3 Growth Stocks With High Insider Ownership And Earnings Growth Up To 111%

Reviewed by Simply Wall St

In recent weeks, global markets have experienced fluctuations driven by tariff uncertainties and mixed economic data, with U.S. stocks ending lower despite strong earnings reports from many companies. Amid these market conditions, investors often look for growth companies with high insider ownership as a sign of confidence in the company's future potential and alignment of interests between management and shareholders.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 17.3% | 22.8% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 26.2% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| CD Projekt (WSE:CDR) | 29.7% | 39.4% |

| Pharma Mar (BME:PHM) | 11.9% | 44.7% |

| Medley (TSE:4480) | 34.1% | 27.3% |

| Kingstone Companies (NasdaqCM:KINS) | 20.8% | 24.9% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 121.1% |

| Plenti Group (ASX:PLT) | 12.7% | 120.1% |

| Findi (ASX:FND) | 35.8% | 111.4% |

Below we spotlight a couple of our favorites from our exclusive screener.

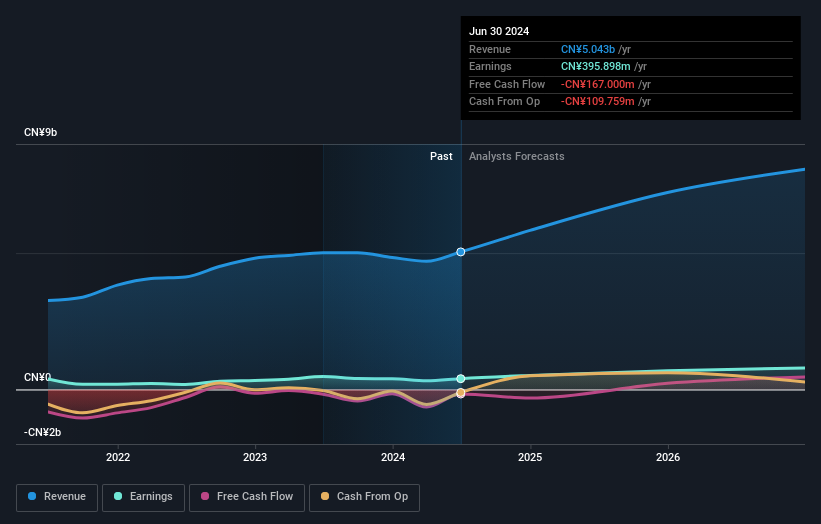

Bozhon Precision Industry TechnologyLtd (SHSE:688097)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Bozhon Precision Industry Technology Co., Ltd. (ticker: SHSE:688097) operates in the precision machinery industry and has a market cap of CN¥12.56 billion.

Operations: In the precision machinery sector, SHSE:688097 generates revenue primarily from its Industrial Automation & Controls segment, amounting to CN¥4.87 billion.

Insider Ownership: 29.4%

Earnings Growth Forecast: 27% p.a.

Bozhon Precision Industry Technology Ltd. is experiencing robust growth, with revenue expected to increase by 20.9% annually, surpassing the broader Chinese market's 13.6%. Earnings are projected to grow significantly at 27% per year, outpacing the market average of 25.5%. Despite a lower-than-market price-to-earnings ratio of 29.7x, recent insider transactions include a CNY 480 million acquisition of a 5.43% stake by Tianjin Xinke Hongchuang Equity Investment Partnership Enterprise, highlighting substantial insider interest and involvement in the company’s future trajectory.

- Navigate through the intricacies of Bozhon Precision Industry TechnologyLtd with our comprehensive analyst estimates report here.

- According our valuation report, there's an indication that Bozhon Precision Industry TechnologyLtd's share price might be on the expensive side.

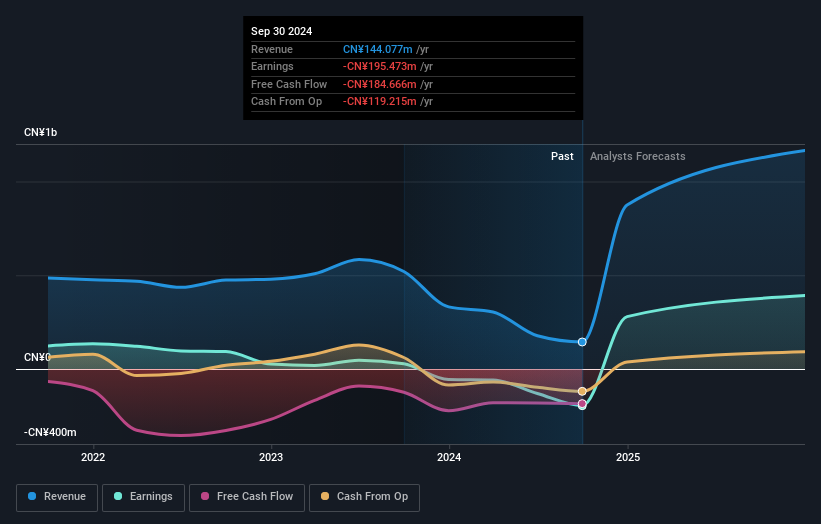

Chengdu M&S Electronics TechnologyLtd (SHSE:688311)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Chengdu M&S Electronics Technology Co., Ltd. (ticker: SHSE:688311) operates in the electronics sector with a market cap of CN¥4.96 billion.

Operations: Chengdu M&S Electronics Technology Co., Ltd. generates its revenue through various segments within the electronics sector.

Insider Ownership: 30%

Earnings Growth Forecast: 111.5% p.a.

Chengdu M&S Electronics Technology Ltd. is poised for significant growth, with revenue forecasted to surge by 66.9% annually, outstripping the Chinese market's 13.6%. Earnings are expected to grow at a very large rate of 111.54% per year, positioning the company towards profitability within three years—an above-average market trajectory. Despite recent removal from the S&P Global BMI Index and high share price volatility, substantial insider ownership suggests confidence in its long-term potential.

- Delve into the full analysis future growth report here for a deeper understanding of Chengdu M&S Electronics TechnologyLtd.

- Our valuation report unveils the possibility Chengdu M&S Electronics TechnologyLtd's shares may be trading at a premium.

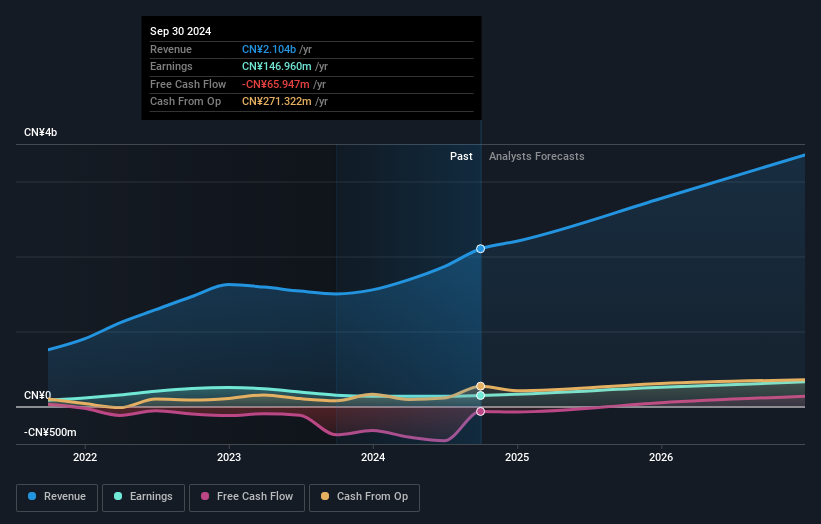

Suzhou Recodeal Interconnect SystemLtd (SHSE:688800)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Suzhou Recodeal Interconnect System Co., Ltd is engaged in the development, production, and sale of connection systems and microwave components globally, with a market capitalization of approximately CN¥10.37 billion.

Operations: The company generates revenue primarily from its Electric Equipment segment, amounting to CN¥2.10 billion.

Insider Ownership: 38.5%

Earnings Growth Forecast: 36.8% p.a.

Suzhou Recodeal Interconnect System Ltd. is set for robust growth, with revenue anticipated to increase by 21.5% annually, surpassing the broader Chinese market's growth rate of 13.6%. Earnings are expected to rise significantly at 36.8% per year, although recent profit margins have declined from last year’s figures. Despite high share price volatility and no significant insider trading activity recently, insider ownership may indicate confidence in its future prospects.

- Take a closer look at Suzhou Recodeal Interconnect SystemLtd's potential here in our earnings growth report.

- In light of our recent valuation report, it seems possible that Suzhou Recodeal Interconnect SystemLtd is trading beyond its estimated value.

Make It Happen

- Unlock our comprehensive list of 1441 Fast Growing Companies With High Insider Ownership by clicking here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Bozhon Precision Industry TechnologyLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688097

Bozhon Precision Industry TechnologyLtd

Bozhon Precision Industry Technology Co.,Ltd.

High growth potential with excellent balance sheet.

Market Insights

Community Narratives