Advertisement

Zhejiang Yuejian Intelligent Equipment Co.,Ltd.'s (SHSE:603095) 29% Price Boost Is Out Of Tune With Revenues

The Zhejiang Yuejian Intelligent Equipment Co.,Ltd. (SHSE:603095) share price has done very well over the last month, posting an excellent gain of 29%. The last month tops off a massive increase of 142% in the last year.

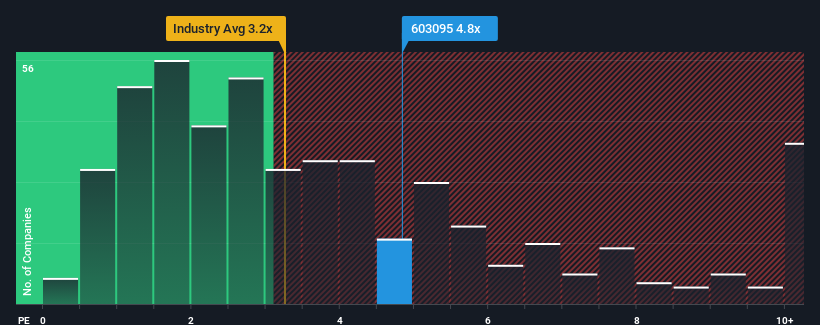

Since its price has surged higher, you could be forgiven for thinking Zhejiang Yuejian Intelligent EquipmentLtd is a stock not worth researching with a price-to-sales ratios (or "P/S") of 4.8x, considering almost half the companies in China's Machinery industry have P/S ratios below 3.2x. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

Check out our latest analysis for Zhejiang Yuejian Intelligent EquipmentLtd

How Has Zhejiang Yuejian Intelligent EquipmentLtd Performed Recently?

Recent times have been quite advantageous for Zhejiang Yuejian Intelligent EquipmentLtd as its revenue has been rising very briskly. It seems that many are expecting the strong revenue performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. If not, then existing shareholders might be a little nervous about the viability of the share price.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Zhejiang Yuejian Intelligent EquipmentLtd's earnings, revenue and cash flow.What Are Revenue Growth Metrics Telling Us About The High P/S?

The only time you'd be truly comfortable seeing a P/S as high as Zhejiang Yuejian Intelligent EquipmentLtd's is when the company's growth is on track to outshine the industry.

Taking a look back first, we see that the company grew revenue by an impressive 38% last year. Despite this strong recent growth, it's still struggling to catch up as its three-year revenue frustratingly shrank by 21% overall. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Weighing that medium-term revenue trajectory against the broader industry's one-year forecast for expansion of 22% shows it's an unpleasant look.

In light of this, it's alarming that Zhejiang Yuejian Intelligent EquipmentLtd's P/S sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. Only the boldest would assume these prices are sustainable as a continuation of recent revenue trends is likely to weigh heavily on the share price eventually.

The Bottom Line On Zhejiang Yuejian Intelligent EquipmentLtd's P/S

Zhejiang Yuejian Intelligent EquipmentLtd's P/S is on the rise since its shares have risen strongly. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Zhejiang Yuejian Intelligent EquipmentLtd revealed its shrinking revenue over the medium-term isn't resulting in a P/S as low as we expected, given the industry is set to grow. Right now we aren't comfortable with the high P/S as this revenue performance is highly unlikely to support such positive sentiment for long. Unless the recent medium-term conditions improve markedly, investors will have a hard time accepting the share price as fair value.

Having said that, be aware Zhejiang Yuejian Intelligent EquipmentLtd is showing 5 warning signs in our investment analysis, and 1 of those is potentially serious.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Yuejian Intelligent EquipmentLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603095

Zhejiang Yuejian Intelligent EquipmentLtd

Zhejiang Yuejian Intelligent Equipment Co.,Ltd.

Excellent balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.0% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor