More Unpleasant Surprises Could Be In Store For Wave Cyber (Shanghai)Co., Ltd.'s (SHSE:688718) Shares After Tumbling 26%

The Wave Cyber (Shanghai)Co., Ltd. (SHSE:688718) share price has fared very poorly over the last month, falling by a substantial 26%. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 49% in that time.

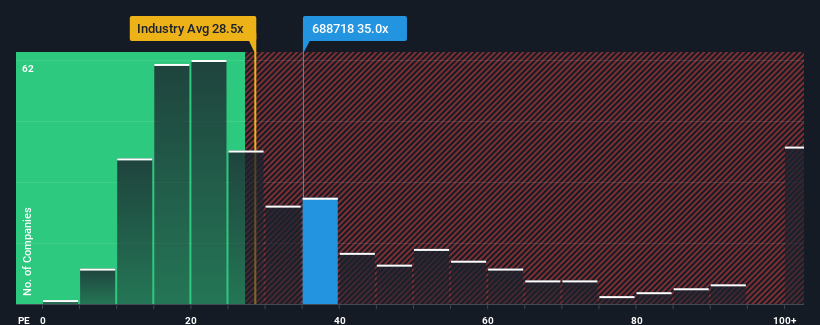

Even after such a large drop in price, given around half the companies in China have price-to-earnings ratios (or "P/E's") below 30x, you may still consider Wave Cyber (Shanghai)Co as a stock to potentially avoid with its 35x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

Recent times have been advantageous for Wave Cyber (Shanghai)Co as its earnings have been rising faster than most other companies. It seems that many are expecting the strong earnings performance to persist, which has raised the P/E. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for Wave Cyber (Shanghai)Co

Does Growth Match The High P/E?

In order to justify its P/E ratio, Wave Cyber (Shanghai)Co would need to produce impressive growth in excess of the market.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 14% last year. However, this wasn't enough as the latest three year period has seen an unpleasant 49% overall drop in EPS. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Turning to the outlook, the next three years should generate growth of 22% each year as estimated by the only analyst watching the company. Meanwhile, the rest of the market is forecast to expand by 25% each year, which is noticeably more attractive.

With this information, we find it concerning that Wave Cyber (Shanghai)Co is trading at a P/E higher than the market. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of earnings growth is likely to weigh heavily on the share price eventually.

The Final Word

Wave Cyber (Shanghai)Co's P/E hasn't come down all the way after its stock plunged. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of Wave Cyber (Shanghai)Co's analyst forecasts revealed that its inferior earnings outlook isn't impacting its high P/E anywhere near as much as we would have predicted. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

A lot of potential risks can sit within a company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Wave Cyber (Shanghai)Co with six simple checks.

If you're unsure about the strength of Wave Cyber (Shanghai)Co's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

If you're looking to trade Wave Cyber (Shanghai), open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Wave Cyber (Shanghai) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688718

Wave Cyber (Shanghai)

Designs, produces, and sells water treatment components.

Flawless balance sheet and overvalued.

Market Insights

Community Narratives