies Co., Ltd. offers metal additive manufacturing solutions in China and has a market cap of CN¥22.63 billion.

Operations: Xi'an Bright Laser Technologies Co., Ltd.'s revenue is primarily derived from providing metal additive manufacturing solutions in China.

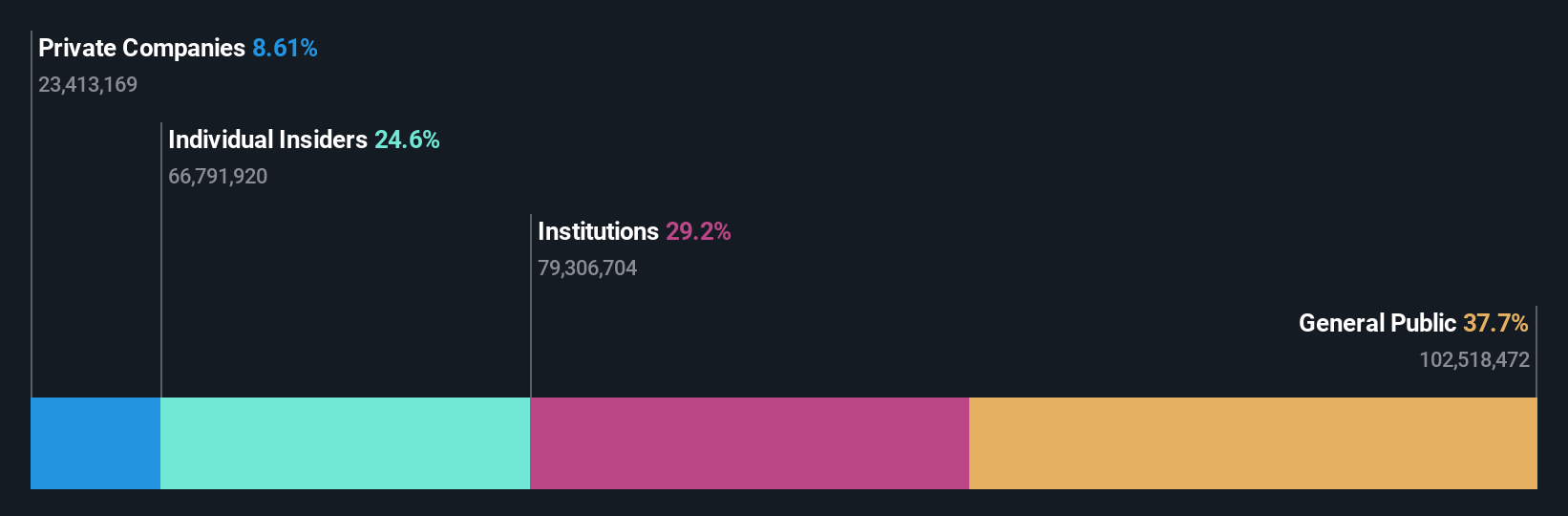

Insider Ownership: 24.6%

Revenue Growth Forecast: 33.2% p.a.

Xi'an Bright Laser Technologies has demonstrated robust growth with its earnings rising by 80.6% over the past year and forecasted to grow at 41.49% annually, outpacing the Chinese market. Revenue is also expected to increase significantly at 33.2% per year. Recent earnings reports show substantial improvements, with net income reaching CNY 155.75 million for the first nine months of 2025, indicating strong operational performance despite a forecast of low future return on equity at 8.7%.

- Dive into the specifics of Xi'an Bright Laser TechnologiesLtd here with our thorough growth forecast report.

- Our expertly prepared valuation report Xi'an Bright Laser TechnologiesLtd implies its share price may be too high.

