Advertisement

- China

- /

- Semiconductors

- /

- SZSE:300940

Three Undiscovered Gems in Asia with Promising Potential

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a landscape of fluctuating economic indicators, Asian equities present intriguing opportunities for investors, particularly in the small-cap segment. With manufacturing activity showing signs of contraction and private payrolls experiencing volatility, discovering stocks with strong fundamentals and growth potential becomes crucial for those looking to capitalize on the region's dynamic market environment.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Chuo WarehouseLtd | 12.82% | 2.30% | 6.14% | ★★★★★★ |

| Central Forest Group | NA | 5.20% | 24.71% | ★★★★★★ |

| JiangXi BaiSheng Intelligent Technology | NA | -8.48% | -19.51% | ★★★★★★ |

| China Post Technology | NA | -13.06% | 30.00% | ★★★★★★ |

| LanZhou Foci PharmaceuticalLtd | 1.63% | 7.07% | -12.27% | ★★★★★★ |

| Shenzhen China Micro Semicon | 6.54% | 5.94% | -43.71% | ★★★★★☆ |

| Changchun FAWAY Group Automobile Components | 4.23% | -1.01% | -7.40% | ★★★★★☆ |

| Shenzhen Jdd Tech New Material | 2.26% | 19.73% | 17.67% | ★★★★★☆ |

| Hangzhou Zhengqiang | 19.76% | 7.83% | 16.32% | ★★★★★☆ |

| Changzhou Nrb | 68.15% | 11.89% | 3.68% | ★★★★☆☆ |

Here's a peek at a few of the choices from the screener.

JiaoZuo WanFang Aluminum Manufacturing (SZSE:000612)

Simply Wall St Value Rating: ★★★★★★

Overview: JiaoZuo WanFang Aluminum Manufacturing Co., Ltd specializes in smelting and processing aluminum products in China, with a market cap of CN¥12.38 billion.

Operations: The company generates revenue primarily from its Electrolytic Aluminum and Aluminum Products segment, amounting to CN¥6.66 billion.

