Advertisement

Freewon China Co.,Ltd. (SHSE:688678) Soars 25% But It's A Story Of Risk Vs Reward

Freewon China Co.,Ltd. (SHSE:688678) shares have continued their recent momentum with a 25% gain in the last month alone. Notwithstanding the latest gain, the annual share price return of 7.0% isn't as impressive.

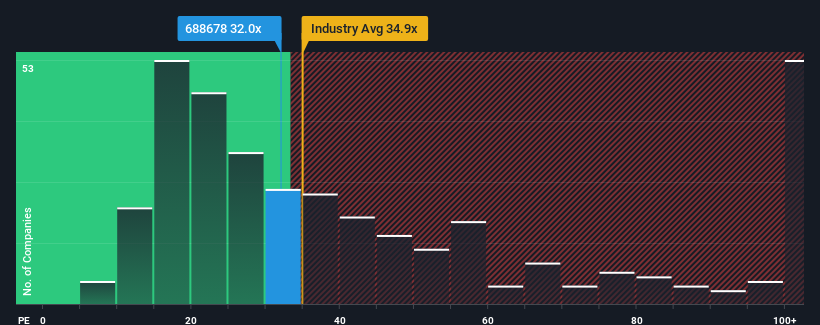

Although its price has surged higher, you could still be forgiven for feeling indifferent about Freewon ChinaLtd's P/E ratio of 32x, since the median price-to-earnings (or "P/E") ratio in China is also close to 35x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

Freewon ChinaLtd's negative earnings growth of late has neither been better nor worse than most other companies. The P/E is probably moderate because investors think the company's earnings trend will continue to follow the rest of the market. You'd much rather the company wasn't bleeding earnings if you still believe in the business. At the very least, you'd be hoping that earnings don't accelerate downwards if your plan is to pick up some stock while it's not in favour.

Check out our latest analysis for Freewon ChinaLtd

What Are Growth Metrics Telling Us About The P/E?

In order to justify its P/E ratio, Freewon ChinaLtd would need to produce growth that's similar to the market.

If we review the last year of earnings, the company posted a result that saw barely any deviation from a year ago. Whilst it's an improvement, it wasn't enough to get the company out of the hole it was in, with earnings down 26% overall from three years ago. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 68% during the coming year according to the only analyst following the company. Meanwhile, the rest of the market is forecast to only expand by 39%, which is noticeably less attractive.

With this information, we find it interesting that Freewon ChinaLtd is trading at a fairly similar P/E to the market. It may be that most investors aren't convinced the company can achieve future growth expectations.

The Bottom Line On Freewon ChinaLtd's P/E

Freewon ChinaLtd appears to be back in favour with a solid price jump getting its P/E back in line with most other companies. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of Freewon ChinaLtd's analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E as much as we would have predicted. There could be some unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. It appears some are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

You need to take note of risks, for example - Freewon ChinaLtd has 2 warning signs (and 1 which makes us a bit uncomfortable) we think you should know about.

Of course, you might also be able to find a better stock than Freewon ChinaLtd. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688678

Freewon ChinaLtd

Engages in the research and development, manufacture, and sale of precision metal parts.

Moderate growth potential with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|29.9% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.8% undervalued

AG

Community Contributor