- China

- /

- Electrical

- /

- SZSE:002487

Dajin Heavy Industry Co.,Ltd.'s (SZSE:002487) 29% Jump Shows Its Popularity With Investors

Dajin Heavy Industry Co.,Ltd. (SZSE:002487) shares have had a really impressive month, gaining 29% after a shaky period beforehand. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 29% over that time.

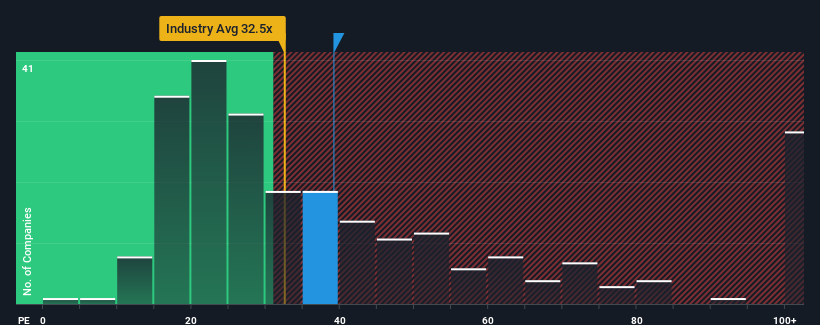

After such a large jump in price, Dajin Heavy IndustryLtd's price-to-earnings (or "P/E") ratio of 39.1x might make it look like a sell right now compared to the market in China, where around half of the companies have P/E ratios below 32x and even P/E's below 20x are quite common. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

Dajin Heavy IndustryLtd could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. It might be that many expect the dour earnings performance to recover substantially, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for Dajin Heavy IndustryLtd

How Is Dajin Heavy IndustryLtd's Growth Trending?

The only time you'd be truly comfortable seeing a P/E as high as Dajin Heavy IndustryLtd's is when the company's growth is on track to outshine the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 22%. This means it has also seen a slide in earnings over the longer-term as EPS is down 29% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Shifting to the future, estimates from the eight analysts covering the company suggest earnings should grow by 44% each year over the next three years. Meanwhile, the rest of the market is forecast to only expand by 26% per year, which is noticeably less attractive.

With this information, we can see why Dajin Heavy IndustryLtd is trading at such a high P/E compared to the market. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Bottom Line On Dajin Heavy IndustryLtd's P/E

The large bounce in Dajin Heavy IndustryLtd's shares has lifted the company's P/E to a fairly high level. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Dajin Heavy IndustryLtd's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Unless these conditions change, they will continue to provide strong support to the share price.

And what about other risks? Every company has them, and we've spotted 1 warning sign for Dajin Heavy IndustryLtd you should know about.

Of course, you might also be able to find a better stock than Dajin Heavy IndustryLtd. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002487

Dajin Heavy IndustryLtd

Develops, produces, and sells wind power equipment in China.

High growth potential with excellent balance sheet and pays a dividend.

Market Insights

Community Narratives