- China

- /

- Professional Services

- /

- SZSE:300492

3 Promising Growth Companies With Insider Ownership Up To 23%

Reviewed by Simply Wall St

As global markets navigate the impact of rising U.S. Treasury yields, growth stocks have shown resilience, with the tech-heavy Nasdaq Composite Index managing slight gains despite broader market challenges. In this environment, companies with high insider ownership can be particularly appealing as they often signal confidence from those who know the business best, aligning leadership interests closely with those of shareholders.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 17.3% | 21.1% |

| Arctech Solar Holding (SHSE:688408) | 37.8% | 25.3% |

| People & Technology (KOSDAQ:A137400) | 16.4% | 35.6% |

| Medley (TSE:4480) | 34% | 30.4% |

| Findi (ASX:FND) | 35.8% | 64.8% |

| Adveritas (ASX:AV1) | 21.2% | 144.2% |

| Plenti Group (ASX:PLT) | 12.8% | 107.6% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.9% | 95% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.4% |

| UTI (KOSDAQ:A179900) | 33.1% | 134.6% |

We're going to check out a few of the best picks from our screener tool.

FULONGMA GROUPLtd (SHSE:603686)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: FULONGMA GROUP Co., Ltd. manufactures sanitation equipment in China and has a market cap of CN¥3.67 billion.

Operations: FULONGMA GROUP Co., Ltd. generates its revenue primarily through the production of sanitation equipment in China.

Insider Ownership: 19.2%

FULONGMA GROUP Ltd. demonstrates characteristics of a growth company with high insider ownership, although recent earnings show a decline in net income to CNY 115.39 million from CNY 186.3 million year-on-year for the first nine months of 2024. Despite this, the company's revenue is forecast to grow at 16.8% annually, outpacing the Chinese market average of 13.9%. Its price-to-earnings ratio of 23.1x suggests it might be undervalued compared to the broader CN market's average of 34x, while its earnings are expected to grow significantly at an annual rate of approximately 26.65%.

- Click here to discover the nuances of FULONGMA GROUPLtd with our detailed analytical future growth report.

- Insights from our recent valuation report point to the potential overvaluation of FULONGMA GROUPLtd shares in the market.

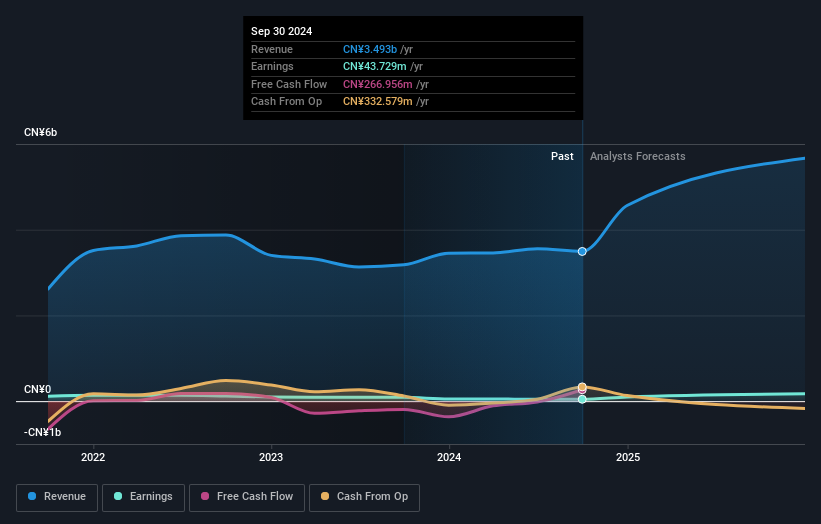

Dayu Irrigation GroupLtd (SZSE:300021)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Dayu Irrigation Group Co., Ltd specializes in the manufacture and sale of water-saving irrigation materials, with a market cap of CN¥3.55 billion.

Operations: Revenue Segments (in millions of CN¥): The company generates revenue through the production and distribution of water-saving irrigation materials.

Insider Ownership: 23.8%

Dayu Irrigation Group Ltd. shows potential for growth with earnings forecasted to increase significantly at 90.1% annually, surpassing the Chinese market's average of 25%. However, recent results reflect a drop in net income to CNY 29.87 million for the first nine months of 2024, down from CNY 36.28 million last year, and profit margins have decreased from 2.8% to 1.3%. The company has expanded its share buyback plan, signaling confidence in future prospects despite current financial challenges.

- Click to explore a detailed breakdown of our findings in Dayu Irrigation GroupLtd's earnings growth report.

- Our comprehensive valuation report raises the possibility that Dayu Irrigation GroupLtd is priced higher than what may be justified by its financials.

