Advertisement

Investors Continue Waiting On Sidelines For Hangzhou Youngsun Intelligent Equipment Co., Ltd. (SHSE:603901)

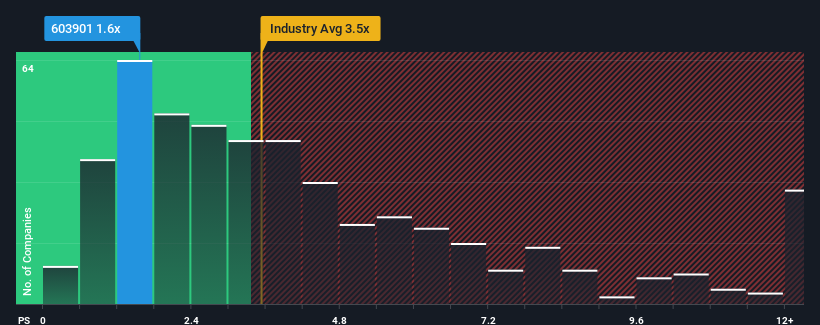

Hangzhou Youngsun Intelligent Equipment Co., Ltd.'s (SHSE:603901) price-to-sales (or "P/S") ratio of 1.6x might make it look like a buy right now compared to the Machinery industry in China, where around half of the companies have P/S ratios above 3.5x and even P/S above 6x are quite common. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

See our latest analysis for Hangzhou Youngsun Intelligent Equipment

What Does Hangzhou Youngsun Intelligent Equipment's Recent Performance Look Like?

There hasn't been much to differentiate Hangzhou Youngsun Intelligent Equipment's and the industry's revenue growth lately. Perhaps the market is expecting future revenue performance to dive, which has kept the P/S suppressed. If you like the company, you'd be hoping this isn't the case so that you could pick up some stock while it's out of favour.

Want the full picture on analyst estimates for the company? Then our free report on Hangzhou Youngsun Intelligent Equipment will help you uncover what's on the horizon.Is There Any Revenue Growth Forecasted For Hangzhou Youngsun Intelligent Equipment?

The only time you'd be truly comfortable seeing a P/S as low as Hangzhou Youngsun Intelligent Equipment's is when the company's growth is on track to lag the industry.

Retrospectively, the last year delivered a decent 7.6% gain to the company's revenues. The latest three year period has also seen a 22% overall rise in revenue, aided somewhat by its short-term performance. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

Shifting to the future, estimates from the dual analysts covering the company suggest revenue should grow by 25% over the next year. That's shaping up to be similar to the 23% growth forecast for the broader industry.

With this in consideration, we find it intriguing that Hangzhou Youngsun Intelligent Equipment's P/S is lagging behind its industry peers. Apparently some shareholders are doubtful of the forecasts and have been accepting lower selling prices.

The Bottom Line On Hangzhou Youngsun Intelligent Equipment's P/S

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've seen that Hangzhou Youngsun Intelligent Equipment currently trades on a lower than expected P/S since its forecast growth is in line with the wider industry. Despite average revenue growth estimates, there could be some unobserved threats keeping the P/S low. However, if you agree with the analysts' forecasts, you may be able to pick up the stock at an attractive price.

Before you settle on your opinion, we've discovered 3 warning signs for Hangzhou Youngsun Intelligent Equipment (2 shouldn't be ignored!) that you should be aware of.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Hangzhou Youngsun Intelligent Equipment might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603901

Hangzhou Youngsun Intelligent Equipment

Hangzhou Youngsun Intelligent Equipment Co., Ltd.

Reasonable growth potential slight.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.0% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor