Advertisement

Shandong Weida Machinery (SZSE:002026) Is Increasing Its Dividend To CN¥0.12

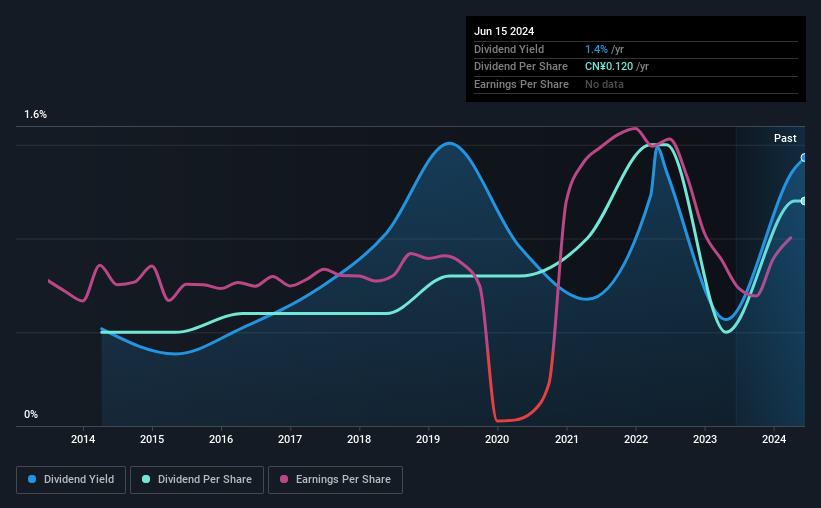

Shandong Weida Machinery Co., Ltd. (SZSE:002026) has announced that it will be increasing its dividend from last year's comparable payment on the 21st of June to CN¥0.12. Although the dividend is now higher, the yield is only 1.4%, which is below the industry average.

View our latest analysis for Shandong Weida Machinery

Shandong Weida Machinery's Earnings Easily Cover The Distributions

While yield is important, another factor to consider about a company's dividend is whether the current payout levels are feasible. Before making this announcement, Shandong Weida Machinery was easily earning enough to cover the dividend. As a result, a large proportion of what it earned was being reinvested back into the business.

The next year is set to see EPS grow by 14.1%. Assuming the dividend continues along recent trends, we think the payout ratio could be 24% by next year, which is in a pretty sustainable range.

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. The dividend has gone from an annual total of CN¥0.05 in 2014 to the most recent total annual payment of CN¥0.12. This means that it has been growing its distributions at 9.1% per annum over that time. We like to see dividends have grown at a reasonable rate, but with at least one substantial cut in the payments, we're not certain this dividend stock would be ideal for someone intending to live on the income.

The Dividend's Growth Prospects Are Limited

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. Earnings has been rising at 4.2% per annum over the last five years, which admittedly is a bit slow. While EPS growth is quite low, Shandong Weida Machinery has the option to increase the payout ratio to return more cash to shareholders.

In Summary

In summary, it's great to see that the company can raise the dividend and keep it in a sustainable range. The dividend has been at reasonable levels historically, but that hasn't translated into a consistent payment. The dividend looks okay, but there have been some issues in the past, so we would be a little bit cautious.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. For example, we've picked out 1 warning sign for Shandong Weida Machinery that investors should know about before committing capital to this stock. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002026

Shandong Weida Machinery

Engages in the manufacture and sale of drill chucks in China and internationally.

Solid track record with excellent balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor