Market Participants Recognise Beijing SinoHytec Co., Ltd.'s (SHSE:688339) Revenues Pushing Shares 37% Higher

Beijing SinoHytec Co., Ltd. (SHSE:688339) shareholders have had their patience rewarded with a 37% share price jump in the last month. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 26% in the last twelve months.

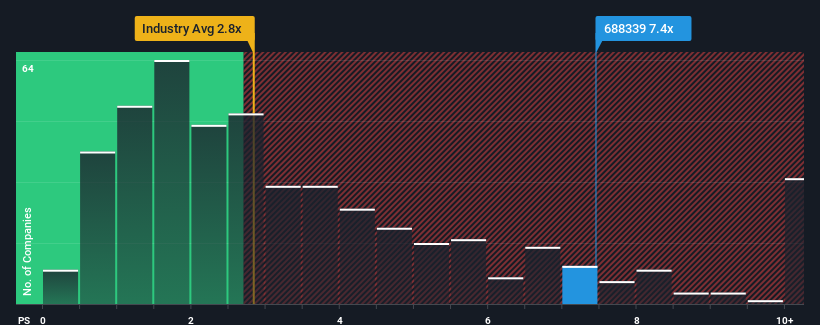

Following the firm bounce in price, you could be forgiven for thinking Beijing SinoHytec is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 7.4x, considering almost half the companies in China's Machinery industry have P/S ratios below 2.8x. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Beijing SinoHytec

What Does Beijing SinoHytec's Recent Performance Look Like?

Beijing SinoHytec certainly has been doing a good job lately as it's been growing revenue more than most other companies. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Beijing SinoHytec.Do Revenue Forecasts Match The High P/S Ratio?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Beijing SinoHytec's to be considered reasonable.

If we review the last year of revenue growth, the company posted a terrific increase of 29%. Revenue has also lifted 20% in aggregate from three years ago, mostly thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

Turning to the outlook, the next year should generate growth of 64% as estimated by the seven analysts watching the company. With the industry only predicted to deliver 23%, the company is positioned for a stronger revenue result.

With this in mind, it's not hard to understand why Beijing SinoHytec's P/S is high relative to its industry peers. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Bottom Line On Beijing SinoHytec's P/S

The strong share price surge has lead to Beijing SinoHytec's P/S soaring as well. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Beijing SinoHytec maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Machinery industry, as expected. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

Having said that, be aware Beijing SinoHytec is showing 1 warning sign in our investment analysis, you should know about.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Beijing SinoHytec might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688339

Beijing SinoHytec

Engages in the research, development, and industrialization of fuel cell engine systems in Mainland China, Canada, and South Korea.

Adequate balance sheet and slightly overvalued.

Similar Companies

Market Insights

Community Narratives