Advertisement

Shanghai Kelai Mechatronics Engineering Co.,Ltd. (SHSE:603960) Stocks Pounded By 28% But Not Lagging Market On Growth Or Pricing

The Shanghai Kelai Mechatronics Engineering Co.,Ltd. (SHSE:603960) share price has softened a substantial 28% over the previous 30 days, handing back much of the gains the stock has made lately. Still, a bad month hasn't completely ruined the past year with the stock gaining 38%, which is great even in a bull market.

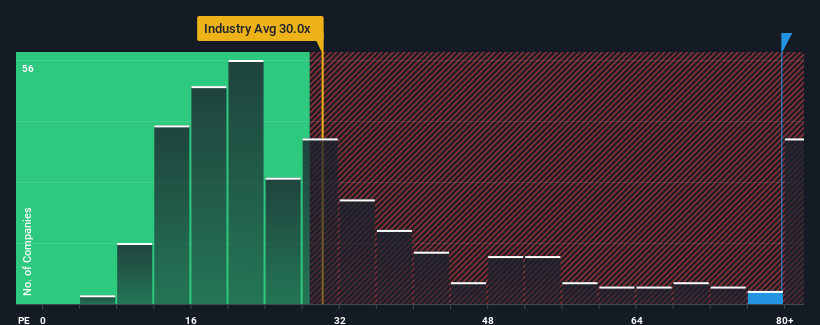

In spite of the heavy fall in price, given close to half the companies in China have price-to-earnings ratios (or "P/E's") below 29x, you may still consider Shanghai Kelai Mechatronics EngineeringLtd as a stock to avoid entirely with its 79.6x P/E ratio. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

With earnings growth that's superior to most other companies of late, Shanghai Kelai Mechatronics EngineeringLtd has been doing relatively well. The P/E is probably high because investors think this strong earnings performance will continue. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for Shanghai Kelai Mechatronics EngineeringLtd

Does Growth Match The High P/E?

The only time you'd be truly comfortable seeing a P/E as steep as Shanghai Kelai Mechatronics EngineeringLtd's is when the company's growth is on track to outshine the market decidedly.

Taking a look back first, we see that the company grew earnings per share by an impressive 206% last year. However, this wasn't enough as the latest three year period has seen a very unpleasant 40% drop in EPS in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Turning to the outlook, the next year should generate growth of 58% as estimated by the dual analysts watching the company. That's shaping up to be materially higher than the 36% growth forecast for the broader market.

With this information, we can see why Shanghai Kelai Mechatronics EngineeringLtd is trading at such a high P/E compared to the market. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Bottom Line On Shanghai Kelai Mechatronics EngineeringLtd's P/E

Shanghai Kelai Mechatronics EngineeringLtd's shares may have retreated, but its P/E is still flying high. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Shanghai Kelai Mechatronics EngineeringLtd's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Unless these conditions change, they will continue to provide strong support to the share price.

It is also worth noting that we have found 1 warning sign for Shanghai Kelai Mechatronics EngineeringLtd that you need to take into consideration.

Of course, you might also be able to find a better stock than Shanghai Kelai Mechatronics EngineeringLtd. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603960

Shanghai Kelai Mechatronics EngineeringLtd

Shanghai Kelai Mechatronics Engineering Co.,Ltd.

Flawless balance sheet with high growth potential.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor