Advertisement

What Zhejiang XiaSha Precision Manufacturing Co., Ltd.'s (SZSE:001306) 26% Share Price Gain Is Not Telling You

Zhejiang XiaSha Precision Manufacturing Co., Ltd. (SZSE:001306) shares have had a really impressive month, gaining 26% after a shaky period beforehand. Longer-term shareholders would be thankful for the recovery in the share price since it's now virtually flat for the year after the recent bounce.

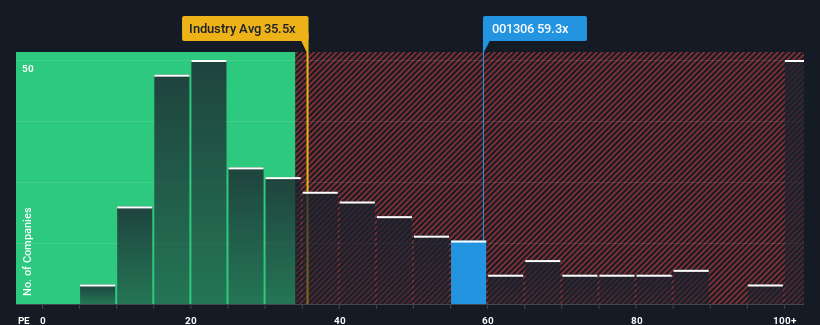

Following the firm bounce in price, Zhejiang XiaSha Precision Manufacturing's price-to-earnings (or "P/E") ratio of 59.3x might make it look like a strong sell right now compared to the market in China, where around half of the companies have P/E ratios below 36x and even P/E's below 21x are quite common. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

For instance, Zhejiang XiaSha Precision Manufacturing's receding earnings in recent times would have to be some food for thought. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for Zhejiang XiaSha Precision Manufacturing

What Are Growth Metrics Telling Us About The High P/E?

In order to justify its P/E ratio, Zhejiang XiaSha Precision Manufacturing would need to produce outstanding growth well in excess of the market.

Retrospectively, the last year delivered a frustrating 34% decrease to the company's bottom line. This means it has also seen a slide in earnings over the longer-term as EPS is down 47% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

In contrast to the company, the rest of the market is expected to grow by 41% over the next year, which really puts the company's recent medium-term earnings decline into perspective.

With this information, we find it concerning that Zhejiang XiaSha Precision Manufacturing is trading at a P/E higher than the market. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as a continuation of recent earnings trends is likely to weigh heavily on the share price eventually.

The Bottom Line On Zhejiang XiaSha Precision Manufacturing's P/E

Zhejiang XiaSha Precision Manufacturing's P/E is flying high just like its stock has during the last month. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Our examination of Zhejiang XiaSha Precision Manufacturing revealed its shrinking earnings over the medium-term aren't impacting its high P/E anywhere near as much as we would have predicted, given the market is set to grow. Right now we are increasingly uncomfortable with the high P/E as this earnings performance is highly unlikely to support such positive sentiment for long. If recent medium-term earnings trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Zhejiang XiaSha Precision Manufacturing (at least 1 which doesn't sit too well with us), and understanding them should be part of your investment process.

You might be able to find a better investment than Zhejiang XiaSha Precision Manufacturing. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang XiaSha Precision Manufacturing might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:001306

Zhejiang XiaSha Precision Manufacturing

Zhejiang XiaSha Precision Manufacturing Co., Ltd.

Adequate balance sheet slight.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor