- China

- /

- Electrical

- /

- SHSE:688006

Market Might Still Lack Some Conviction On Zhejiang HangKe Technology Incorporated Company (SHSE:688006) Even After 52% Share Price Boost

Zhejiang HangKe Technology Incorporated Company (SHSE:688006) shareholders would be excited to see that the share price has had a great month, posting a 52% gain and recovering from prior weakness. The bad news is that even after the stocks recovery in the last 30 days, shareholders are still underwater by about 7.5% over the last year.

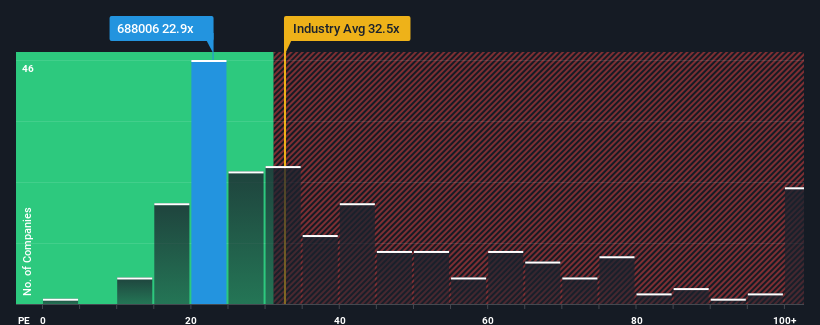

Although its price has surged higher, Zhejiang HangKe Technology may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 22.9x, since almost half of all companies in China have P/E ratios greater than 34x and even P/E's higher than 64x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

Zhejiang HangKe Technology has been struggling lately as its earnings have declined faster than most other companies. The P/E is probably low because investors think this poor earnings performance isn't going to improve at all. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. If not, then existing shareholders will probably struggle to get excited about the future direction of the share price.

See our latest analysis for Zhejiang HangKe Technology

Is There Any Growth For Zhejiang HangKe Technology?

Zhejiang HangKe Technology's P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

Retrospectively, the last year delivered a frustrating 20% decrease to the company's bottom line. Still, the latest three year period has seen an excellent 84% overall rise in EPS, in spite of its unsatisfying short-term performance. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

Looking ahead now, EPS is anticipated to climb by 23% per year during the coming three years according to the seven analysts following the company. Meanwhile, the rest of the market is forecast to only expand by 19% per year, which is noticeably less attractive.

In light of this, it's peculiar that Zhejiang HangKe Technology's P/E sits below the majority of other companies. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

The Key Takeaway

Despite Zhejiang HangKe Technology's shares building up a head of steam, its P/E still lags most other companies. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of Zhejiang HangKe Technology's analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E anywhere near as much as we would have predicted. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. At least price risks look to be very low, but investors seem to think future earnings could see a lot of volatility.

There are also other vital risk factors to consider and we've discovered 3 warning signs for Zhejiang HangKe Technology (1 can't be ignored!) that you should be aware of before investing here.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang HangKe Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688006

Zhejiang HangKe Technology

Designs, develops, produces, and sells lithium-ion (Li-ion) battery post-processing systems for charging and discharging industry in China and internationally.

Flawless balance sheet with high growth potential.

Market Insights

Community Narratives