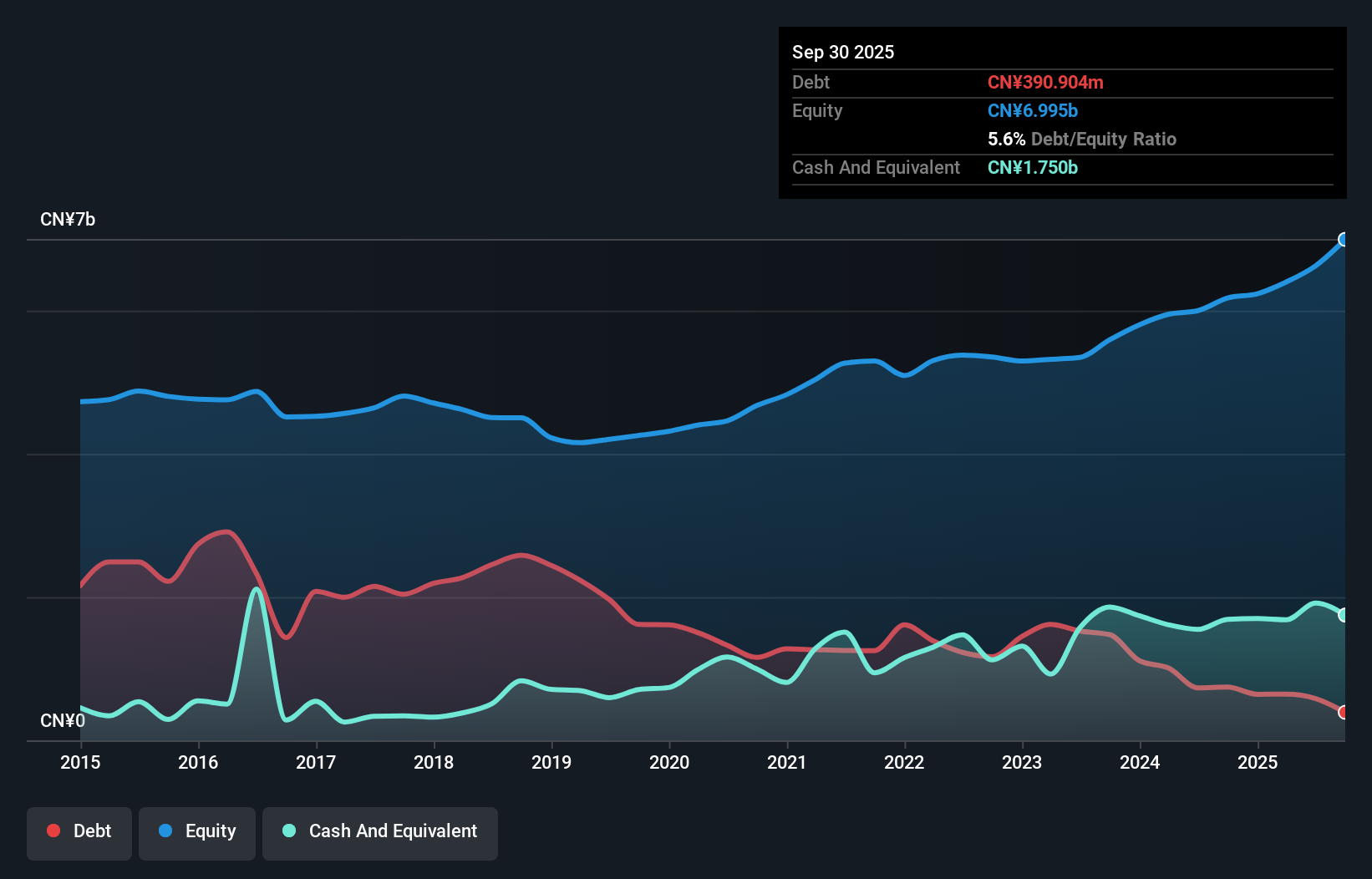

JiaoZuo WanFang Aluminum, a relatively small player in the aluminum industry, has demonstrated impressive financial health and growth. With earnings surging 25.9% over the past year, it outpaced its industry peers who grew at 8.4%. The company boasts a price-to-earnings ratio of 12.8x, significantly lower than the Chinese market average of 44.1x, suggesting potential undervaluation. Its net income for the first nine months of 2025 reached CNY 905.92 million compared to CNY 527.98 million last year, reflecting robust profitability with high-quality earnings supported by reduced debt levels from a debt-to-equity ratio of 24.7% to just 5.6% over five years.

- Delve into the full analysis health report here for a deeper understanding of JiaoZuo WanFang Aluminum Manufacturing.

Understand JiaoZuo WanFang Aluminum Manufacturing's track record by examining our Past report.

Dalian Huarui Heavy Industry Group (SZSE:002204)

Simply Wall St Value Rating: ★★★★★☆

Overview: Dalian Huarui Heavy Industry Group Co., LTD. is engaged in the manufacturing of special-purpose equipment and has a market cap of CN¥13.58 billion.

Operations: The primary revenue stream for Dalian Huarui Heavy Industry Group comes from its special-purpose equipment manufacturing segment, generating CN¥15.10 billion.

Dalian Huarui Heavy Industry Group, a notable player in the machinery sector, showcases robust financial health with earnings growth of 33.8% over the past year, outpacing the industry average of 6.1%. The company reported sales of CNY 10.98 billion for the first nine months of 2025, up from CNY 10.16 billion last year, while net income rose to CNY 489.77 million from CNY 395.08 million previously. With a price-to-earnings ratio at an attractive level of 22.9x compared to the CN market's average of 44.1x and high-quality earnings reported, Dalian Huarui seems well-positioned for continued success in its field.

Shen Zhen Australis Electronic TechnologyLtd (SZSE:300940)

Simply Wall St Value Rating: ★★★★★☆

Overview: Shen Zhen Australis Electronic Technology Ltd, with a market cap of CN¥6.94 billion, is engaged in the development and production of electronic components and systems.

Operations: The company generates revenue primarily from the sale of electronic components and systems. It has a market cap of CN¥6.94 billion, reflecting its position in the industry.

