Insufficient Growth At Guangdong Hongtu Technology (holdings) Co.,Ltd. (SZSE:002101) Hampers Share Price

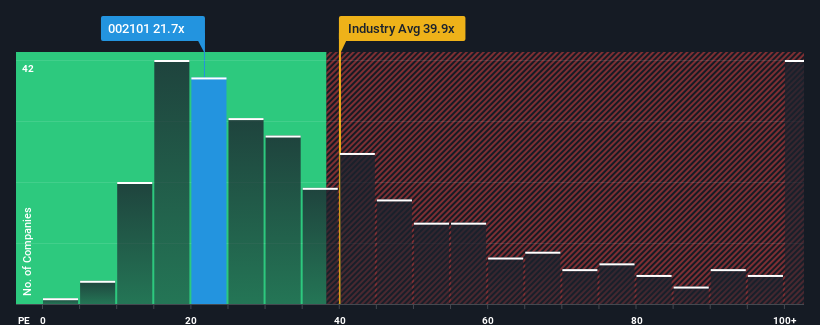

When close to half the companies in China have price-to-earnings ratios (or "P/E's") above 39x, you may consider Guangdong Hongtu Technology (holdings) Co.,Ltd. (SZSE:002101) as an attractive investment with its 21.7x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

With earnings that are retreating more than the market's of late, Guangdong Hongtu Technology (holdings)Ltd has been very sluggish. It seems that many are expecting the dismal earnings performance to persist, which has repressed the P/E. You'd much rather the company wasn't bleeding earnings if you still believe in the business. Or at the very least, you'd be hoping the earnings slide doesn't get any worse if your plan is to pick up some stock while it's out of favour.

View our latest analysis for Guangdong Hongtu Technology (holdings)Ltd

How Is Guangdong Hongtu Technology (holdings)Ltd's Growth Trending?

There's an inherent assumption that a company should underperform the market for P/E ratios like Guangdong Hongtu Technology (holdings)Ltd's to be considered reasonable.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 25%. This has soured the latest three-year period, which nevertheless managed to deliver a decent 14% overall rise in EPS. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of earnings growth.

Shifting to the future, estimates from the dual analysts covering the company suggest earnings should grow by 32% over the next year. Meanwhile, the rest of the market is forecast to expand by 37%, which is noticeably more attractive.

In light of this, it's understandable that Guangdong Hongtu Technology (holdings)Ltd's P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

What We Can Learn From Guangdong Hongtu Technology (holdings)Ltd's P/E?

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Guangdong Hongtu Technology (holdings)Ltd's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Don't forget that there may be other risks. For instance, we've identified 1 warning sign for Guangdong Hongtu Technology (holdings)Ltd that you should be aware of.

If you're unsure about the strength of Guangdong Hongtu Technology (holdings)Ltd's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002101

Guangdong Hongtu Technology (holdings)Ltd

Designs, develops, manufactures, and sells precision aluminum alloy die castings and related accessories used in automotive, communication, and electromechanical products in China.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Community Narratives