Jiangsu Beiren Robot System Co., Ltd's (SHSE:688218) 44% Jump Shows Its Popularity With Investors

Jiangsu Beiren Robot System Co., Ltd (SHSE:688218) shares have had a really impressive month, gaining 44% after a shaky period beforehand. But the gains over the last month weren't enough to make shareholders whole, as the share price is still down 4.2% in the last twelve months.

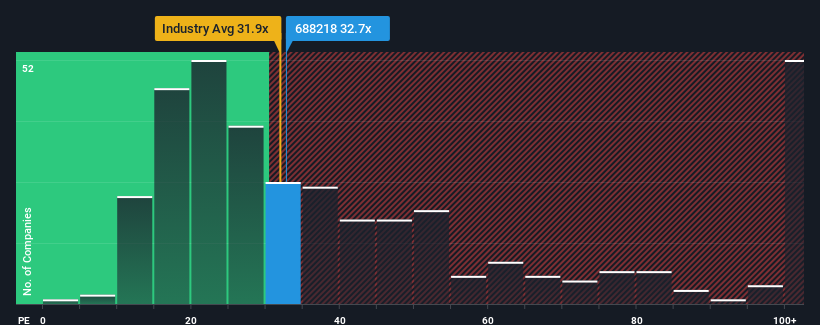

In spite of the firm bounce in price, there still wouldn't be many who think Jiangsu Beiren Robot System's price-to-earnings (or "P/E") ratio of 32.7x is worth a mention when the median P/E in China is similar at about 34x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

As an illustration, earnings have deteriorated at Jiangsu Beiren Robot System over the last year, which is not ideal at all. It might be that many expect the company to put the disappointing earnings performance behind them over the coming period, which has kept the P/E from falling. If you like the company, you'd at least be hoping this is the case so that you could potentially pick up some stock while it's not quite in favour.

See our latest analysis for Jiangsu Beiren Robot System

What Are Growth Metrics Telling Us About The P/E?

In order to justify its P/E ratio, Jiangsu Beiren Robot System would need to produce growth that's similar to the market.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 4.0%. Even so, admirably EPS has lifted 175% in aggregate from three years ago, notwithstanding the last 12 months. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

Comparing that to the market, which is predicted to deliver 37% growth in the next 12 months, the company's momentum is pretty similar based on recent medium-term annualised earnings results.

With this information, we can see why Jiangsu Beiren Robot System is trading at a fairly similar P/E to the market. Apparently shareholders are comfortable to simply hold on assuming the company will continue keeping a low profile.

The Final Word

Its shares have lifted substantially and now Jiangsu Beiren Robot System's P/E is also back up to the market median. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Jiangsu Beiren Robot System revealed its three-year earnings trends are contributing to its P/E, given they look similar to current market expectations. At this stage investors feel the potential for an improvement or deterioration in earnings isn't great enough to justify a high or low P/E ratio. Unless the recent medium-term conditions change, they will continue to support the share price at these levels.

You always need to take note of risks, for example - Jiangsu Beiren Robot System has 2 warning signs we think you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688218

Jiangsu Beiren Robot System

Engages in the research and development, design, production, assembly, and sale of production lines primarily in China.

Adequate balance sheet slight.

Market Insights

Community Narratives