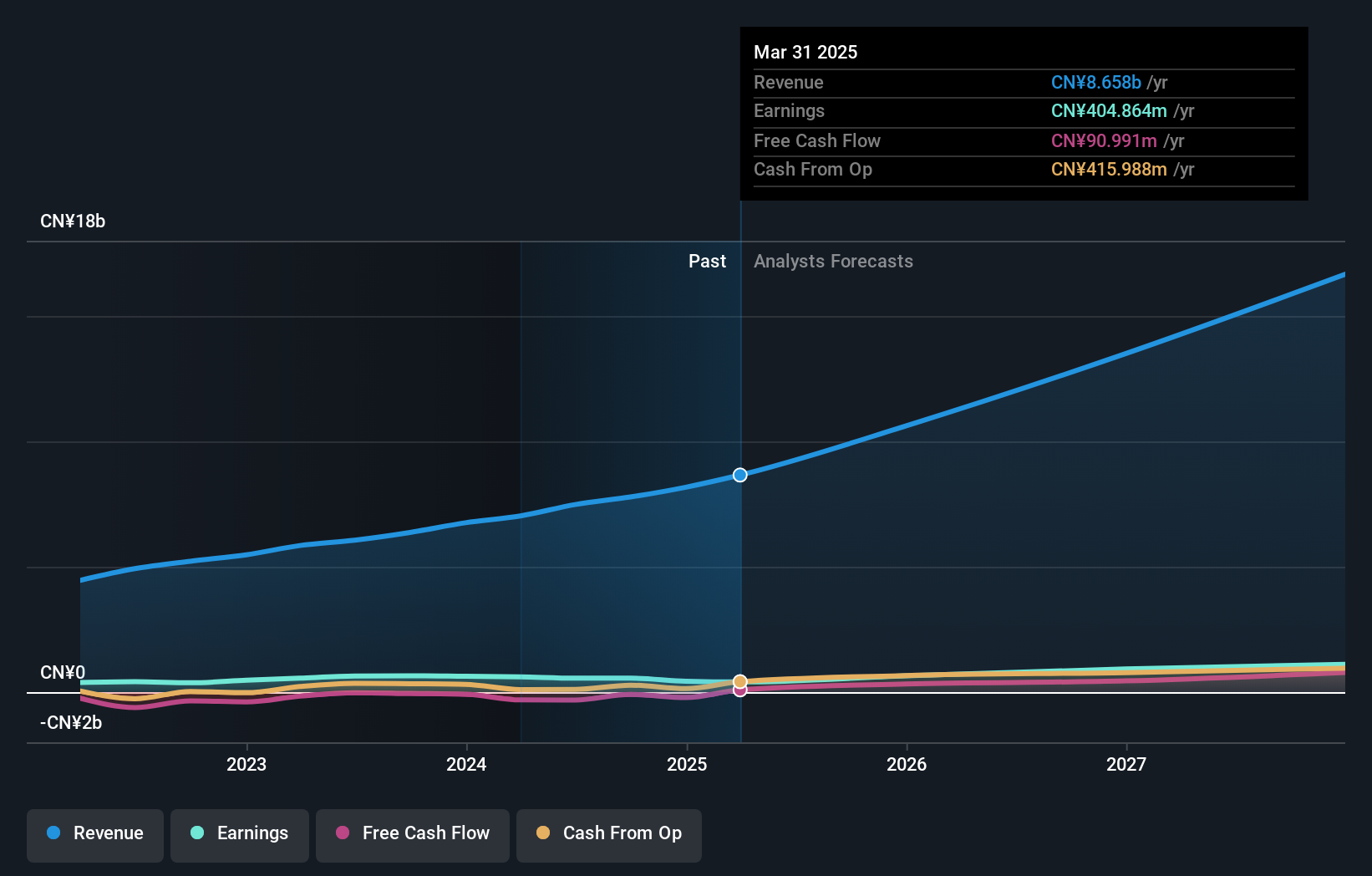

Shenzhen Megmeet Electrical (SZSE:002851)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shenzhen Megmeet Electrical Co., LTD is an electrical automation company in China with a market cap of CN¥40.94 billion.

Operations: Shenzhen Megmeet Electrical Co., LTD generates revenue through its electrical automation operations in China.

Insider Ownership: 33.1%

Revenue Growth Forecast: 25.6% p.a.

Shenzhen Megmeet Electrical shows promising growth potential with earnings forecasted to rise significantly at 58.1% annually, surpassing the Chinese market average. Despite a volatile share price and lower profit margins (2.6%) compared to last year, revenue is projected to grow robustly at 25.6% per year. Recent executive changes and amendments to company bylaws may impact future governance, while net income for the first nine months of 2025 decreased to CNY 212.62 million from CNY 411.15 million last year, reflecting current challenges.

- Unlock comprehensive insights into our analysis of Shenzhen Megmeet Electrical stock in this growth report.

- Our valuation report here indicates Shenzhen Megmeet Electrical may be overvalued.