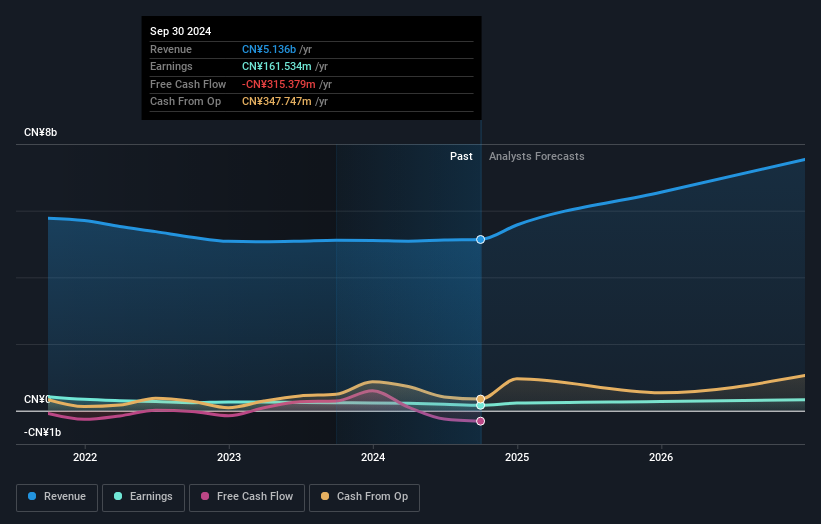

Huatu Cendes (SZSE:300492)

Simply Wall St Growth Rating: ★★★★★★

Overview: Huatu Cendes Co., Ltd. is an architectural design company offering professional design, consulting, and engineering services to various clients in China, with a market cap of CN¥10.14 billion.

Operations: Huatu Cendes generates revenue through its architectural design, consulting, and engineering services provided to state-owned enterprises, multinational corporations, private companies, and government agencies in China.

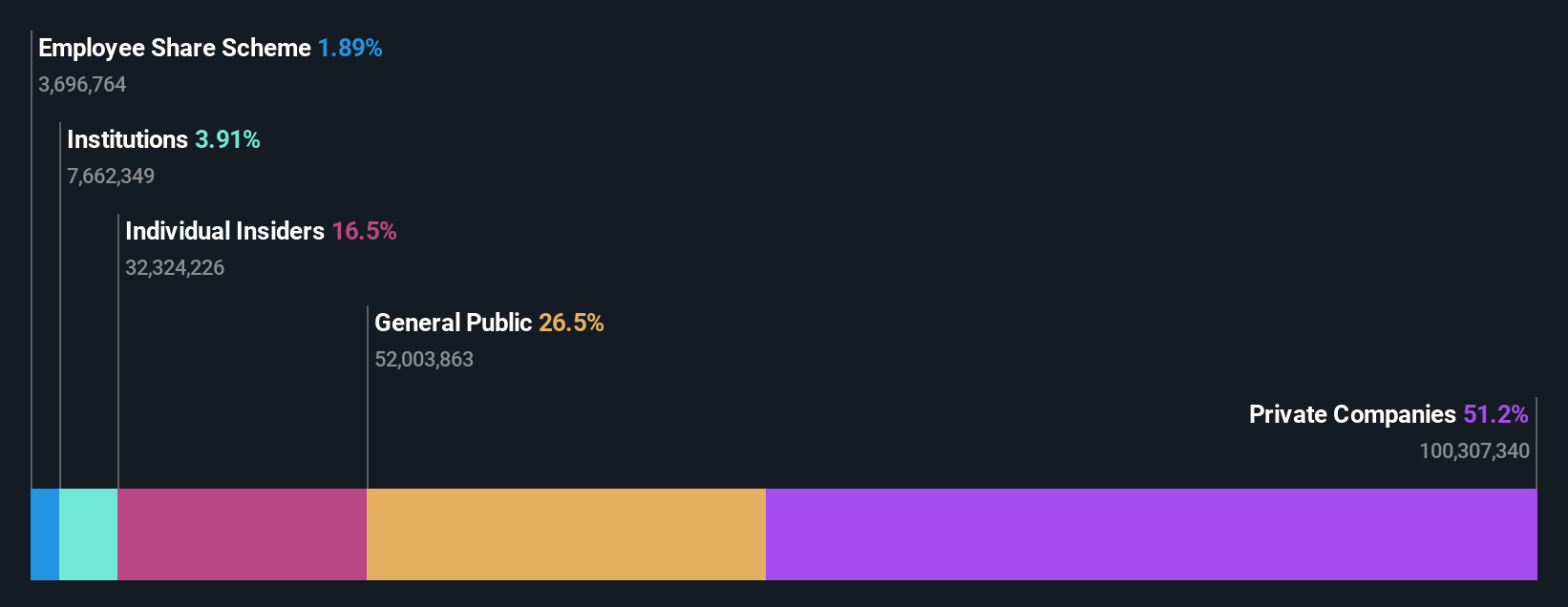

Insider Ownership: 22.4%

Huatu Cendes demonstrates strong growth potential with its earnings forecasted to rise significantly at 62.7% annually, outpacing the Chinese market's 25%. The company reported substantial financial improvements for the nine months ended September 2024, with sales surging to CNY 2.13 billion from CNY 44.37 million and net income reaching CNY 129.43 million compared to a net loss previously. Despite high share price volatility, Huatu remains undervalued against its estimated fair value.

- Click here and access our complete growth analysis report to understand the dynamics of Huatu Cendes.

- Our valuation report unveils the possibility Huatu Cendes' shares may be trading at a discount.

Summing It All Up

- Click this link to deep-dive into the 1530 companies within our Fast Growing Companies With High Insider Ownership screener.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Huatu Cendes might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300492

Huatu Cendes

Huatu Cendes Co., Ltd., an architectural design company, provides professional, designing, consulting, and engineering services to state-owned enterprises, multinational corporations, private companies, and government agencies in China.

Exceptional growth potential and good value.