Getting In Cheap On Harbin Boshi Automation Co., Ltd. (SZSE:002698) Is Unlikely

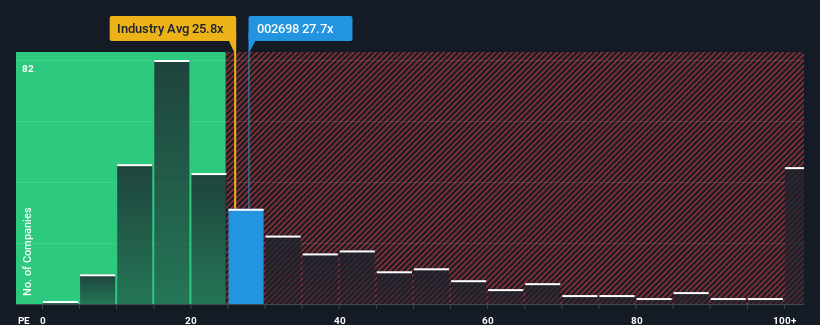

There wouldn't be many who think Harbin Boshi Automation Co., Ltd.'s (SZSE:002698) price-to-earnings (or "P/E") ratio of 27.7x is worth a mention when the median P/E in China is similar at about 26x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

Harbin Boshi Automation has been struggling lately as its earnings have declined faster than most other companies. One possibility is that the P/E is moderate because investors think the company's earnings trend will eventually fall in line with most others in the market. You'd much rather the company wasn't bleeding earnings if you still believe in the business. If not, then existing shareholders may be a little nervous about the viability of the share price.

See our latest analysis for Harbin Boshi Automation

What Are Growth Metrics Telling Us About The P/E?

Harbin Boshi Automation's P/E ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 8.9%. That put a dampener on the good run it was having over the longer-term as its three-year EPS growth is still a noteworthy 18% in total. So we can start by confirming that the company has generally done a good job of growing earnings over that time, even though it had some hiccups along the way.

Shifting to the future, estimates from the dual analysts covering the company suggest earnings should grow by 17% per annum over the next three years. With the market predicted to deliver 19% growth per year, the company is positioned for a weaker earnings result.

With this information, we find it interesting that Harbin Boshi Automation is trading at a fairly similar P/E to the market. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. Maintaining these prices will be difficult to achieve as this level of earnings growth is likely to weigh down the shares eventually.

The Final Word

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of Harbin Boshi Automation's analyst forecasts revealed that its inferior earnings outlook isn't impacting its P/E as much as we would have predicted. Right now we are uncomfortable with the P/E as the predicted future earnings aren't likely to support a more positive sentiment for long. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

Many other vital risk factors can be found on the company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Harbin Boshi Automation with six simple checks.

If these risks are making you reconsider your opinion on Harbin Boshi Automation, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Harbin Boshi Automation might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002698

Harbin Boshi Automation

Engages in the research and development, production, and sale of intelligent manufacturing equipment and industrial robots in the People’s Republic of China.

Excellent balance sheet average dividend payer.

Market Insights

Community Narratives