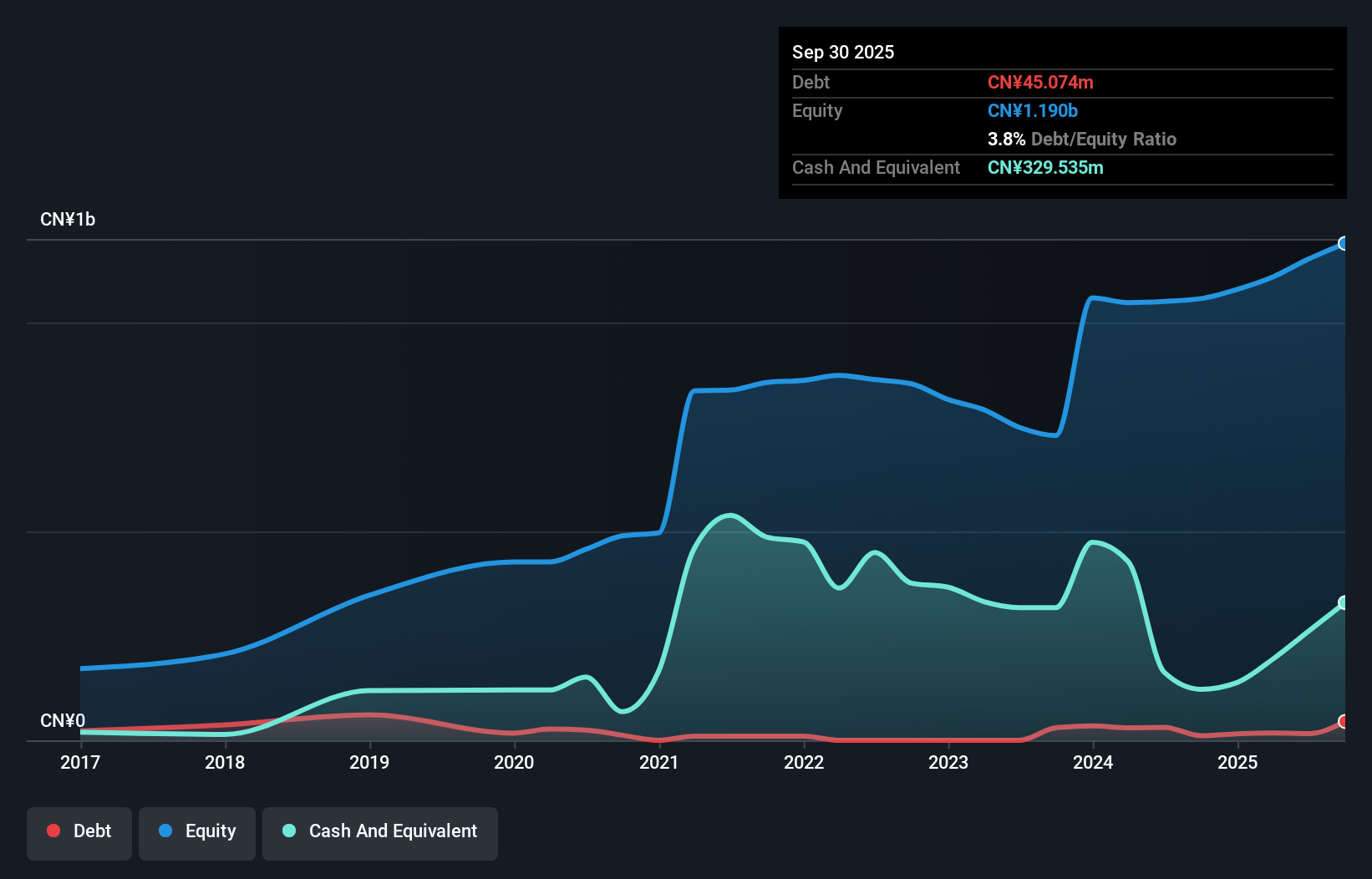

Shen Zhen Australis Electronic Technology Co., Ltd. has shown impressive financial performance, with sales reaching CNY 615.33 million for the first nine months of 2025, a significant rise from CNY 238.34 million the previous year. Net income also turned positive at CNY 110.14 million compared to a net loss of CNY 1.55 million last year, indicating strong operational efficiency and profitability growth in recent periods. Despite an increased debt-to-equity ratio from 2.5 to 3.8 over five years, the company maintains more cash than total debt and earns sufficient interest to cover its obligations comfortably, reflecting sound financial health amidst industry volatility.

Turning Ideas Into Actions

- Dive into all 2502 of the Asian Undiscovered Gems With Strong Fundamentals we have identified here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300940

Shen Zhen Australis Electronic TechnologyLtd

Shen Zhen Australis Electronic Technology Co.,Ltd.

Excellent balance sheet with moderate growth potential.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

64 followersusers have followed this narrative

7 commentsusers have commented on this narrative

19 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Magma Silver ·

Silver's Breakout to over $50US will make Magma’s future shine with drill sampling returning 115g/t Silver and 2.3 g/t Gold at its Peru Mine

Fair Value:CA$0.3534.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on SEGRO ·

SEGRO's Revenue to Rise 14.7% Amidst Optimistic Growth Plans

Fair Value:UK£9.3924.7% undervalued

0 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PI

PicaCoder on Microsoft ·

After the AI Party: A Sobering Look at Microsoft's Future

Fair Value:US$42015.0% overvalued

62 followersusers have followed this narrative

12 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

958 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

64 followersusers have followed this narrative

7 commentsusers have commented on this narrative

19 likesusers have liked this narrative