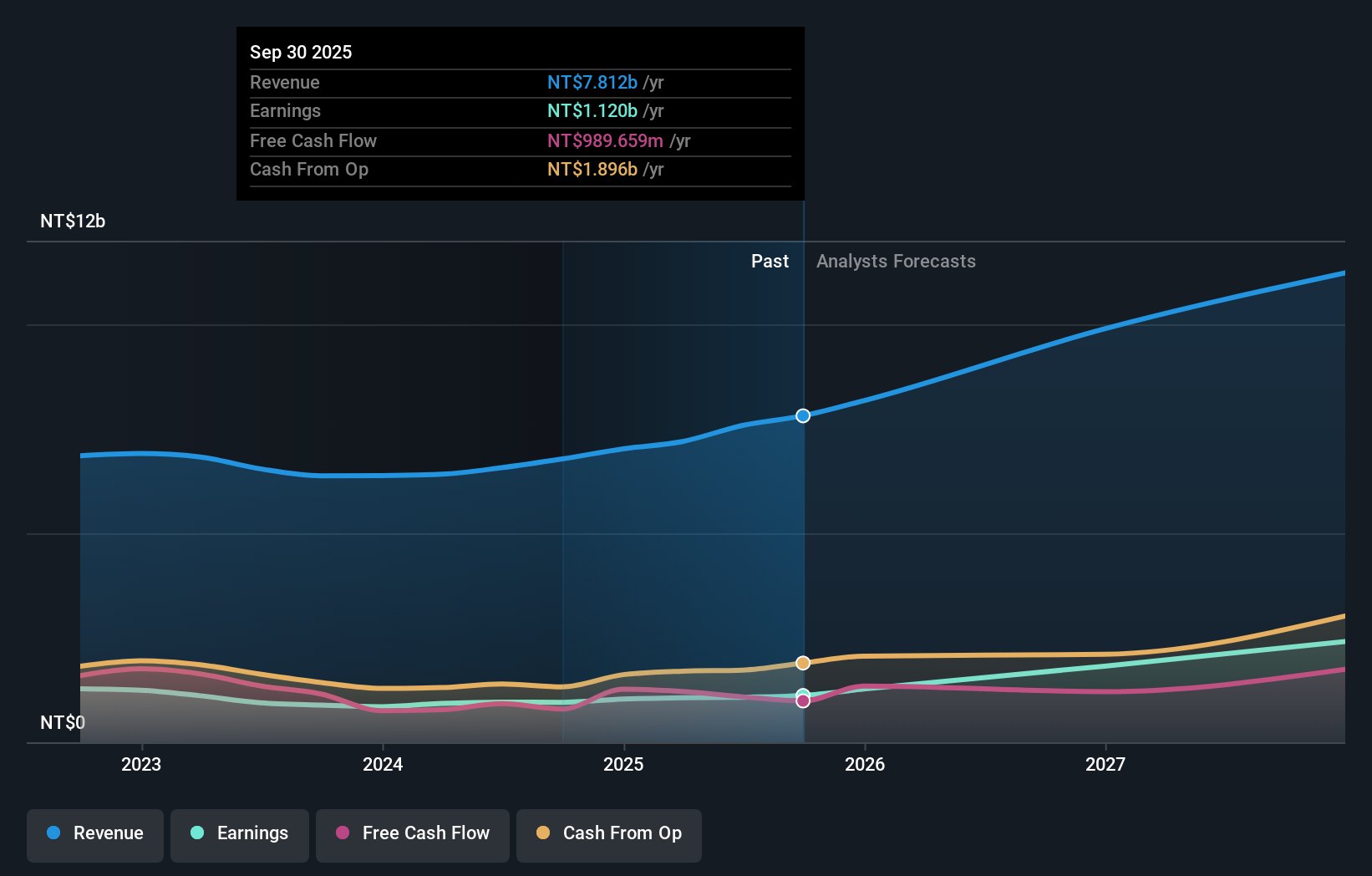

Kinik (TWSE:1560)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Kinik Company is engaged in the production and sale of abrasives, cutting tools, and reclaimed wafers both in Taiwan and internationally, with a market cap of NT$53.05 billion.

Operations: The company's revenue is derived from two main segments: the Electronics Sector, contributing NT$3.71 billion, and the Traditional Sectors, accounting for NT$4.10 billion.

Insider Ownership: 15.8%

Revenue Growth Forecast: 16.8% p.a.

Kinik demonstrates solid growth potential, with earnings projected to increase significantly at 34.2% annually, outpacing the Taiwanese market average. The company's revenue is also expected to grow faster than the market at 16.8% per year. Recent financial results show a rise in sales to TWD 2.09 billion for Q3 2025, up from TWD 1.86 billion a year ago, and net income increased to TWD 328.44 million from TWD 285.35 million last year, indicating strong performance momentum despite no significant insider trading activity recently noted.

- Take a closer look at Kinik's potential here in our earnings growth report.

- The analysis detailed in our Kinik valuation report hints at an inflated share price compared to its estimated value.

Where To Now?

- Gain an insight into the universe of 642 Fast Growing Asian Companies With High Insider Ownership by clicking here.

- Want To Explore Some Alternatives? Uncover 13 companies that survived and thrived after COVID and have the right ingredients to survive Trump's tariffs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002851

Shenzhen Megmeet Electrical

Operates as an electrical automation company in China.

High growth potential with adequate balance sheet.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

68 followersusers have followed this narrative

7 commentsusers have commented on this narrative

20 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.9% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

EN

Enemy on Halyk Bank of Kazakhstan ·

Halyk Bank of Kazakhstan will see revenue grow 11% as their future PE reaches 3.2x soon

Fair Value:US$52.2351.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Magma Silver ·

Silver's Breakout to over $50US will make Magma’s future shine with drill sampling returning 115g/t Silver and 2.3 g/t Gold at its Peru Mine

Fair Value:CA$0.3534.3% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on SEGRO ·

SEGRO's Revenue to Rise 14.7% Amidst Optimistic Growth Plans

Fair Value:UK£9.3925.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

961 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

68 followersusers have followed this narrative

7 commentsusers have commented on this narrative

20 likesusers have liked this narrative